Rotation

Forward-Deployed Engineers: The Human Infrastructure Layer of Agentic AI

The AI trade is moving from model capability to operating deployment. The clearest public, high-frequency proxy for that shift is not a chip metric — it is a job title.

For most of 2023–2025 the dominant question was: how powerful are the models, how many GPUs are needed, and who owns the infrastructure bottleneck? That was the AI Capex phase, and the market rewarded the visible supply chain — GPUs, HBM, advanced packaging, foundry capacity, networking, power, cooling, data centers. Our Rubin Build-Out index was built to track exactly that chain.

The next phase is different. The question is no longer only whether the model can reason, write code or call tools. It is whether that capability can be inserted into the real workflows of banks, insurers, governments, industrial companies, hospitals and regulated enterprises. That is where the forward-deployed engineer enters — and why we now track it as a leading indicator for the Agentic Ecosystem (opex) and Agentic Winners theses. It is the supply-side complement to our demand-side Agentic Demand family, and the human edge of the same handover we described in the Opex Handover pulse.

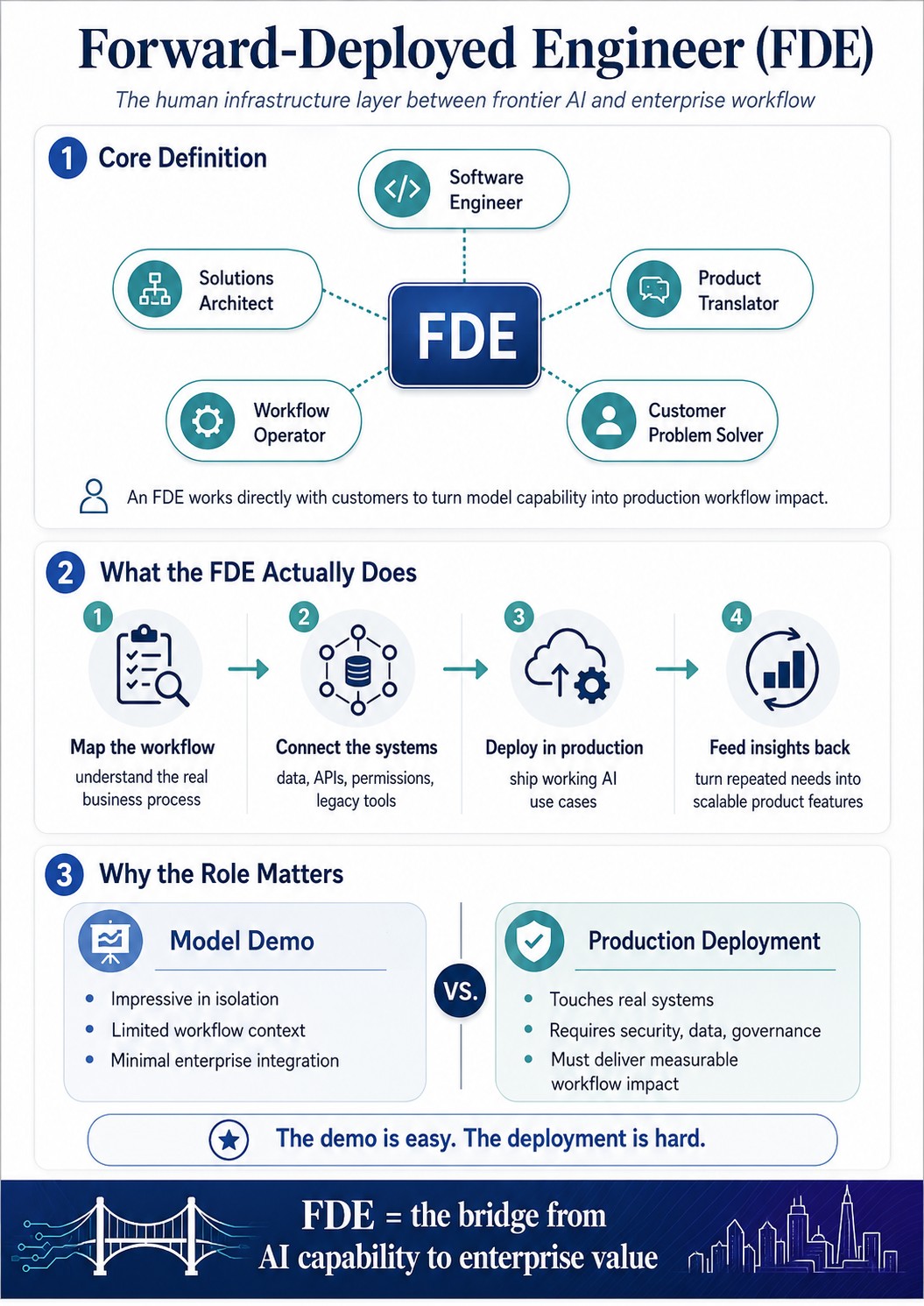

What is a forward-deployed engineer?

A forward-deployed engineer (FDE) is a software engineer who works directly inside or alongside the customer’s operating environment. The role was popularized by Palantir, which frames it precisely: a normal product engineer builds one capability for many customers; the forward-deployed engineer enables many capabilities for one customer.

An FDE is not a consultant, and not merely pre-sales, customer success or implementation. The FDE sits where product, code, data, workflow and business outcome collide. The job is to make the technology work in reality. In the AI era, OpenAI describes its forward-deployed engineers as people who lead complex end-to-end deployments of frontier models in production with strategic customers — and says success is measured by production adoption, measurable workflow impact, and feedback that changes the product and model roadmaps. The FDE does not help a customer “use AI.” The FDE translates frontier-model capability into production workflow impact.

