Live Today — unreviewed draft

—

Pulse · Daily

Short market briefs, published most trading mornings at 08:30 New York time — one hour before the Wall Street open — with the occasional intraday read. A cowork mix: some agent-generated from the Closelook data spine (Money Temperature, pattern scanner, index moves, cointegration), some written by Thomas, often a blend of the two. 85 stories on file.

Live Today — unreviewed draft

—

QQQ out of its correction channel, semis through the consolidation, the Mag Seven at 71 and cloud at a four-year high — with the 7-10 year Treasury sitting on a two-year trendline.

Ten overlapping AI contests, one conclusion: models get plentiful, orchestration stays scarce. Palantir's 93% quarter priced it in forty-eight hours.

Korea trades like semis, India like software — and India shows the bottom grammar software showed months ago. MakeMyTrip referees the turn this morning.

MAGS +13% in a year vs QQQ +22, SOXX +110 — a capex-fear discount. Azure +43% and AWS +37% just refuted the fear where it was priced deepest.

Both raised AI capex; only demand-pulled spend got paid. Add SAP's agent deployment and Rubin economics, and the agentic year dates itself: H2 26 – H1 27.

SK Hynix printed a record and fell 9%. Teradyne printed one with a raise and gained 11%. The regime prices the forward line — into FOMC and MSFT/META.

Korea's -8% circuit-breaker session is a semiconductor print: KOSPI-NDX correlation at a 2021 high, and Corning -16% on an in-line guide.

Kimi K3's weights and its first independent assessments landed together: #1 in frontend code, 42.0 on SWE Marathon — but stage 17 of 32 on cyber.

ServiceNow and SAP made the same orchestration claim in one week. Enterprise software's agentic shift is a knockout over few control planes — the field, scored.

IBM's mainframes fell 42% while its AI servers grew 37%, Nokia's AI networking sales doubled, Google buys servers — the build-out dollar moves down the stack.

The market pays the vendors of the AI capex spree, not the spenders. Five megacaps now have nine days to show a path to monetize the spend. The scoreboard.

UBS's trading desk calls the momentum unwind near its end and buys the dip — with a basket that reaches past semis into AI opex and apps, the shape our Kimi-K3 series mapped. The week we score it.

One week after Kimi K3 wiped $15B off EDA, the market gets two sessions to choose between rotation and unwind — and the answer arrives with Alphabet's capex line after tomorrow's close.

Nikkei −4.7%, Taiex −4.9%, SOXX indicated below both June floors, the Nasdaq-100 entering its 28,550–28,200 zone — four forces meet the last lines, the close decides.

TSMC beats everything, raises 2026 capex to $60–64B and full-year growth past 40% — and trades −4% premarket. The churn under semis is being answered today.

ASML beat its own guide, skipped the bookings line and answered with a 30% EUV capacity add. Plus: June PPI at 8:30 ET — the hot side of the inflation wedge.

IBM fell 23% on a preliminary Q2 miss — customers front-ran memory price increases and shifted budgets to AI. Why this is legacy weakness, not software weakness.

SOXX closed on the 554 signal floor while software pressed its highs. CPI and five bank prints arbitrate the split tape's double decision — the levels to watch.

Japan urges its $1.8T pension giants to invest at home. Why capital repatriation could pressure the yen carry trade — and crowded US risk assets — this summer.

Twelve exits, three opens, seven adds in one session. VEU doubled as the single ex-US core; Korea, Taiwan and India carry the satellite risk.

SK Hynix's $26.5B ADR debuts at a premium; the HBM leader trades at 4.8x vs Micron's 6.6x and a 29.8x industry median. The memory trio, taken apart.

Rubin −9.6% on the week, +103% YTD; Agentic Winners +2.9% week, −21% YTD; HALO flat both ways. The week is rotating against the year — and Health Care leads globally in all regions at once.

One month inside S&P 500 tech: hardware held, software lagged. Five days: IT Services +10%, Software +5%, semis −6%. The rotation inside tech is days old.

Monday's semi bounce looked like buy-the-dip; the pre-market — Korea selling Samsung and SK Hynix despite strong earnings — argues rotation into HALO, agentic winners and low-vol. The SOXX 554 double-bottom decides it this week.

Both held their belief lines and bounce — but Bitcoin's five-wave drop signals a regime shift while gold's three-wave dip stays corrective. Up for the swing.

Sixteen log entries, mostly dividend reinvestment. The real moves: BB opened in two books, IBIDY as a strategic buy, laggard adds in BABA and MMYT, SPMO opened.

