Read · · 10 min read

The make-or-break memory print — and the one question that decides whether the multiple finally re-rates.

For years, Micron earnings were treated as a niche semiconductor-cycle event. Important for memory investors, yes. Relevant for DRAM pricing, inventory digestion, and gross-margin watchers, sure. But for the broader market? Usually not the main event.

How it resolved: Micron beat, guided Q4 toward $50B, and the stock ripped ~15% instead of fading — the full follow-up is in “Micron Didn’t Sell the Peak This Time”. This preview is kept as published.

That has changed.

Micron's report on Wednesday, 24 June, after the bell is now one of the most important near-term tests for the AI trade. The reason is simple: AI is no longer just about GPUs. It is about the entire infrastructure stack — accelerators, networking, power, cooling, servers, and increasingly, memory.

And memory is where Micron sits. It is also the only US-headquartered company making high-bandwidth memory at scale. The other two are SK Hynix and Samsung. Three companies make essentially all of it. Right now, there is not nearly enough.

From cyclical to strategic

High-bandwidth memory, DRAM, and storage are no longer boring components in the background. They have become strategic bottlenecks in the AI buildout. If Nvidia is the engine of the AI trade, memory is part of the fuel system. Without enough fast memory, AI servers cannot fully perform. Without pricing power in memory, the broader AI supply-chain story looks less explosive.

The numbers behind that re-rating are not subtle. A year ago Micron traded below $100 a share. It crossed a trillion dollars in market cap in late May — the second memory company in history to do so, after Samsung.

Last quarter it printed record revenue of $23.9 billion, net income of $13.8 billion, and $5.5 billion in free cash flow, at a gross margin around 75%. For a business that historically ran 30–45% margins and swung violently with the cycle, that is a different animal.

The mechanism is HBM. It stacks DRAM dies vertically — twelve high in the current generation — and links them with thousands of microscopic channels, delivering bandwidth measured in terabytes per second. It sits physically next to every AI accelerator. And it is brutally wafer-hungry: HBM consumes roughly three times the wafer capacity per bit of conventional DRAM, and that ratio climbs with each generation — HBM4 runs closer to four-to-one. Every wafer shifted to HBM is supply pulled out of the standard memory market. That is why consumer DRAM, server DDR5, and NAND prices have all ripped higher in parallel. Analysts have a name for it now — the “three-to-one rule”: every AI chip built destroys the capacity to make roughly three ordinary PC chips.

This is the part that makes the cycle look structural rather than cyclical. Micron has already exited the consumer market entirely, winding down its Crucial brand to feed enterprise and AI customers. Its entire calendar-2026 HBM output — HBM3E and HBM4 — was allocated and locked on price and volume back in late 2025. SK Hynix has called its 2026 capacity essentially sold out. Goldman Sachs, no perma-bull on this name, pegs the 2026 memory shortage as the worst in fifteen years and has revised its 2027 shortage estimate higher. New supply does not meaningfully arrive until 2027–2028: Micron's Idaho fab outputs first wafers around mid-2027, the New York megafab with Bechtel later, Singapore NAND not until late 2028.

Beyond the headline: what the print signals

The revenue line is what the wires will lead with, and the least informative number in the release. Guidance is $33.5 billion plus or minus $750 million; the Street sits near $34.7 billion; the EPS whisper runs north of $22 against a $19.15 guide. Micron has beaten its revenue guidance by a material margin for five straight quarters — so a beat is the base case, not the signal. Four operational reads carry more information than the headline, and one structural question, treated separately below, carries more than all of them.

