Heresy · 08:30 NY

Nvidia: Great Company, Bad Hold — Closelook Heresy VI

Nvidia is the best business in the AI build-out — but its stock leadership is episodic, not permanent: front-loaded into each architecture, then handed downstream, then restarted by the next chip. Hopper restarted it. Blackwell restarted it. If Rubin ships as successfully as its predecessors — the likely case on product grounds — a fresh leadership leg may be opening, not closing.

Nvidia is the best business in the AI build-out. That is not the same as the best stock to hold mindlessly straight through a chip cycle — its leadership is episodic, front-loaded into each new architecture and then handed downstream. But episodic cuts both ways: every architecture so far has restarted the leg. Hopper did. Blackwell did. Rubin, on the evidence, may be next.

The orthodoxy

The consensus on Nvidia is short enough to fit on a hat: it is the AI trade, so you own it, and you keep owning it. Every dip is a gift, every quarter a confirmation, every roadmap slide a reason to add. Nvidia earned that reputation the hard way — the margins are real, the moat is real, the execution has been close to flawless. None of that is in dispute here.

What is in dispute is the conclusion. “Great company” has quietly hardened into “permanent hold,” and those are not the same sentence. The first is a statement about the business. The second is a statement about the stock, the price you are paying, and the part of the cycle you happen to be standing in. As our own NVIDIA Investor’s Timeline puts it, the question that matters is not “is Nvidia a good company?” — it is “is Nvidia’s stock a good risk-adjusted investment at this price?” At 50x+ forward earnings, those two questions can have opposite answers.

The heresy

Nvidia’s leadership is episodic, not structural. It is front-loaded into the opening act of each new architecture cycle, and then — reliably, mechanically — it fades. Not because the company stumbles, but because the trade moves on without it.

You want to own Nvidia when the next architecture is being priced. You want to be somewhere else when that architecture is being deployed. Most investors do the opposite. They find their conviction to hold somewhere in the middle of the cycle — after the easy leadership leg, just as the baton passes downstream — and then sit through quarters of relative underperformance wondering why “the AI leader” is lagging the AI trade.

The stock is not a marriage. It is a lease that renews with every new architecture — expiring as one chip moves into deployment, reopening as the next one is priced. The entire skill is knowing which phase you are in. And right now, with Rubin’s launch on the calendar, the next lease may be about to open.

Two clocks, one cycle

There are two ways to watch the same chip cycle, and they tell you different things.