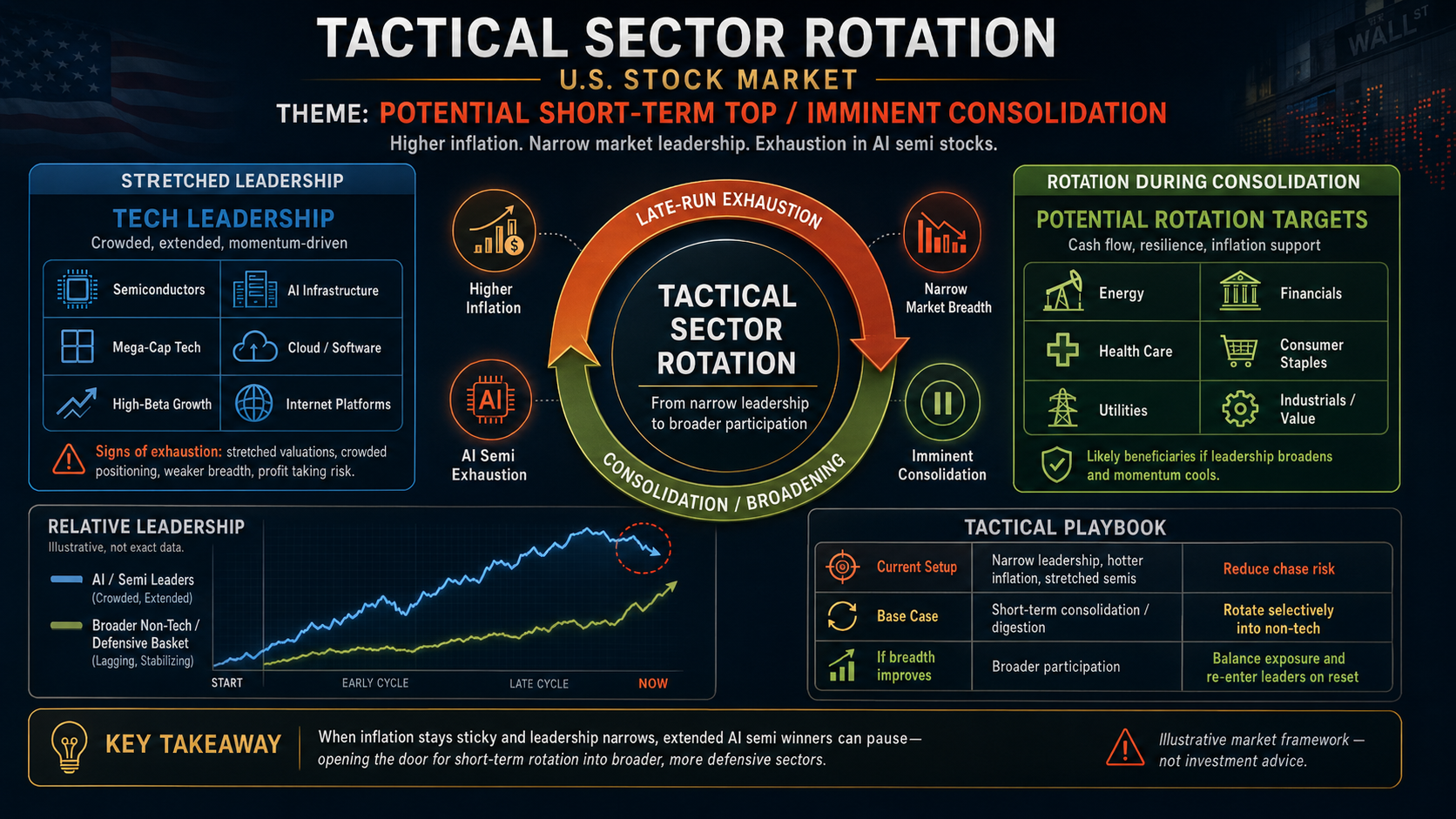

XLK still tops the one-year sector table, but over 21 trading days it is the weakest SPDR sector at −7.1% and its quadrant has flipped to Weakening. Industrials leads, seven sectors are improving — and HALO, the AI-neutral growth basket, is back above 1,050 and positive YTD.

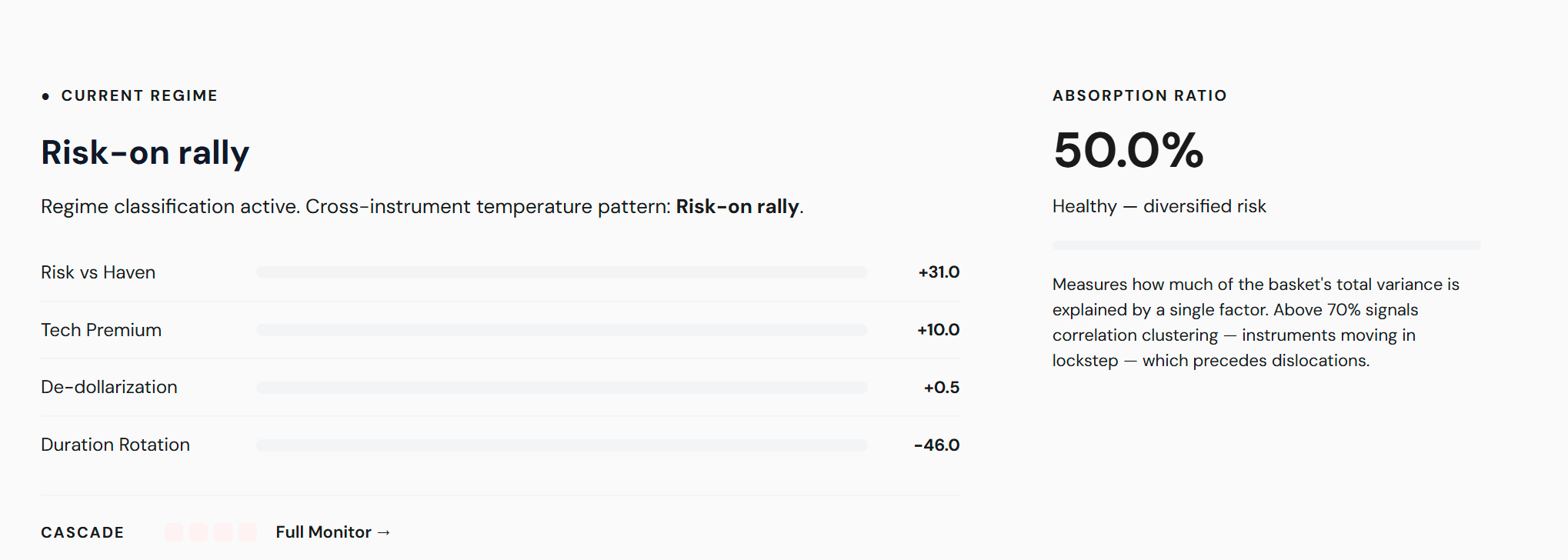

DXY is pressed against the 102 ceiling that has capped every rally since 2022, coiling on higher lows. A decisive close above 102 flips the macro trade from reflation to real rates — and makes the dollar the discriminator for gold, Bitcoin, and the AI-capex complex.

Gold and Bitcoin hit their belief levels together. A joint break reads two ways — forced de-grossing or a de-rating of the apocalypse into the AI build-out. Follow the proceeds.