Why the role exists

Enterprise AI is not plug-and-play. The demo is easy; the production deployment is hard. A model can look magical in a controlled setting and still fail inside a company, because the real environment contains legacy systems, permission layers, fragmented data, compliance restrictions, audit requirements, human approval loops and internal politics.

The evidence is blunt. An MIT (Project NANDA) study in 2025 examined roughly 300 public enterprise AI projects and found that the large majority produced little or no measurable profit-and-loss impact — the models worked, but the deployments did not. The gap between capability and outcome is the FDE’s job. This is especially true for agentic AI: a chatbot can live at the edge of the enterprise; an agent cannot. An agent must touch systems of record, workflow engines, data layers, identity systems, ERP, CRM, code repositories and governance controls. That turns AI adoption from a model-selection problem into a deployment-engineering problem — and the forward-deployed engineer is the bridge.

The FDE as AI-opex infrastructure

The first AI trade was capital expenditure: the market paid for the factories of intelligence. The next is operating expenditure: enterprises now spend to make those models useful inside their own systems — and that spend goes not only to tokens but to integration, orchestration, monitoring, security, governance, workflow redesign, data preparation, evaluation and human-in-the-loop control.

So the FDE is not just a job title. It is a signal that the market is entering the operating-deployment phase. In the Capex phase the scarce asset was compute. In the Opex phase the scarce asset becomes deployment capacity — and forward-deployed engineers are one of the clearest public signals of that shift. (Why the per-token cost collapse forces this migration is the subject of our Inference Economics note.)

