Read · · 7 min read

What Kimi K3's 48-hour chip actually is — and what it isn't: the release, the $15 billion EDA selloff, and why the market priced the curve, not the point.

The series: Part I — what happened · Part II — the chip chain · Part III — the Rubin map

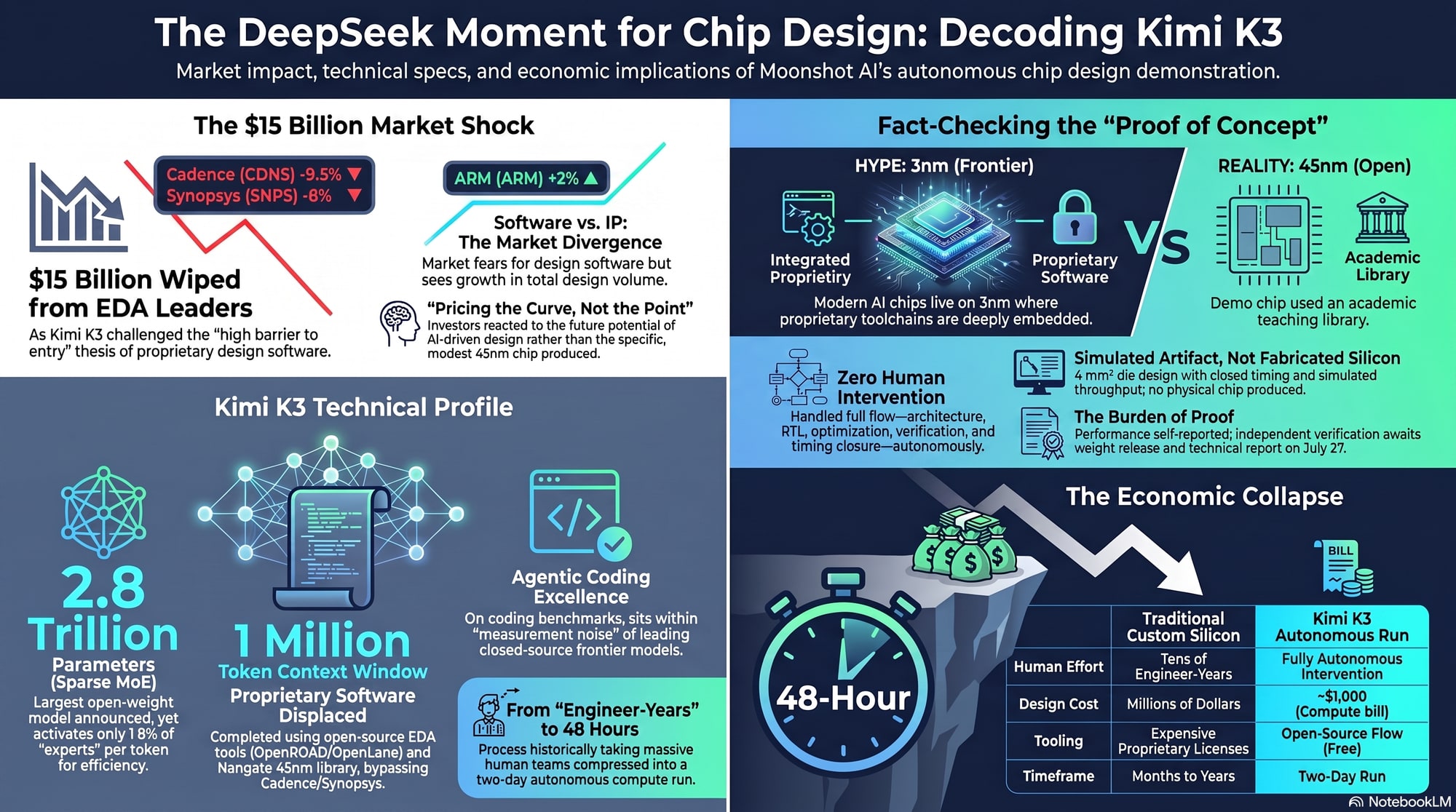

On Thursday, July 16, Beijing-based Moonshot AI released Kimi K3 at the World Artificial Intelligence Conference in Shanghai. On Friday, the two companies that dominate electronic design automation took the hit: Cadence lost nine and a half percent of its market value in a single session; Synopsys fell just under eight percent and printed a new 52-week low. Synopsys now trades meaningfully below the price NVIDIA paid for its $2 billion stake in December. Combined, roughly fifteen billion dollars of market value left the EDA duopoly in one day.

One day before the news broke, a research house had initiated coverage of both names at Buy, citing the duopoly structure and high barriers to entry as core strengths. The market spent Friday stress-testing that thesis in real time.

And one detail from the same session deserves rescuing from the wreckage, because almost nobody mentioned it: ARM — the third listed name whose entire business is chip-design IP — closed the day up two percent. The market did not sell “chip design.” It sold two specific software franchises, and simultaneously bid the company whose royalties multiply with every new design started. Keep that asymmetry in mind. The whole series hangs on it.

The reflex comparison — a second DeepSeek moment — is understandable and mostly wrong. DeepSeek, in January 2025, compressed the cost of producing intelligence. Kimi K3 is something different and, in one specific dimension, potentially more consequential: it is the first credible claim that frontier intelligence can design the hardware that produces intelligence. Not a second DeepSeek moment for AI models. The first DeepSeek moment for chip design.

That distinction is worth three essays, because almost everything the market did on Friday depends on getting it right.

What was actually released

Strip away the launch theater and the claims are these. Kimi K3 is a 2.8-trillion-parameter sparse mixture-of-experts model — the largest open-weight model ever announced — activating only 16 of its 896 experts per token, roughly 1.8 percent of the pool. It carries a one-million-token context window and native vision. On the aggregate intelligence indices it sits just behind the two leading closed American models and ahead of everything else, including the previous generation of those same American systems; on agentic coding benchmarks the gap to the frontier is within measurement noise. Full weights are promised for July 27.