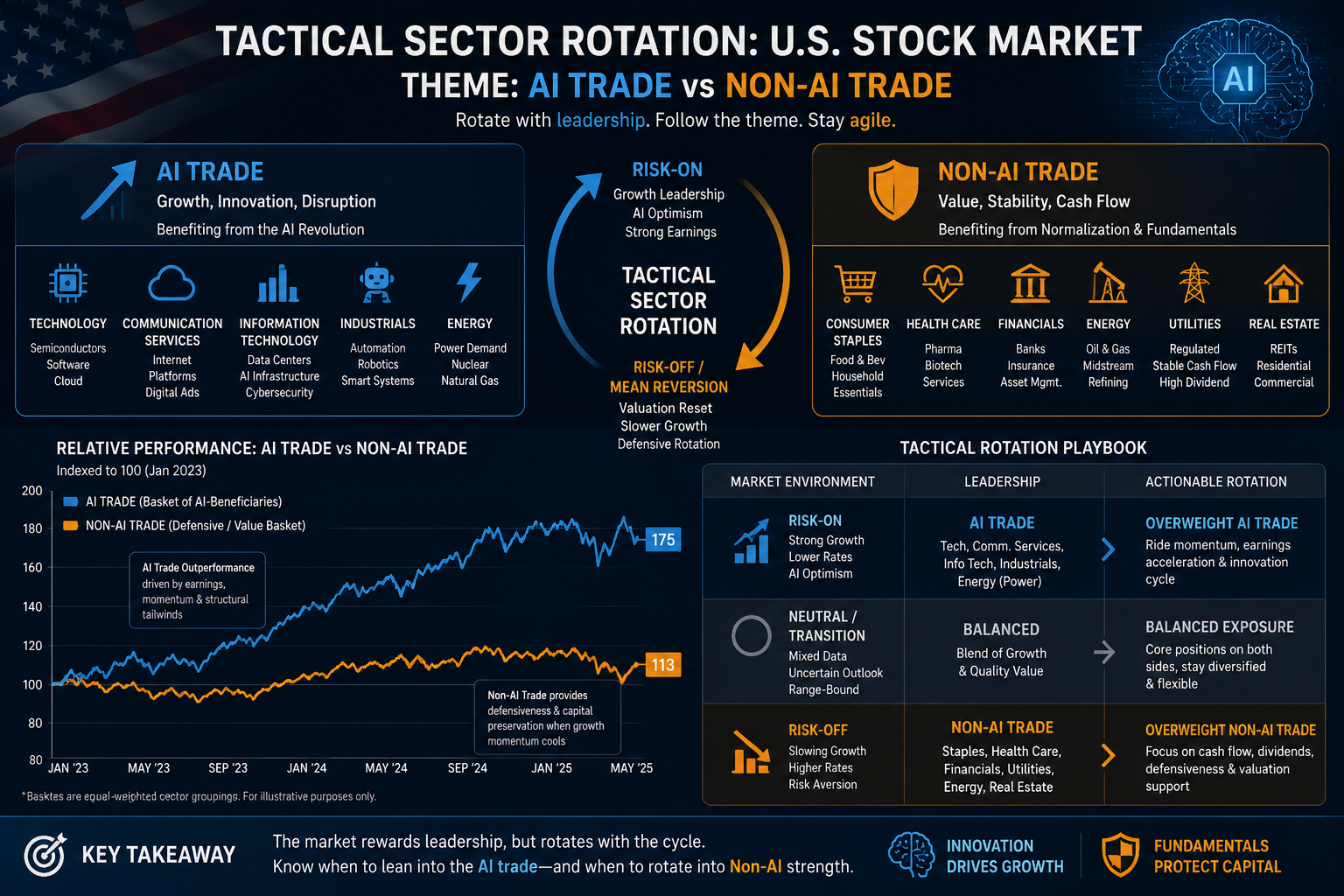

The AI trade is rotating from capex (semis) to the opex layer that gets paid when agents run — the Rubin rollout, the China model wave and TurboQuant pull it forward.

Why we reduced the infrastructure side of the AI trade — exhaustion and persisting negative divergences. The only buys: KLIC, MKSI and an ALAB put.

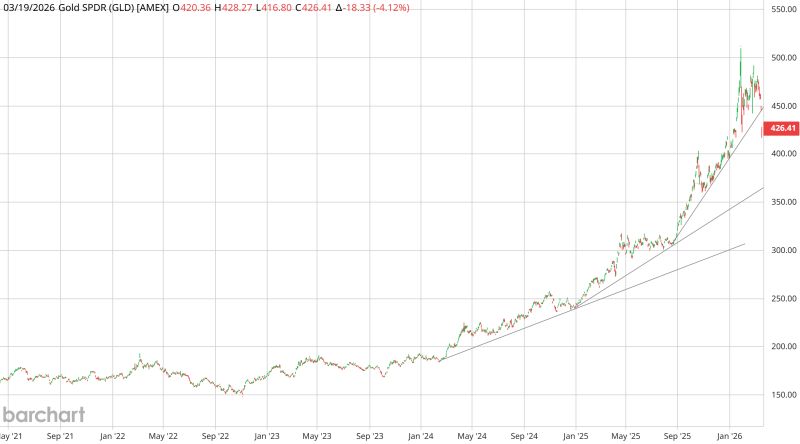

Gold's late-June 2026 drawdown wasn't a gold story but a plumbing story: Indian, Chinese and Western ETF demand all reversed, leaving bullion exposed to 2%-plus real yields. The one pillar still standing — price-insensitive central-bank buying — is why a rout became a correction. Plus the bull vs bear wave counts.