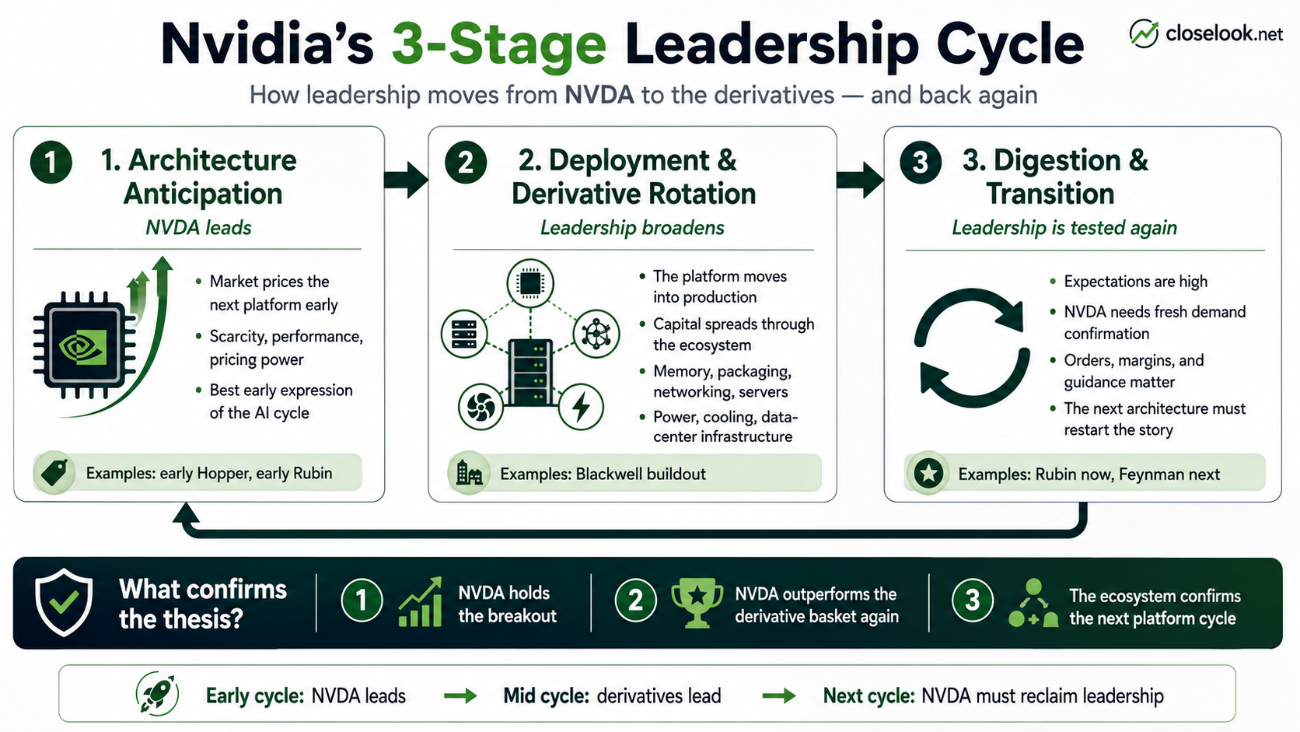

The first clock is the stock clock — the three-phase leadership model. Phase 1 is anticipation: the market prices the new platform before the revenue arrives, and Nvidia leads because it is the purest expression of scarcity. Phase 2 is deployment: the platform goes into production, the trade broadens into the supply chain, and Nvidia starts to lag. Phase 3 is digestion: expectations are full, the stock consolidates, and the market begins searching for the next catalyst.