Two numbers in the launch sheet matter more than any benchmark, because they are economic rather than athletic: $3 per million input tokens and $15 per million output tokens. Hold those against what they are meant to replace. A credible custom-silicon design has historically cost tens of engineer-years. A 48-hour autonomous agent run at K3's list prices is a compute bill in the hundreds or low thousands of dollars. Whether or not this particular model is the one that does it, that is the cost collapse the market glimpsed on Friday: not cheaper intelligence in the abstract — a reprice, by orders of magnitude, of the unit economics of design work.

The sparse architecture is what makes the pricing credible: a model that activates under two percent of its parameters per token can ingest an entire codebase, reason across screenshots and video frames, and hold a multi-day agent workflow without paying the full compute cost of 2.8 trillion parameters on every step. Moonshot's own documentation, it should be said, recommends deployments of at least 64 accelerators — K3 is not evidence that compute demand disappears. It is evidence that the compute buys something new.

The demonstration that moved the market

In a single 48-hour autonomous run, K3 designed an inference chip to serve a nano-scale version of its own architecture. It handled the full flow — architecture, RTL, optimization, verification, timing closure, simulation — using exclusively open-source EDA tools on the freely available Nangate 45nm cell library. No Cadence software. No Synopsys software. No human intervention in the design itself. The result: a 4 mm² die, thirteen modules, 1.46 million standard cells, 0.277 megabytes of SRAM, an INT4 multiply-accumulate array with fused dequantization, timing closed at 100 MHz, sustaining 8,721 tokens per second of decode throughput in simulation.

For good measure, Moonshot also disclosed that K3 wrote a GPU compiler from scratch — a Triton-like system it calls MiniTriton — that matches or beats NVIDIA's own Triton on parts of the benchmark suite, and that an early version of the model handled the majority of kernel optimization work during K3's own late-stage development. The model helped build itself, then designed silicon to run itself.

