Weekly Signal · · 10 min read

Half-Time on the AI Trade

The build-out splits into three, and the second half belongs to the layers that use it.

29 June 2026 — closes through Jun 26.

Last week, the market was two-speed. A slim majority of stocks still participated, the broad tape was not broken, but a narrow engine carried the index gains: the AI build-out.

The S&P 500 closed Friday at 7,354, down 2.0% on the week, while the Nasdaq fell 4.5%. Apple and Microsoft raised consumer product prices, citing memory and storage chip costs that have more than doubled since autumn 2025 and are expected to more than double again by the end of the year. The main driver has been the demand for DRAM and NAND from AI data centers.

Rubin, our capex index, was the load-bearing wall — until Thursday. The question was whether semiconductors could keep carrying the structure; on Friday they tumbled.

It is now the last weekend of the first half. Rubin closed the half +124% from its December inception, the cleanest trade of H1. But as the half ends, the question changes shape. It is no longer can capex keep carrying the market. It is does leadership rotate from building the factory to using it.

Because the AI trade is still alive, and it is no longer one trade. It has split into three clocks: capex, opex, and applications.

A note on the word, because it matters for the canon. These are not the clock of Heresy IX. There, clock meant the thing that sets the cadence — NVIDIA, and the memory layer beside it. Here it means timing of onset: the capex clock ticks first, the opex clock second, the application clock last. Same word, different axis — and the two frames lock together, because these three clocks are the macro phases the constraint relay passes through. Capex is the supply relay building the stack. Opex is the recurring-rails layer that gets paid when the stack runs. Applications are the demand link — the one arrow in the relay that does all the work, and the one most likely to break.

What the first half actually did

The split is already on the tape. You do not have to forecast it. You can read it in two lines.

Rubin closed the half +124% from inception. Software — IGV — closed it −18% over the same six months. The market paid a violent price for the factory and sold software that has not yet proven it captures agentic value. XLK and QQQ finished green — tech up, but up because the capex engine carried it, not because the breadth was healthy.

That divergence between Rubin and IGV is the three-way split, compressed into two numbers. The build-out and the application layer did not move together in H1. They moved in opposite directions.

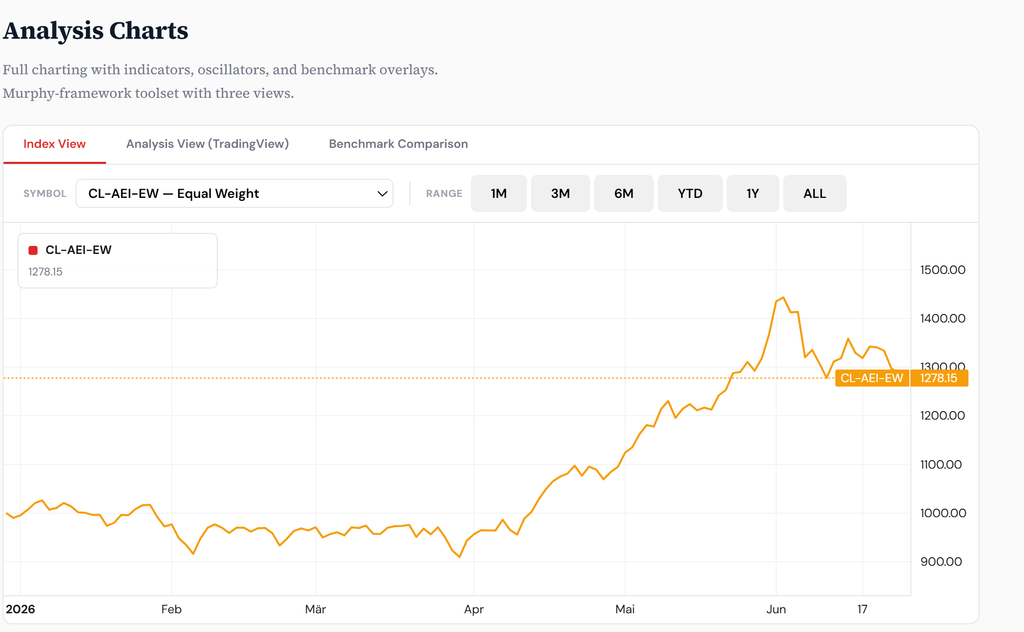

And yet the capex index is no longer accelerating. Rubin peaked near 2,450 in early June and sits at 2,241 now — the trend is intact, the acceleration is gone. The Agentic Ecosystem equal-weight tells the same story one layer down: it ran from 1,000 to a peak near 1,450 in early June, then corrected to 1,278. Up strongly on the half. Off roughly 12% from its high.