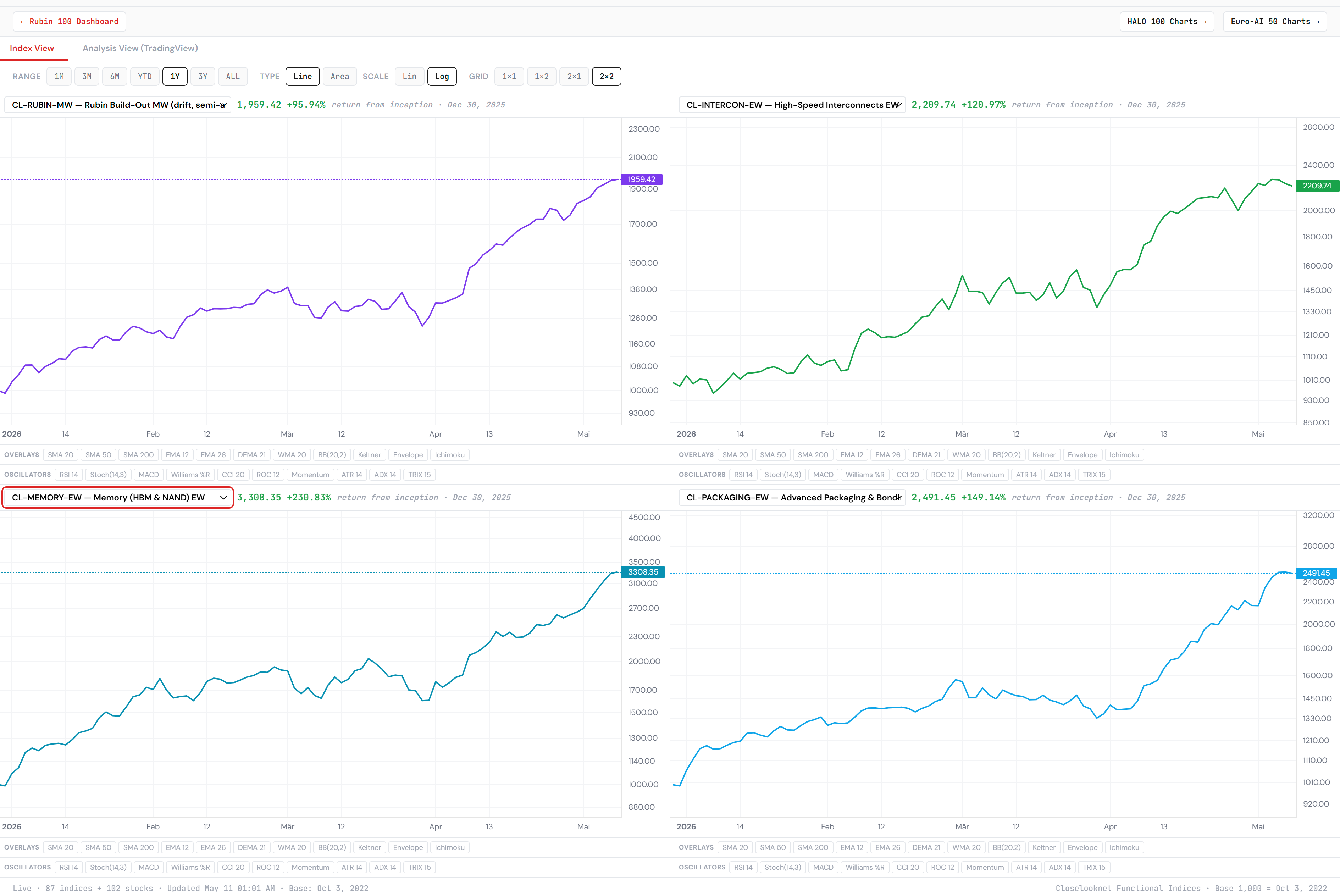

Memory dipped into Micron's print and ripped ~15% on the beat — but the beat isn't the story. 16 take-or-pay Strategic Customer Agreements (~$100B minimum contracted revenue, $22B deposits) attack the old memory bear case: customers are no longer buying memory, they're reserving it under contract.

Software's first derating was about duration. With Bank of America now floating three Fed hikes in 2026 and the belly of the curve under pressure, the next leg may pair a rising discount rate with an AI-softened earnings base — and when both move at once, the adjustment is multiplicative, not additive.

KOSPI -6%, European chips -5%, Nasdaq futures -2%: the AI trade derisks as Micron's make-or-break fiscal Q3 print nears. The real question isn't the beat — it's whether memory can shed its boom-bust discount.

Warsh's first FOMC delivered a hawkish hold — but the curve is splitting. The front end and belly reprice higher while TLT tries to base. Why that's a transitory signature, and what our Structural Inflation monitor says.

Four monthly charts, one clean split: India and China going nowhere while Taiwan (EWT) and South Korea (EWY) go vertical on the AI supply chain. Five forces behind it — composition, TSMC and HBM, regulatory inflows, flows leaving India, and China’s own drag.

Fresh records in the Rubin Build-Out 100 and the Dow, but semis, software and QQQ breadth are not confirming the AI trade — Generation Rotation in action.

Rockwell Automation (ROK) broke above $440 resistance to ~$457.59 after a strong fiscal Q2 — sales +12%, adjusted EPS +32%, raised FY26 guidance and Software & Control +20%. A diary read on ROK as a physical-AI infrastructure play: bullish but valuation-sensitive near 35x forward EPS.

The 10 June US close was a synchronised risk-off day: XSD −3.55% below 577.40, GLD −4.15% with no safe-haven bid, TLT flat. Defensive until semis reclaim 577–580.

CLOU broke its rising trendline; IGV is testing support. Salesforce and ServiceNow broke while Cloudflare and Datadog hold — bottom or dead-cat bounce?

Nvidia has broken above its trading range, but the breakout needs confirmation. The architecture-cycle read: Nvidia leads early, then leadership rotates to the derivatives (HBM, packaging, networking, power). Is Vera Rubin the start of the next Nvidia leadership leg, or does AI leadership stay downstream?