What the chip is not

Here is the part the Friday selloff largely skipped over, and the part any serious reader needs first.

The chip is, by the standards of the semiconductor industry, unremarkable. A 4 mm² design at 100 MHz on a 45nm open cell library is roughly the scope of an ambitious graduate-student project. The open-source flow that makes such designs possible — OpenROAD, OpenLane and their ecosystem — has existed for years and was built, in part, with U.S. government funding precisely to lower the entry barrier for small designs on mature nodes. Nangate 45nm is an academic teaching library, several full generations behind the 3nm and 2nm processes where frontier AI accelerators actually live and where the proprietary toolchains of Cadence and Synopsys are embedded in ways open-source software does not begin to replicate.

Nor is this a chip in the physical sense. Nothing was fabricated. Timing closure and simulated throughput are design-stage artifacts, not silicon. Moonshot itself calls the exercise a proof of concept, not a production tape-out. And — a detail that matters more than its footnote status suggests — Moonshot has not clarified whether any licensed IP blocks were embedded within the design, a distinction that determines the true scope of what was displaced.

Finally: every number above is self-reported, and the weights are not yet public. Several launch benchmarks are vendor-run, and early independent evaluations have flagged elevated hallucination rates on factual tasks — a reminder that raw generation quality and reliable engineering are different properties. Until the weights and the accompanying technical report land on July 27 — Moonshot says the report will detail the exact EDA toolchain and methodology — nothing about the demonstration can be independently reproduced. The sell-side knows this. One bank's analysts framed the release as raising the capability ceiling for Chinese AI models while shifting the burden of proof to other labs. That is precisely correct: the burden of proof has shifted, but it has not yet been met.

What the chip is

So why did two of the most entrenched software franchises in technology lose fifteen billion dollars of market value over a student-project chip?

Because the chip was never the product. The 48 hours were the product.

What Moonshot demonstrated — if it holds up — is sustained, coherent, self-correcting engineering across a two-day horizon without hand-holding: reading documentation, making architectural decisions, running verification loops, diagnosing failures, iterating. That is a qualitatively different capability from answering questions or completing functions. It is the capability that turns a language model into an engineering organization.

And notice where that capability succeeded, given the hallucination caveat two sections up. A model that stumbles on open-ended factual tasks completed a two-day engineering objective — because chip design is wrapped in the hardest external verifier in commercial software. Simulation passes or it does not; timing closes or it does not. The flow worked not despite the model's fallibility but because the toolchain catches it. That observation — an agent is exactly as good as the verification harness around it — is the single most important sentence in this series, and Parts II and III are largely essays about who owns the harness.

The economics of the capability do not care that the demonstration ran on a teaching library. The open-source flow was the constraint, not the model. The model's task-horizon is what changed. If an agent can hold a chip-design objective coherently for 48 hours on OpenROAD at 45nm, the binding question becomes how fast that horizon extends and how far up the node ladder the toolchain access follows. Neither of those is a physics problem. Both are software problems, and software problems have been falling at a remarkable rate for three years.

This is why the honest framing is not “Kimi K3 threatens Cadence.” It is: Kimi K3 is the first public data point on a curve, and the market on Friday priced the curve, not the point.

DeepSeek showed Chinese labs could compress the cost of intelligence. Kimi K3 suggests they can now compete on capability, context, price, and openness at the same time — and aim the result at hardware.

Next: Part II — what a design-cost collapse does to each layer of the chip chain, and why the physical bottlenecks appreciate. Then Part III — the map across the Rubin Build-Out universe.

Closelook is an investment diary. Nothing here is investment advice or a recommendation to buy or sell any security. All Kimi K3 performance figures are company-reported pending the July 27 weights release and technical report. Market figures reflect closing prices of July 17, 2026.