HBM4 yields and the Rubin clock

HBM3E is sold out and priced; the live question is HBM4 for Nvidia's Vera Rubin, which entered full production in June and pushes 288 to 384 GB of HBM4 at roughly 22 terabytes per second — close to three times Blackwell. Nvidia certified all three memory makers on 5 June; Micron, widely reported as shut out of the first Rubin runs, had secured a slot by the time Jensen Huang said so on stage in Taipei. The number that matters is not whether Micron is in, but its yield and qualification cadence — how much of the ramp it can actually convert against SK Hynix's 60-to-70 percent grip on Rubin volume and an estimated 18 percent of the 2026 HBM4 market. Any hint of HBM4 yield trouble doesn't just dent Micron; it pushes the whole compute timeline right. The next fight is already visible: Rubin Ultra, on HBM4E, lands in late 2027.

The margin print is a pricing-mechanism tell

Eighty-one percent is the purest read on HBM pricing power — but the mechanism underneath it is what to watch. Micron's entire 2026 HBM book was locked on price and volume back in late 2025, while conventional DDR5 and DRAM are repricing in near-real-time against a spiking spot market. That has compressed the usual gap between HBM and commodity margins; on the margin, some desks now read standard DRAM as the richer incremental book. Whichever way it cuts, gross margin cracks before revenue when supply loosens — it is the earlier warning light than the top line everyone watches.

Capex — the snake eating its own tail

Micron guided fiscal-2026 capex above $25 billion, stepping up again in 2027. That is correct if demand stays structurally above supply, and the classic memory trap if it doesn't: tight supply lifts margins, fat margins invite spending, spending eventually builds the glut that ends the party. New capacity is a late-2027-into-2028 story — Micron's Idaho fab around mid-2027, the Korean makers each adding roughly 150,000 wafers a month of cleanroom, Samsung converting a third of a DRAM node to general-purpose memory. The tell on the call is any sign that NAND or DRAM expansion is being pulled forward; that is when the market starts pricing the peak.

The demand-efficiency wildcard

The bear's cleanest non-cyclical argument isn't oversupply — it's that the bit-growth math the re-rating rests on assumes memory intensity per unit of compute keeps climbing. Anything that durably bends that curve down — leaner model architectures, memory-saving techniques at the accelerator level — chips at the demand side the supply story can't answer. It is under-defined today, which is why it sits in the wildcard column rather than the bear column. But it is the question a careful investor keeps in a drawer.

The argument that owns the multiple

Strip away the revenue beat, the margin print, even the HBM4 ramp, and one question sits under all of them: does memory still deserve to be priced as a boom-bust business?

For four decades the market's answer was yes, and it never forgot. Memory makers have always traded at a discount to the rest of semis — low-double-digit earnings multiples even at the top of the cycle — because everyone learned the same lesson the hard way. Pricing was negotiated quarterly and cleared on the spot market; capacity always overshot; today's record margin was tomorrow's write-down. You did not pay up for peak memory earnings, because peak earnings were the warning, not the reward. That reflex — the refusal to capitalize good numbers — is the cyclical discount, and it is the single biggest thing standing between Micron at roughly fourteen times earnings and Micron at a multiple that looks like a secular grower's.

Contracts, not beats

What deletes that discount is not a bigger number. It is visibility — and the only thing that manufactures visibility in a commodity is a contract.

So the part of Wednesday's call that matters least to the headline matters most to the multiple: the structure of Micron's customer agreements. The bull case is no longer “demand is strong” — strong demand is cyclical, and the market knows it. The bull case is that the way memory is sold has structurally changed. In place of the old quarterly haggle, hyperscalers are reportedly locking three-to-five-year supply agreements with volume and price fixed in advance — the model that let Micron close its entire 2026 HBM book on price and volume back in late 2025, and that has SK Hynix sold out just as far. If that is real and it extends, memory stops being a spot-priced commodity and starts looking like a contracted, capacity-constrained supplier with years of booked revenue — a business the market is finally allowed to capitalize.

That is the exact mechanism behind the most aggressive call on the Street. UBS's Timothy Arcuri, whose $1,625 target is the highest on Wall Street, does not get there with a higher revenue estimate — he gets there by arguing the long-term, partially fixed contracts justify roughly fifteen times forward earnings instead of a cyclical discount. Same earnings, different multiple: the whole bull case is a re-rating argument, not an estimate argument. Goldman, near $400, makes the opposite bet in the same language — that the contracts are thinner than they look, the margins are a peak and not a floor, and memory will be memory in the end.