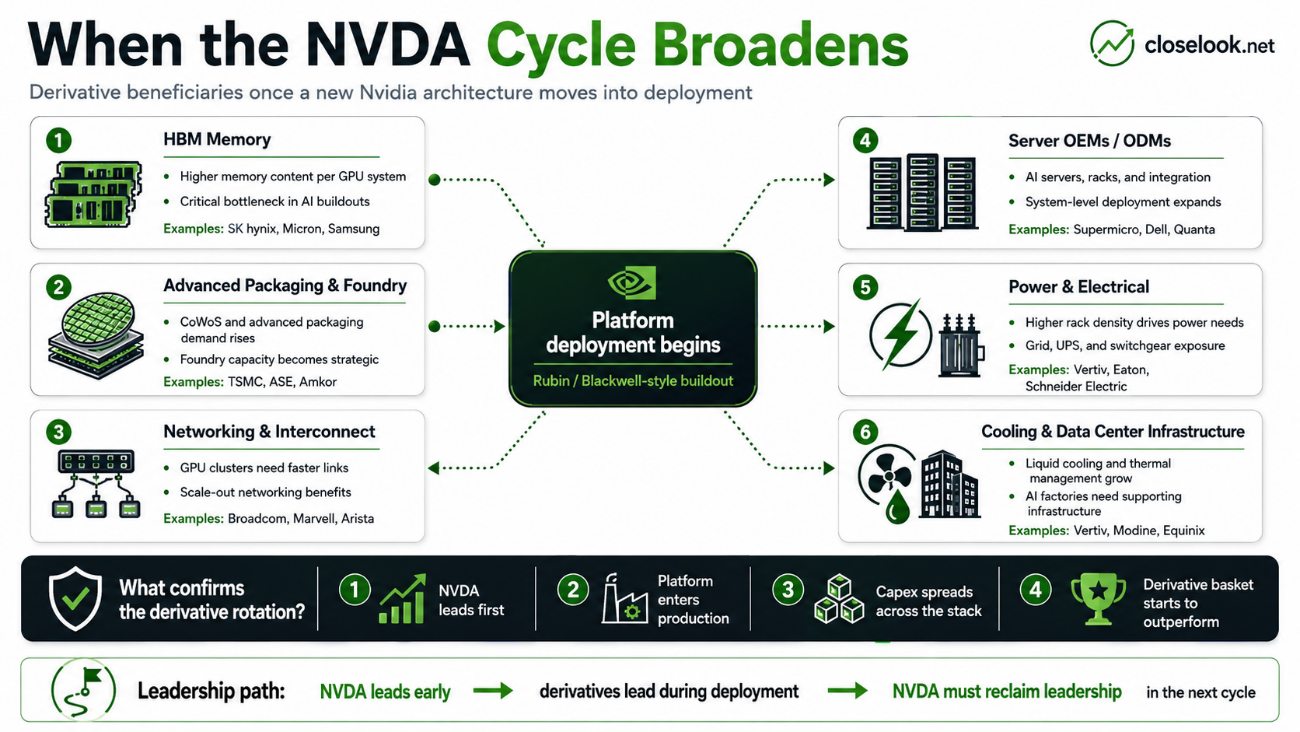

The second clock is the supply-chain clock — Generation Rotation, Layer 0 of the Weekly Signal: Dawn → Early Ramp → Mid-Ramp → Sunset. Dawn rewards EDA and IP. Early Ramp rewards memory (HBM) and advanced packaging (CoWoS, hybrid bonding). Mid-Ramp rewards networking, optical, cooling and power. Sunset flattens the architecture-specific names and opens the next Dawn.

These are the same phenomenon viewed from two seats. Map them together and the heresy stops being an opinion and becomes a schedule:

| Stock clock | Supply-chain clock | Who leads | Nvidia’s role | Posture |

|---|---|---|---|---|

| Phase 1 — Anticipation | Dawn → opening of Early Ramp | Nvidia; EDA / IP | First-order leader | Own Nvidia. This is the lease window. |

| Phase 2 — Deployment | Early Ramp → Mid-Ramp | Memory & packaging, then networking, cooling, power | Lagging compounder | Rotate into the Constraint Sectors. |

| Phase 3 — Digestion | Sunset | Quality, cash, next-gen Dawn | Range-bound, re-pricing | Reduce. Wait for the next Dawn. |

Read across one row and the rule writes itself: Nvidia’s leadership window is the anticipation window — Dawn and the opening of Early Ramp. Once Early Ramp confirms, leadership has already broadened, and you are holding the first-order name into its second-order phase.

The evidence is already on the tape

This is not a thought experiment waiting for data. The data has printed.

Generation Rotation flagged Rubin Early Ramp confirmed in April 2026 — Memory up roughly +61% year-to-date relative to broad semis, advanced Packaging up roughly +43%. Those are not random outperformers. They are the canonical Early Ramp beneficiaries doing exactly what the framework predicts when the baton starts moving: HBM allocation becomes the gating factor, packaging capacity becomes the throughput ceiling, and the constraint names lead because expanding their capacity is the only way to expand total output.

That is the Constraint Sectors thesis made visible. The packaging bottleneck (BESI, Kulicke & Soffa), the testing bottleneck (Advantest — a Sentinel ticker), the cooling constraint (Vertiv, Modine): structurally short of supply, small-cap, under-followed, and therefore mispriced relative to the headline names. In an Early Ramp, the bottleneck owns the pricing power. The bottleneck is not Nvidia.

So on the supply-chain clock, we are already past the point where Nvidia is the obvious overweight. The Rubin leadership leg has, by the framework’s own reading, already started leaving the building — and it walked downstream into the constraints.

What Hopper and Blackwell already showed

The episodic pattern is not a theory; it is on the long-term chart. Each time Nvidia has brought a genuinely new architecture to market, the stock has opened a fresh leadership leg around the launch — and only later, once that platform moved into deployment, did leadership broaden into the supply chain while the stock digested.

That is the part the “baton has left” reading underweights. Yes, the baton moves downstream during deployment — but it comes back to Nvidia when the next architecture is priced. And from a product standpoint, a successful Rubin is the high-probability case: the roadmap is credible, the demand is visible, and Nvidia has not missed a generation. If Rubin lands the way Hopper and Blackwell did, the cyclical logic points to Nvidia re-taking the front of the trade — a new leadership leg, not a fade, as the base case.

So what is the June breakout?

Here is where the two readings collide, because the breakout sits directly on the seam between them.

Nvidia just pushed above the grey trading range it had digested in since late 2025. The Daily Pulse called this correctly as crunch time: a breakout that needs confirmation, a stock that must now stay out of the box. Fair. But the framework forces a second reading the bulls are not pricing.