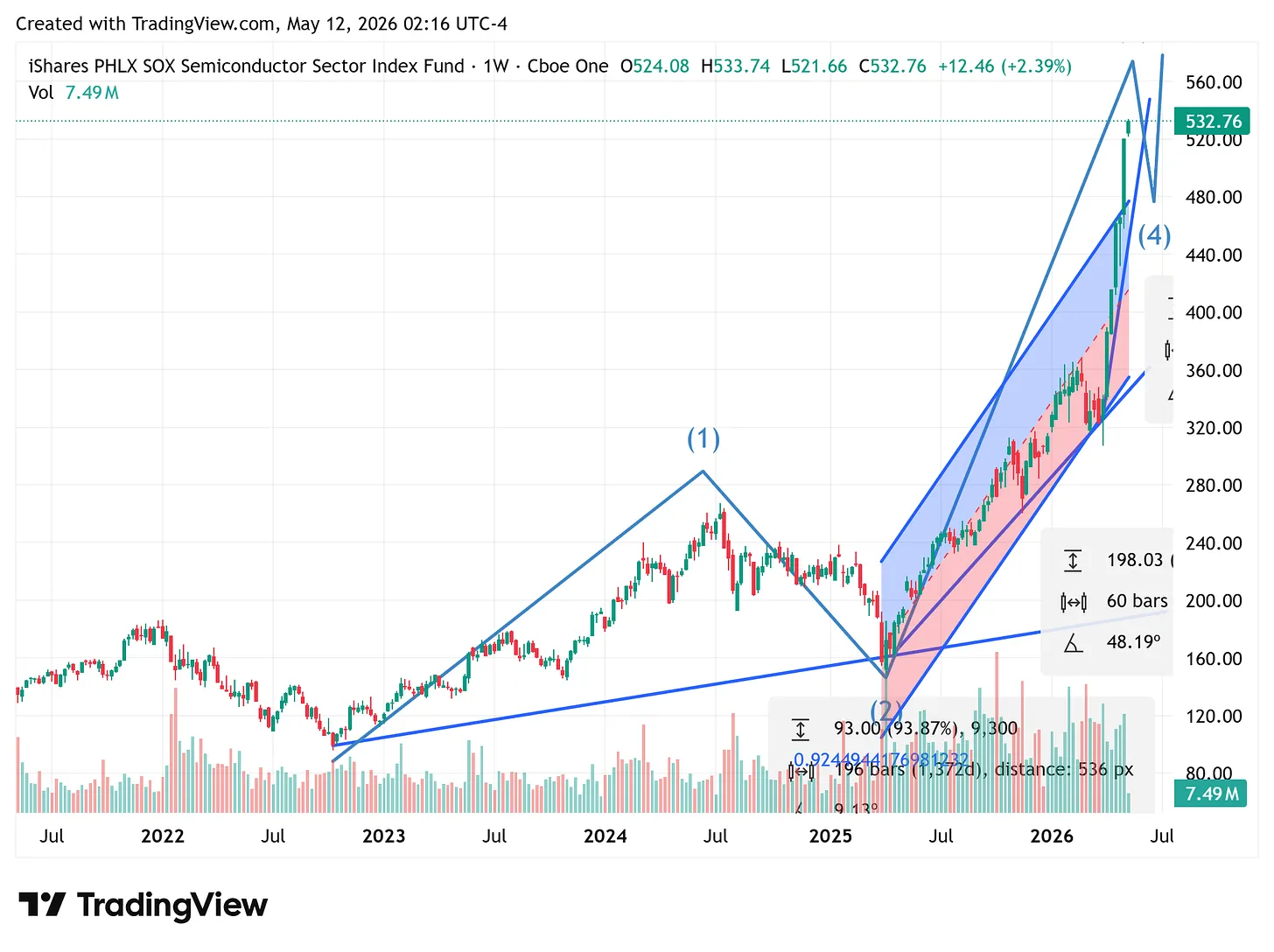

XSD -7.12%, SMH -5.38%: the equal-weight semis' breadth warning from 02 June has become price confirmation. The parabolic leg is over — support at 580 then 520, an A-B-C corrective the likely path.

Rubrik (RBRK) beat with revenue +39% to $387M and Agent Cloud as an enterprise-AI control layer; Samsara (IOT) beat +31% to ~$479M on physical-world operations — both strong prints with a muted market response on guidance.

Meta launches commercial AI agents across WhatsApp, Instagram and Messenger, and Arete Research upgrades META to Buy with a $735 target — an idiosyncratic 5% rally that decouples from a weak tape after roughly 18 months of going nowhere.

SMH +5.46% on five days; XSD -0.46% — the equal-weight semis rolled over while the cap-weighted complex climbs. A short-term top in the second tier, not the end of the bull.

A new class of value stocks is forming: old-tech hardware names — Dell, HPE, Texas Instruments, Lenovo, Intel, HP Inc.

BTC at 73,248 (−2.47%), back on the 50% retrace at 71,581. A possible fifth wave down would flip the regime — 71.6k is the hinge, 60k the verdict.

GLD trades 408.56 on the lower rail of its 30-day regression channel. Closelooknet reads this as Wave A — first leg, not the whole move.

Pattern 03 admits public names when NVIDIA takes equity stakes or admits them to named architecture layers.

Rubin 100 +3.37% leads a narrow tape; VXN and VVIX compress as VIX ticks up; Europe midday broadly bid. Closelook Daily Pulse 2026-05-22.

Semiconductor architects up 5.4% while US futures slip 0.4–0.6% and European indices trade lower. VVIX above 96 flags vol uncertainty.

Rubin +14% vs HALO −4.5% on the month — a narrow AI-infrastructure tape as cross-asset selling and VVIX spike signal rising fragmentation.

Rubin +14% vs HALO −4.5% on the month — a narrow AI-infrastructure tape as cross-asset selling and VVIX spike signal rising fragmentation.

MOVE +7.8% vs VIX −3.3%: the vol complex splits. Narrow tape, defensive rotation, and Rubin vs HALO diverge 23 points on the month.

Daily Pulse May 18: every cross-asset closed down Friday, Korea −6.1%, XLE alone bid, Rubin −3.3%, 6 cointegration breaks.

Closelook Daily Pulse May 15 2026: Temp 62 risk-on, Rubin +5.80% week / +25.41% month, Memory +9.7% / Interconnects +18% on the week, breadth thins,…

Closelook Daily Pulse May 14 2026: risk-on at 59, Rubin 100 +25.1% on the month, scanner flags defensive support-confluence tests, 7 cointegration breaks.

Rubin −3% after 27% monthly surge as defensives bid: XLV +1.96%, XLP +1.28%, XLF +0.78%. Semis roll: SOXX −3.15%. Rotation signal forming.

SOXX into its third ever-steeper trendline. Three consolidation triggers stack against semis: NVIDIA earnings, US-Iran, post-Trump-Xi euphoria fade.

Closelook Daily Pulse: Euro-AI 50 +3.1% today, +23% on the month. Seven cointegration breaks, zero new pairs — regime in transition.

Rubin 100 up 2.3% on the day and 39% over one month. Seven cointegration breaks, zero active pairs. HALO lags as risk-on narrows.