Which is why the evidence management has to put on the table is specific, and it is not the 2026 book — 2026 is sold out and priced in. It is 2027. How much of next year is already under long-term agreement rather than exposed to spot. How long the deals run. Whether the pricing is genuinely fixed and premium, or locked on volume but soft on price. How broad the customer set is beyond the marquee names. Monday's Anthropic pact is the template they will point to — a multi-year supply agreement for memory and storage tied to Anthropic's own build-out, alongside a Micron investment in the company — but the disclosed terms are about multi-year intent, not fixed volumes and prices. Closing that gap is the call's real job. Sanjay Mehrotra has already said Micron can fill only half to two-thirds of what its key customers want on a multi-year basis; converting that scarcity into signed, durable, premium contracts is the entire game.

Because that is what investors are actually waiting for. Not another beat — Micron has beaten for five straight quarters and the stock still wears the discount. They are waiting for proof that the boom-and-bust reflex can be switched off for good, so the multiple can move up and stay up. Give them multi-year contracted coverage of 2027 and the re-rating has room to run. Give them a record quarter and a shrug about “strong demand,” and the oldest instinct in the sector takes over: sell the peak.

The Closelook lens: both legs are running hot

There is a way to see what the re-rating did to the stock itself, beyond the fundamentals. Split MU's sensitivity to the Nasdaq-100 into its up-day and down-day halves and the regime break is unmistakable: through the 2026 melt-up MU's beta stepped from about 1.9 — its level from late 2024 through 2025 — to roughly 2.8, and the old downside-heavy tilt (it used to fall harder than it rose) flattened to almost symmetric. The stock did not just go up; its whole relationship to the market changed gear.

Right now the upside leg is running near 3.1 — almost two standard deviations above its own three-month norm — while the downside leg, at 2.7, is also elevated. Our convexity score, which reads each leg against its own history, sits at +0.94 and is rising at its fastest pace in months. For now the asymmetry is bending the right way.