That is what a maturing build-out trade looks like. The theme survives. The market stops rewarding everything attached to it with the same force and starts asking which constraint is next, which is already priced, and which part of the chain is now vulnerable to being digested.

The relay, now running in three places at once

H1 was a single clean relay. GPU, then memory, then packaging, then power, cooling, optical, test, cloud capacity. The direction was obvious: find the bottleneck, buy the bottleneck, wait for the next capacity warning. The trade was a relay, and the baton moved in a straight line.

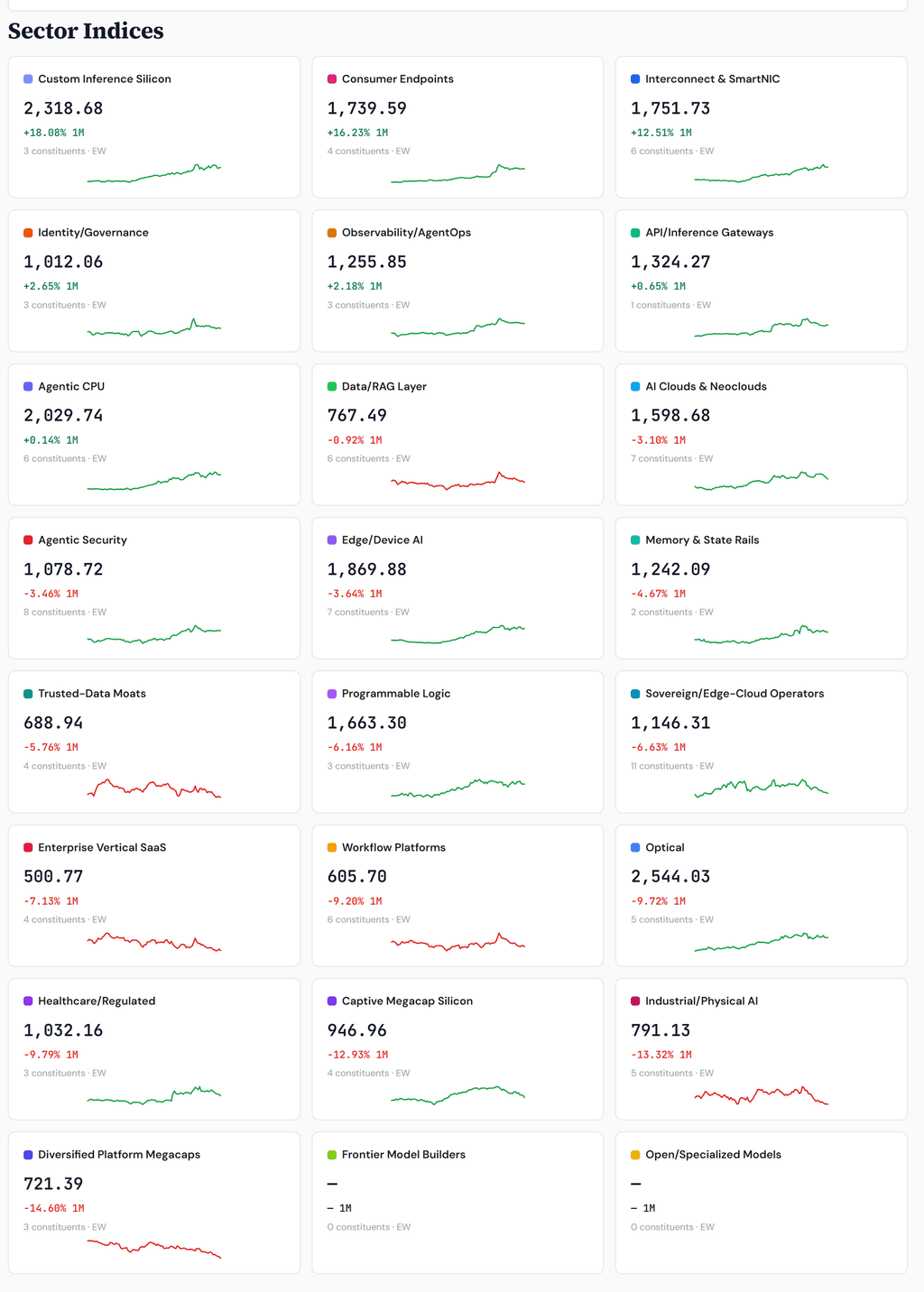

That relay has not stopped. It has gone internal. Inside the build-out, leadership now rotates rather than rising as one block. Optical led for months and is −9.7% on the month, digesting a large run. Custom Inference Silicon has taken the baton — +18% on the month, the strongest absolute sector performer in the agentic grid. The capex relay continues; it just no longer moves in one piece.