Gold heads for 360–370 — 13% lower, trendline plus horizontal-support confluence. Bitcoin's verdict hinges on 86,877.

Microsoft's earnings call reframed enterprise software pricing into per-user-and-usage. IGV reclaimed 83.91.

Closelook Daily Pulse: Rubin 100 +3.4% leads a risk-on session at Temperature 56 while defensive names form support-confluence patterns;…

ServiceNow und IBM beat-and-lose am selben Tag. Multiple-Compression 85–90% durch, Bridge-Math netto positiv. NOW $81.24 / IGV $74.62 ist der Test.

Nine rotation-out-of-tech calls since October 2022. Same script, same ending. The exit door strategists keep pointing at is a mirror.

Closelook Daily Pulse: Rubin 100 +30.8% monthly, AW25 +11% weekly, six cointegration breaks signal relative-value regime shift.

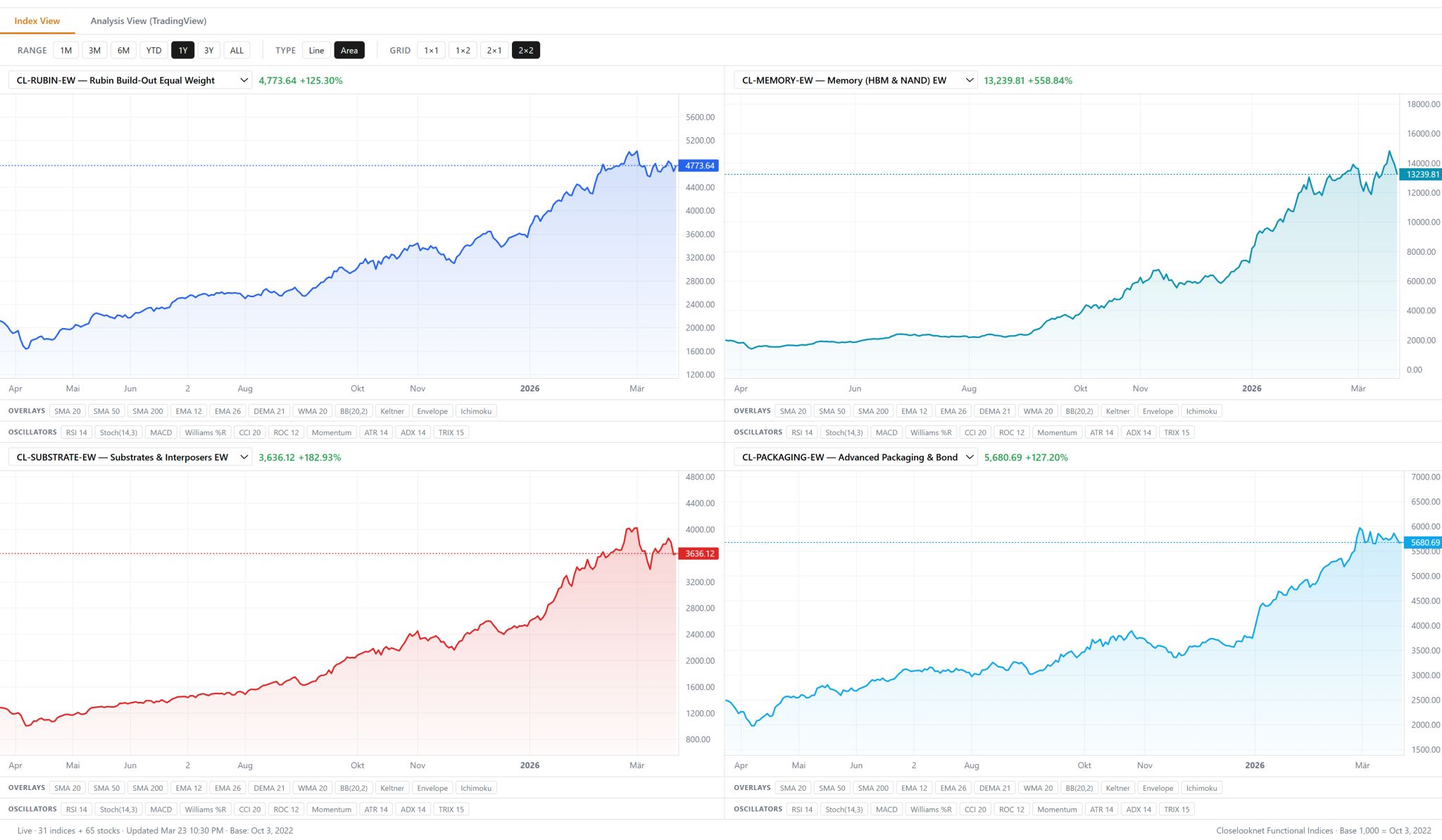

Nasdaq 100 up 6% YTD. Rubin Build-Out 100 up 65% equal-weight, 90% momentum. The spread is the Generation Rotation Framework working layer by layer.

Gold printed ATH a month before Iran war and has given back 14%. Bitcoin quietly reclaimed $74k. The positioning reveal is the trade.

Closelook Daily Pulse Apr 16: Temperature at 59 risk-on, AW25 surges 5.3% intraday, cointegration breaks hit 6 as pair structures reset.

Closelooknet's Agentic Winners 25: a 25-name tactical index across 7 sectors built to identify enterprise software platforms agents cannot operate without,…

Closelooknet tracks Jensen's $2B Marvell investment via NVLink Fusion — rack-scale inference infrastructure confirming the token-generation demand surge…

Closelooknet tracks how stacked inference optimizations — speculative decoding, distillation, caching — compress per-workflow costs toward cents,…