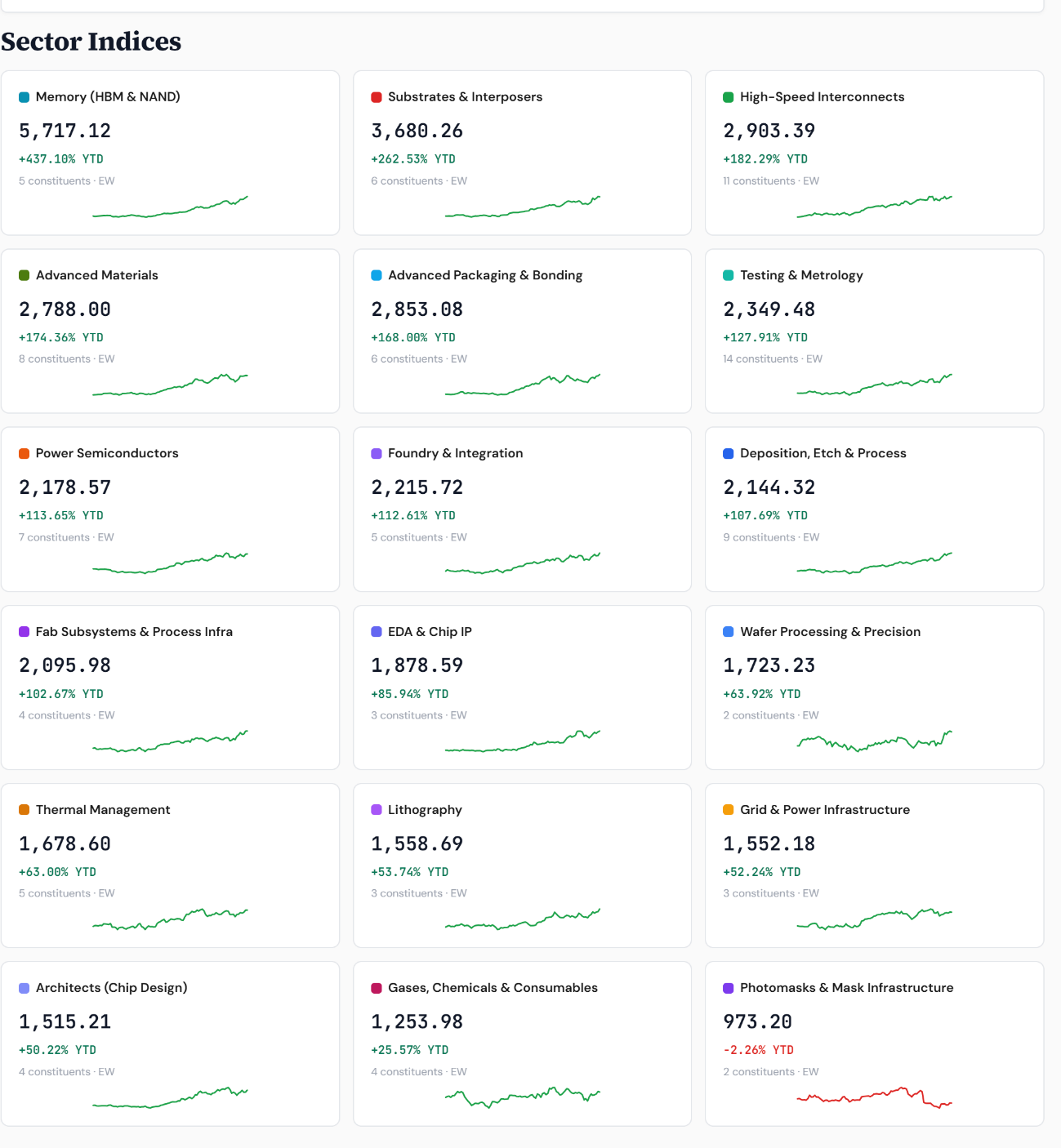

But this is not the clean, one-sided convexity of a name that catches the upside and sheds the downside. It is the entire beta inflating — more of everything, leaning up. A stock in that state pays handsomely on up-tape and bites just as hard on down-tape, which is precisely the tension going into a binary print: MU has been catching roughly three times the index on its up-days, and the same machinery runs in reverse if Wednesday disappoints. Run the same split on the memory basket Micron belongs to, and on our Rubin Build-Out index, and both sit near beta 1.4–1.5 to the Nasdaq this year — barely half Micron's 2.8. The whole complex re-rated; Micron is simply its highest-octane expression. (Closelook Beta Instability monitor vs QQQ, through 18 June — closelook.net/lab/market-structure/.)

The pulse check

And it prints into a tape that has just turned. As of early Tuesday trading, the global semiconductor complex is derisking hard: South Korea's KOSPI — home to Micron's two HBM rivals — fell more than 6% overnight, European chip names are off around 5%, and Nasdaq-100 futures are down more than 2%. Micron's own record close now meets a market pulling risk off the table right as the print lands.

Positioning is stretched and the options market is pricing a move of roughly 17% on the print. The same day, the broader complex is watching: hyperscaler AI capex is tracking toward roughly $700 billion in 2026, up from around $400 billion in 2025, and Reuters has flagged Micron as a “pulse check” for whether that spend is holding. Nvidia holds its annual meeting the same day. A clean beat-and-raise with firm, contract-backed 2027 HBM commentary is another green light for the entire stack. A merely “good” print — solid numbers, cautious guidance, any hint of capex-driven supply on the horizon — hands the crowd an excuse to take profits across the most crowded trade in the market.

Micron used to report on the memory cycle. This week, it reports on the health of the AI cycle.