What changed at half-time is that a second and third relay opened above the first. Opex — running the factory. Applications — the factory's output meeting real demand. Three relays, three clocks, three different questions. Rubin answers: who builds the AI factory. Opex answers: who gets paid when it is used. Applications answer: who captures the product value when agents become the interface.

The point of half-time is that the market no longer has to move all three together.

Capex: maturing, mixed, still the foundation

No agentic economy exists without enough compute, memory, power, networking, and deployment. Rubin remains the foundation. But the basket has stopped behaving as one body.

The clearest signal in the capex layer is what is being sold. Diversified Platform Megacaps −14.6% on the month. Captive Megacap Silicon −12.9%. Industrial/Physical AI −13.3%. The megacaps are the worst performers in the grid. The market is deconglomerating the AI trade — moving from owning the megacap that does everything to owning the specific layer that actually binds. That is not the theme breaking. That is the theme maturing into a layer-by-layer market.

So in H2, a capex pause is no longer automatically a warning. Some pauses are warnings. Others are rotations. You tell them apart by whether the layer above confirms usage.

Opex: the cleaner H2 candidate — leading on momentum, not yet on price

This is the part of the stack that should matter most if the H2 story shifts from how much capacity gets built to how much gets used. Runtime, edge, data, observability, identity, security — the control system around autonomous software. Not optional layers. The reason an agent can be trusted, monitored, permissioned, and stopped.

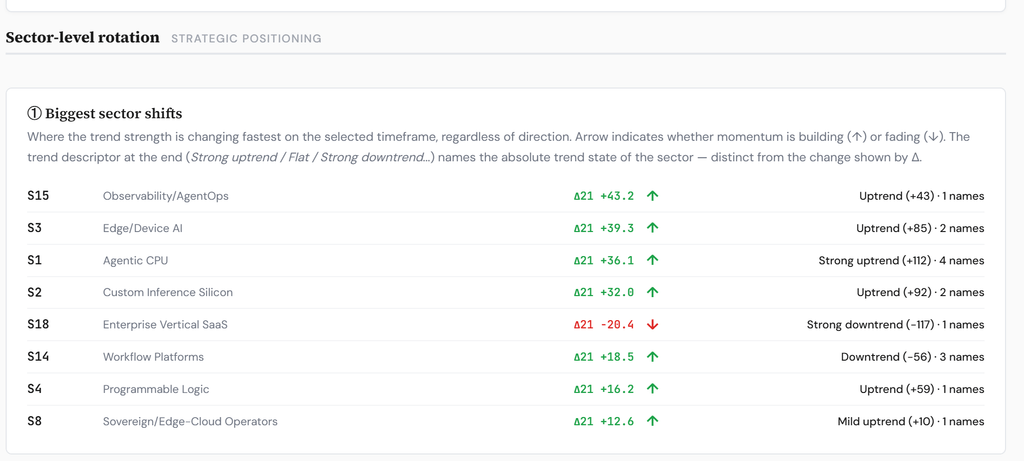

The momentum data says opex is turning. On the 21-day trend-strength shift, Observability/AgentOps is the largest builder in the entire grid, at +43.2. Identity/Governance, AgentOps, the operational layer around agents — all building trend.

But here is the honest read: the headline misses the mark. On price, opex has not led yet. Observability/AgentOps is only +2.2% on the month. Identity/Governance +2.7%. API/Inference Gateways +0.7%. The momentum is turning up before the price has. That is exactly what an early leadership candidate looks like — and exactly why it is still a candidate, not a confirmed trend.

The tell to watch into H2 is precise: opex price performance crossing into clear outperformance. Until the green in the 1-month column matches the green in the momentum column, opex is a thesis. When they converge, it is the trade.

The CPU: the relay's prediction, confirming live

The standout in the data is not opex. It is the CPU.

Agentic CPU prints Strong uptrend +112 — the strongest established trend in the entire agentic grid — with its 21-day shift still building at +36. Custom Inference Silicon: uptrend +92, +18% on the month. Edge/Device AI: strong uptrend, +85. These are the layers that scale up when the build-out shifts from training scale to inference, edge, and agent scale-out.