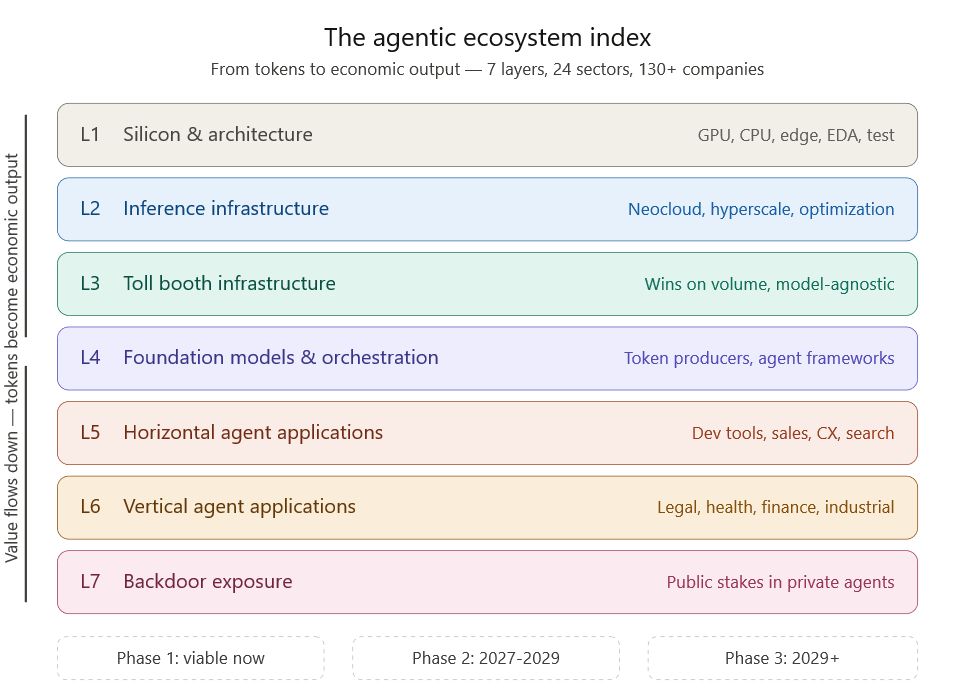

Closelooknet maps the demand side of the AI infrastructure cycle: a seven-layer, 24-sector index tracking 130–150 companies as inference costs collapse…

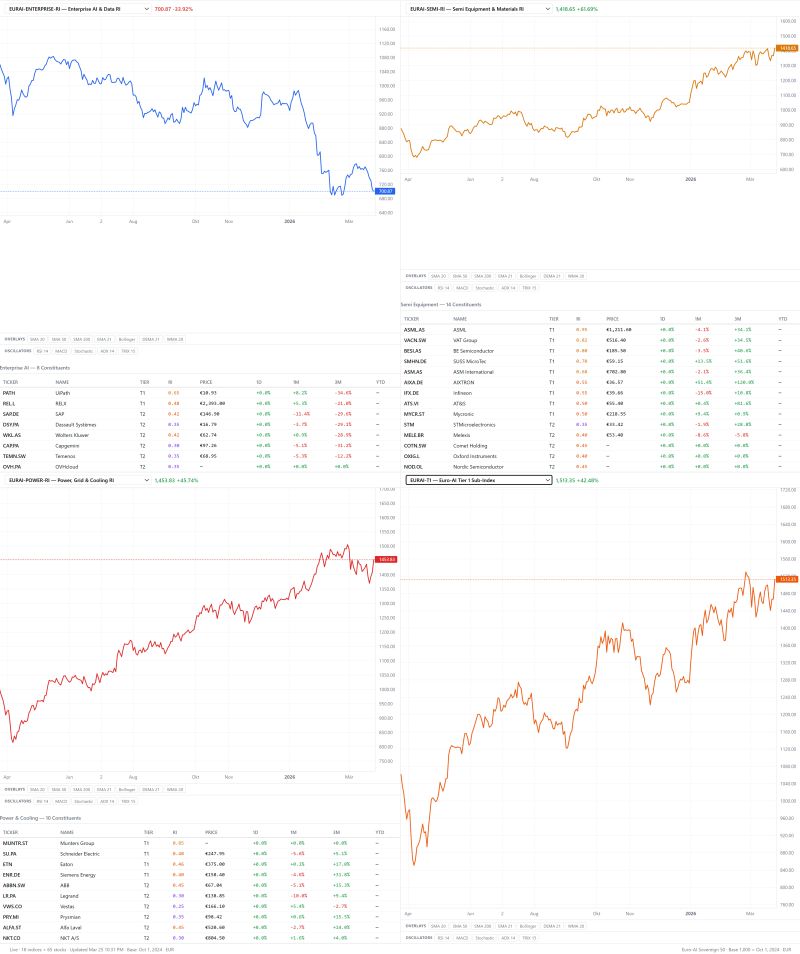

Closelooknet's Euro-AI Sovereign 50 tracks 50 European-listed names across six AI sectors — semi equipment at +61.7%, power and grid at +45.7%,…

Closelooknet tracks Google's TurboQuant — a training-free KV-cache compression algo that cuts memory 6x,…

Closelooknet tracks 100 physical-layer companies NVIDIA cannot route around — deposit, etch, packaging, interconnects,…

Closelooknet examines why gold correlates with M2 and real-rate compression, not CPI — only 16% of price variation since 1971 tied to US inflation.

Closelooknet unpacks why gold fell 8–10% amid Middle East conflict: margin-call liquidation, a hawkish hold on rates,…

Closelooknet tracks GLD's double-top near $500, a broken steepest trendline, and a failed ATH despite bullish macro — signs the momentum phase may be…

Closelooknet applies factor attribution to Gold and the Rubin Build-Out: when speculative-flow β runs 3x central-bank β,…

