Heresy · 09:00 CET

The Numerator Regime — Closelook Heresy X

The buyback era inflated financial assets. The AI-capex era inflates bottlenecks — and pays the constraint, not the spender.

The buyback era inflated financial assets. The AI-capex era inflates bottlenecks — and pays the constraint, not the spender.

The heresy: The AI build-out is inflationary in the physical layer, and the spenders are not the clean winners — they are the funders. The cycle pays whoever controls the constraint and gets paid first, not whoever spends the most. Own the tollbooth, not the toll-payer — and do not assume the largest capex line on the tape belongs to the cleanest income statement.

The orthodoxy

Two beliefs govern how most investors own this cycle. First, that AI is disinflationary — software productivity, cost taken out, the deflation that technology always brings. Second, that you own the AI trade by owning its largest names: the hyperscalers, the spenders, the trillion-dollar balance sheets writing the capex checks.

Both are half-wrong in exactly the way that costs money.

The heresy

The AI build-out is inflationary in the physical layer, and the spenders are not the clean winners — they are the funders. The cycle pays whoever controls the constraint and gets paid first, not whoever spends the most. Own the tollbooth, not the toll-payer. And do not assume the largest capex line on the tape belongs to the cleanest income statement.

From denominator to numerator

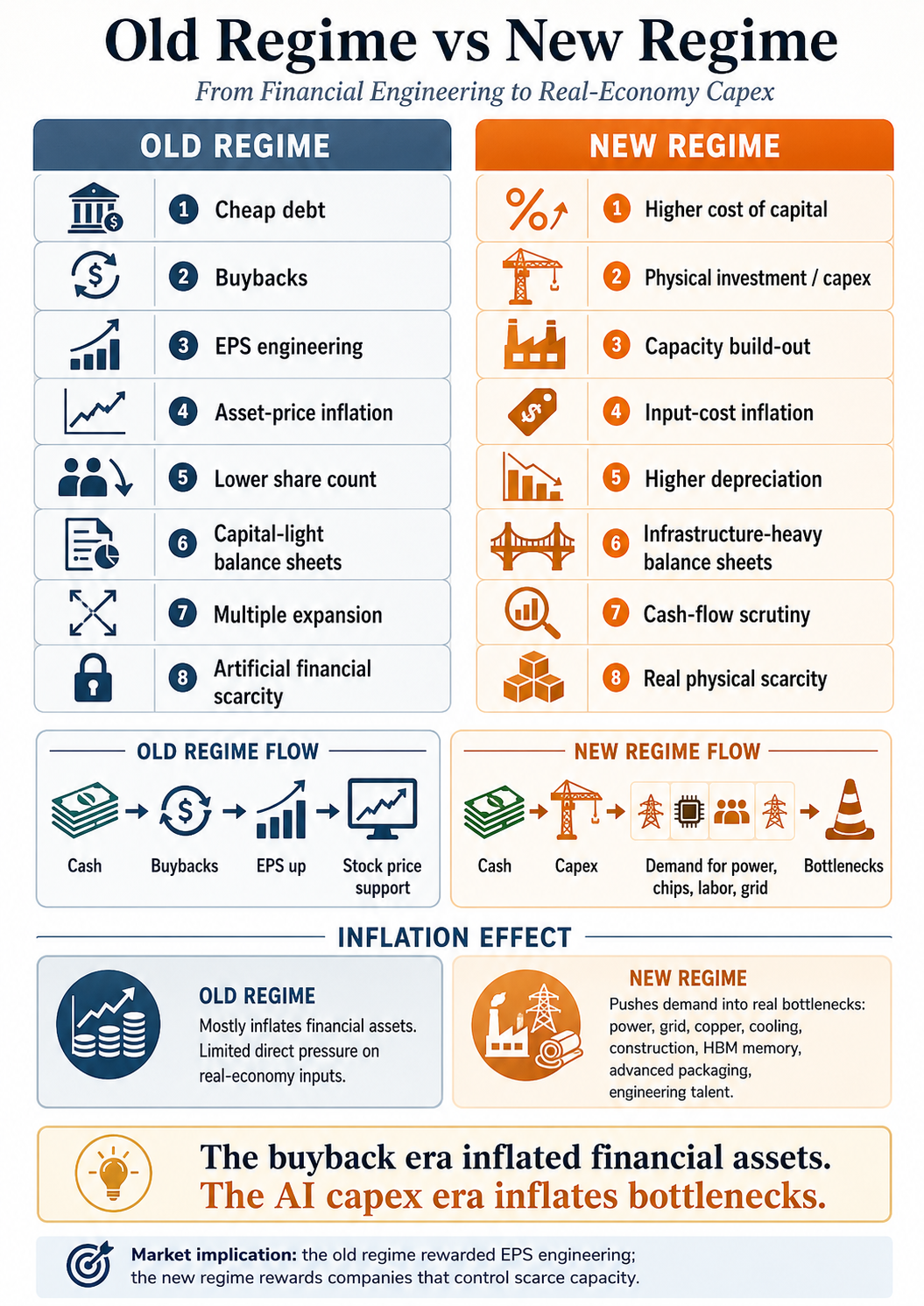

For fifteen years the machine ran one way: low rates, cheap debt, buybacks, lower share count, higher EPS, higher stock price, management comp clears. That was financial engineering — manufacturing EPS growth by optimising the denominator, the share count, while organic revenue growth stayed mediocre. It required nothing physical. It recycled cash into equities.