This is the call from Heresy IX, on the tape. The argument there was that the CPU layer sits below the co-determination threshold during the training-scale phase — when it mostly feeds the accelerators — and crosses above it as the phase turns toward agents, because the host becomes the thing that gates useful work. H1 was training scale. H2 is the turn. And the index is already pricing it: the CPU and inference-silicon layers carry the strongest trend in the agentic complex into the second half.

Note the nuance that proves it rather than breaking it. Agentic CPU is +0.14% on the month — flat. Strong established trend, consolidating at a high level after a large run. That is the sawtooth: a layer that refreezes on each generation's cadence, runs, then digests at altitude before the next leg. The trend is the signal. The flat month is the breath between.

If you want one structural rotation to anchor the H2 view, it is this. The CPU crossing the threshold is the relay's clearest live tell, and it is happening now.

Applications: the disruption is leading the enhancement

The application layer was always going to be the hardest and the most dispersed. The thesis was that an agentic cycle does not lift broad software — it sorts software into companies whose products become more valuable because agents act inside them, and companies whose products become less valuable because agents act around them.

The sorting has started. But read the data carefully, because the bifurcation is asymmetric. The disrupted side is loud and on the tape. Enterprise Vertical SaaS is the only large fader in the momentum grid — a strong downtrend getting worse, −20.4 on the 21-day shift, −117 in absolute trend. Workflow Platforms −9.2% and still in a downtrend. IGV −18% on the half. The pre-agentic incumbents — the screens, seats, dashboards, and workflow steps an agent can compress — are being repriced down, hard.

The enhanced side — the companies that own trusted data, a workflow that cannot be bypassed, distribution, the transaction layer, the regulated system of record, the final action an agent must execute — is not yet clearly green. The winners have not been printed.

So the application layer in H2 is currently pricing the threat before the opportunity. The market is selling what agents disrupt before it is buying what agents make more valuable. In relay terms, the demand link — the one arrow the whole loop depends on — is resolving as repricing down before repricing up. That is the air-pocket showing its early shape: cost is falling, but the value-capture at the application layer is arriving as loss before it arrives as gain.

The H2 question for applications is therefore not whether software recovers. It is whether the agent-enhanced winners emerge in the green — or whether the whole layer stays sold because adoption is too slow to offset the threat.

The H2 map

Three relays, and the market no longer has to move them together. That gives four shapes for the second half, and each has a line to watch.

A constructive rotation looks like this: Rubin consolidates from stretched levels without breaking, the opex sectors cross from momentum into price leadership (watch Observability/AgentOps and Identity turning the 1-month column green and outperforming), the CPU and inference-silicon layers keep their trend, and the application layer finally shows green winners alongside the red incumbents. That is the trade evolving — leadership moving downstream from building to using.

A correction looks different: Rubin and opex break together, the megacaps keep rolling, the Agentic Ecosystem equal-weight loses its current 1,278 footing, and applications fall as one. That is the theme being sold as a block rather than rotated internally.

The single most important line is the relative one — Rubin against the opex sectors. If Rubin pauses and opex leads, the trade rotates, and the message is constructive. If Rubin falls and opex falls with it, the trade corrects. And underneath that, the application bifurcation: the day the enhanced winners start printing green next to the disrupted incumbents is the day the real agentic economy begins to price.

Stance

Constructive on AI — no longer as one trade.

Capex is the foundation, and it is mixed. Own the binding layer, not the index; megacap deconglomeration suggests the market is already doing exactly that.

Opex is the cleaner H2 candidate, but it is unconfirmed: leading on momentum, waiting on price. Size into the confirmation, not ahead of it.

The CPU and inference-silicon layers are the structural rotation of the half — the strongest trend in the agentic grid and the relay's clearest live tell. This is the part of the build-out crossing the threshold into H2.

Applications are a sorting machine, and right now it is sorting downward first. Treat it as a sorting machine, not a rebound basket. Wait for the winners to appear in green before treating the layer as anything other than a source of dispersion.

The Weekly Signal is therefore simple. Watch whether AI leadership rotates downstream. If capex cools and opex leads, the trade is evolving. If both break together, the trade is correcting. If applications bifurcate with visible winners, that is not noise. That is the second half, beginning to price the real agentic economy.

That is the H2 signal.

Source: closelook.net Functional Indices, closes through Jun 26, recomputed Jun 27. This is an investment diary, not investment advice — Look Investment GmbH is not a licensed adviser.