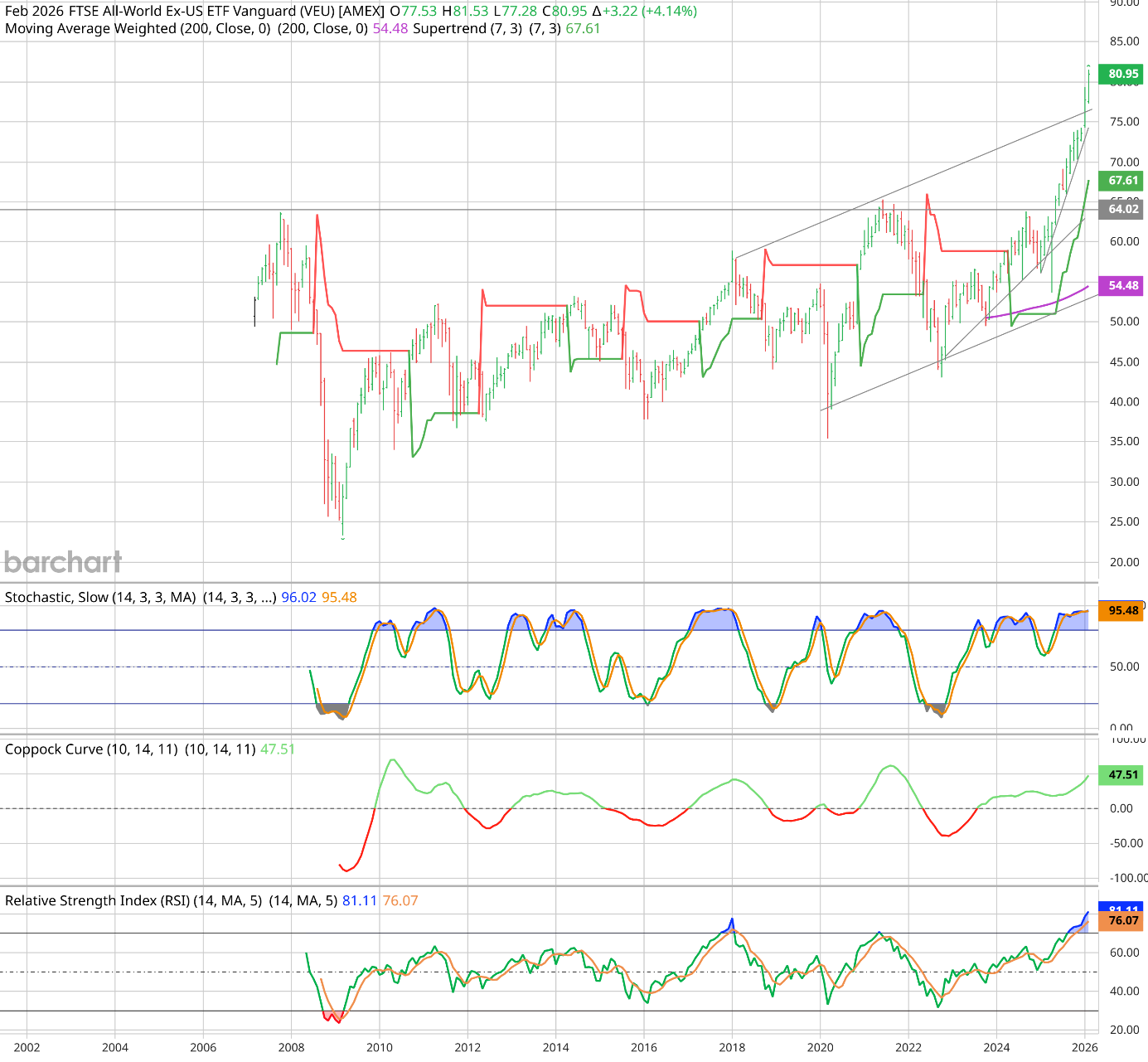

Closelooknet tracks VEU's breach of $64.02 fifteen-year resistance — RSI at 81, Coppock rising, Supertrend green — as capital rotates from U.S.

Closelooknet tracks $DXY slicing through 2011 trendline support, Coppock Curve at −13.09, and what a secular dollar bear cycle historically means for…

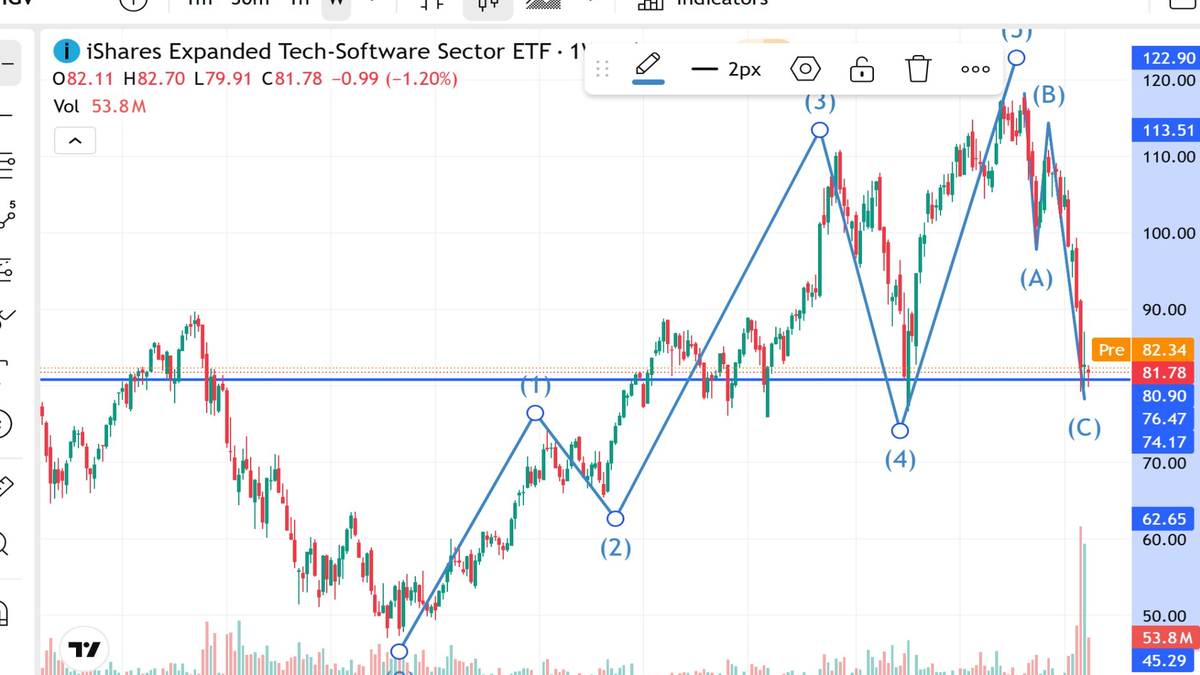

Closelooknet tracks IGV completing an ABC correction into wave (1) support at $82 — a potential double bottom,…

85 pulses · new every trading morning at 08:30 NY.