AI, energy, reshoring, grid, defence, data centres and memory force the opposite machine: higher capex, more physical investment, less free cash flow, fewer buybacks, more depreciation, more debt discipline. The market moves from optimising the denominator to building the numerator — actual capacity, actual output, actual throughput. Financial engineering gives way to physical engineering. That single rotation reprices almost everything downstream.

Why the inflation sign flips

Here is what the disinflation consensus misses. Buybacks are asset-price inflationary, not goods-and-services inflationary. They lift multiples and shrink float; they do not bid for copper, transformers, turbines, cooling, land, engineers, or grid interconnects. Capex does — directly, and in scarce categories.

Software scaled with almost zero marginal physical constraint. That is precisely why the 2010s SaaS cycle was disinflationary and capital-light. AI infrastructure is its inverse: it scales through scarce hardware, scarce power, and scarce supply chains. So “technology is deflationary” becomes a category error the moment it is applied to the build-out. Not broad 1970s inflation — persistent bottleneck inflation, concentrated in the physical layers: power equipment, electricity, skilled construction labour, copper, gas turbines, land around data-centre clusters, advanced packaging, HBM, cooling, substations, grid interconnection, and specialised engineering talent.

The buyback era inflated financial assets; the capex era inflates bottlenecks.

The hidden margin effect

There is an earnings-quality consequence, and it cuts against the spenders. In the buyback era a company could say: operating income up three percent, EPS up eight — because the float shrank. In the capex era the sentence inverts: revenue grows strongly, but free cash flow is weak, because the investment cannot stop. Depreciation rises. Debt discipline returns. Earnings quality matters again — the discipline a decade of buybacks let managements ignore.

That is a very different equity setup, and it favours companies that receive capex over companies that must spend it. The hyperscaler writing hundreds of billions in checks may win the strategic war and still carry a heavier, messier statement while doing it. The supplier converts that same wave into clean revenue and lets someone else carry the depreciation.

The constraint relay, extended

This is where Heresy IX returns. The Constraint Relay described how leadership passes along the binding constraint inside the compute stack — cadence-setter to memory co-clock to CPU to gate. The Numerator Regime carries the relay out of silicon and into the physical world. The constraint no longer stops at HBM and packaging; it runs on into power, cooling, grid, copper, interconnect, and the raw human capacity to build.

Map it onto the generation-rotation layers and it lines up cleanly: Early Ramp claims memory, packaging and substrates; Mid-Ramp claims power, cooling and optical. The tollbooths and constraint-solvers — the cohort the market files under “picks and shovels” — are simply whoever owns the current link in that relay: compute and gate (NVIDIA, TSMC), memory and packaging (SK Hynix, Micron), signal integrity and interconnect (Broadcom, Amphenol, Astera, Credo), power and thermal (Vertiv, Eaton, Schneider). They get paid before the monetisation question is even asked. That is the whole point of a tollbooth. You can watch the within-generation version of this rotation live in the Rubin Build-Out sector reads.

The regime, side by side

| Old regime | New regime |

|---|---|

| Cheap debt | Higher cost of capital |

| Buybacks | Physical investment |

| EPS engineering | Capacity build-out |

| Asset inflation | Input inflation |

| Lower share count | Higher depreciation |

| Capital-light balance sheets | Infrastructure-heavy balance sheets |

| Multiple expansion | Cash-flow scrutiny |

| Artificial financial scarcity | Real physical scarcity |

The five questions

The last cycle was governed by one question: is it capital-light? The new cycle replaces it with five, and they are the entire selection discipline:

- Who controls the bottleneck?

- Who gets paid first?

- Who has pricing power?

- Who must fund the build-out?

- Who only benefits later — and only if monetisation works?

The last two are the trap. “Bullish on AI” is not a position; it is a mood. The position is knowing which of those five a given name actually answers to. The intelligence, as ever, is in the selection — not in the conviction.

The counter-heresy

A heresy earns its place only if it survives the best case against it. Four rebuttals deserve their air:

The spenders may win because of the heavy statement. Capex can be a moat. The hyperscaler who over-builds power and compute ends up owning the scarce capacity everyone else must rent. Heavy today, landlord tomorrow.

AI may be disinflationary where it counts. Inflationary at the build layer — but if the application layer substitutes labour and compresses cost at scale, the net macro sign is ambiguous, and policy reacts to the net, not to the bottleneck.

Bottlenecks invite their own cure. Input inflation is the price signal that pulls capital into power, copper and packaging — which eventually relieves the scarcity. These may be pockets, not permanence, and the real risk is paying peak-scarcity multiples straight into a supply response.

The reflexive trap. If input inflation keeps the cost of capital high, it pressures the very multiples the entire complex — tollbooths included — trades on. The regime that pays the constraint can also de-rate it.

Hold these honestly. The Numerator Regime is a lens, not a guarantee — and a lens that names its own failure modes is worth more than a thesis that doesn't.

The consequence

The market becomes more selective because the easy story is gone. The last cycle rewarded whoever could engineer the denominator. This one rewards whoever controls scarce capacity — and quietly taxes whoever must build it. AI capex is bullish for the economy and for specific suppliers. It is not automatically bullish for every large technology company, because it pulls money away from buybacks, raises depreciation, and makes free cash flow less clean.

The whole heresy in a line:

The old regime rewarded companies that engineered EPS. The new regime rewards companies that control the constraint.

Everything else is narrative.

Heresies is a series of contrarian investment theses; this is Heresy X, extending Heresy IX — The Constraint Relay. Reference-portfolio commentary, not individual investment advice — and we hold skin in the game on the themes we write about. Named companies are exemplars of constraint categories, not a recommendation list; positioning language is reference-portfolio logic, and publishing and money management remain separate.