There are two ways to interpret a Nvidia breakout that arrives after Early Ramp has already confirmed:

- The restart. Rubin is large and credible enough to open a fresh Phase 1 — a second anticipation leg, this time for the Rubin-to-Feynman handoff. Nvidia re-takes first-order leadership and the constraints follow it higher.

- The handoff rally. The breakout is the last, loudest leg of the existing anticipation window — a relief move and a crowd catching up — while the real Rubin leadership has already rotated into memory, packaging and the constraint complex.

Both readings are live, and the breakout alone cannot separate them. But the precedent tilts the odds toward the first. Hopper and Blackwell both produced exactly this shape — the stock pushing to new ground as the market began to price the next architecture — and both resolved into renewed Nvidia leadership rather than a fade. With Rubin’s launch on the near calendar and its product success the high-probability case, a fresh anticipation leg is the reading the chart is most consistent with.

The discipline still matters: Generation Rotation exists as Layer 0 precisely so you confirm leadership rather than assume it. But assuming the breakout is only a handoff — that Nvidia is finished leading this cycle — is the mirror-image mistake to blind permanent-hold, and the last two launches argue against it.

The decision rule

Strip away the narrative and the heresy reduces to one operating line:

Own Nvidia for the anticipation, not the deployment. Lease the architecture window; rotate to the constraints when Early Ramp confirms.

That rule is symmetric, and the symmetry is the point. Through the deployment phase that dominated early 2026 it pointed the marginal dollar at the under-followed bottleneck names — the Constraint Sectors and the Rubin Functional Index — that owned the pricing power while Nvidia digested. But the same rule says you own the first-order name into anticipation, and a Rubin launch is precisely the event that reopens that window. The rule never said “sell Nvidia.” It said hold it for the right reason — the cycle, not the marriage — and as the next leg is priced, that reason points back toward Nvidia.

This is also why our reference portfolios track Nvidia through the Functional Index and Sentinel tickers rather than holding the stock as a permanent anchor. We are positioning in the sub-sector tied to this phase — not the one that led the last phase, and not the one the crowd is finally noticing.

Reality check: what would prove this heresy wrong

A heresy without a falsification signal is just an attitude. Here is the line that decides it.

Watch Nvidia’s relative strength against the constraint basket — NVDA versus SMH, versus the HBM names, versus packaging and the Constraint Sectors watchlist, cross-checked against the Pattern 03b constraint screen.

- If Nvidia holds the breakout and its relative strength against that basket inflects upward — Nvidia leading the group, not merely keeping pace — then this is a genuine fresh Phase 1. Rubin is re-pricing Nvidia specifically, the orthodoxy wins this round, and the lease re-opens.

- If Nvidia holds the breakout in absolute terms but the constraints keep leading on a relative basis, then the heresy holds: the AI build-out continues, but the better risk/reward has already moved downstream, exactly as the April Early Ramp signal said it would.

The breakout alone settles nothing. A leader is defined by relative strength, not by clearing a horizontal line. Absolute price can rise while leadership rots underneath it — that is precisely the trap the “permanent hold” crowd never sees coming, because they are watching the wrong clock.

There are honest ways the framework itself breaks, and they are worth naming: a stretched or compressed generation cadence distorts the phase timing, a skipped or accelerated architecture scrambles the rotation, and a genuine CapEx-cliff demand shock collapses the phase structure entirely. The schedule assumes the architectural cadence holds. If that assumption breaks, every phase signal needs re-deriving — including this one.

Bottom line

Nvidia is the best company in the AI infrastructure cycle, and its leadership is episodic — front-loaded into each architecture, handed downstream during deployment, then restarted by the next chip. That is the whole heresy: the mistake is not owning Nvidia, it is holding it mindlessly, blind to which phase you are in.

Read the clock correctly and the current setup is constructive, not cautionary. Rubin’s launch is on the near calendar; on product grounds a successful Rubin is the high-probability case; and Hopper and Blackwell both show what a successful launch does to the stock. A new cycle may be starting, and with it renewed Nvidia leadership — provided Rubin delivers as its predecessors did. The June breakout is the early tell; NVDA’s relative strength against the constraint basket is the confirmation to watch.

Great company. Episodic stock. And the clock may be turning back its way.

Related reads: NVIDIA Investor’s Timeline · Generation Rotation · Constraint Sectors · Rubin Functional Index · Daily Pulse: Nvidia’s Crunch Time