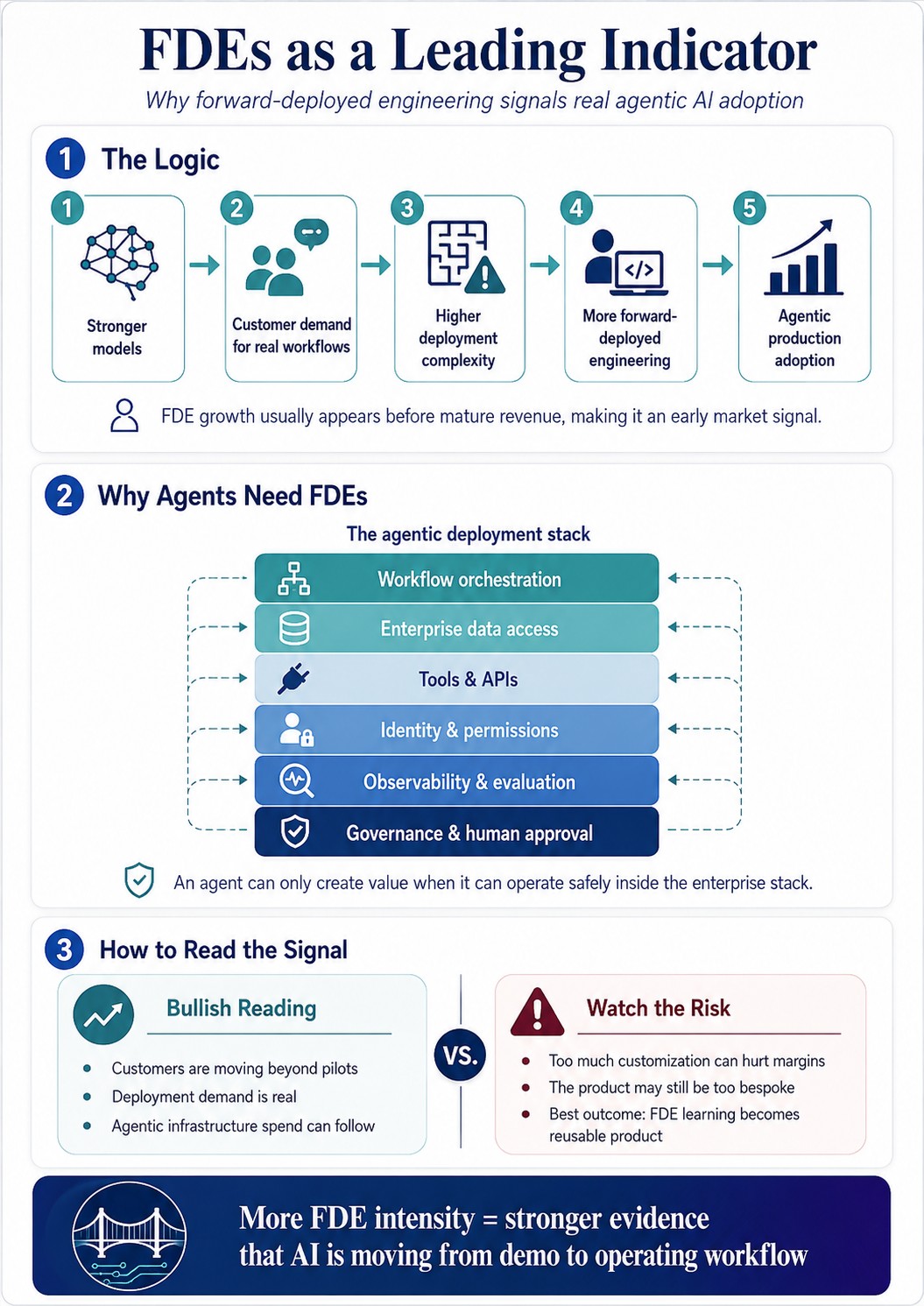

Why FDEs are a leading indicator

FDE activity leads revenue because companies hire these people before the revenue fully shows up. An enterprise does not build an FDE organization because customers are experimenting; it builds one because customers are asking for systems that must work in production. The logic is simple:

No serious agentic uptake without deployment complexity. No deployment complexity without embedded engineering. No embedded engineering at scale without forward-deployed capacity.

When FDE hiring rises, AI vendors are seeing enough customer demand to justify putting expensive engineering talent next to the customer. That is not the same as hiring salespeople: salespeople indicate pipeline; FDEs indicate deployment friction — and, more importantly, deployment opportunity. The bottleneck is moving from “can the model do it?” to “can the enterprise absorb it?”

The new deployment stack

Agentic AI needs a new operating stack; the model is one component. The real stack includes enterprise data access; semantic layers and knowledge graphs; identity and permissioning; workflow orchestration; API and tool integration; observability and evaluation; governance and audit trails; human approval loops; security and compliance; cost control and token budgeting; and change management inside the organization. A forward-deployed engineer touches many of these layers — which is why FDE growth matters not only for the labs but for public-market investors. It points toward the categories that stand to benefit from the opex transition: data platforms, observability vendors, identity providers, workflow systems, orchestration layers, cloud platforms, security platforms and agentic-infrastructure companies — the same map as our Agentic Ecosystem index. The FDE is the human edge of that stack.

Why the signal is becoming stronger now

The FDE model is no longer just a Palantir story. In a four-month span the entire value chain — frontier labs, hyperscalers, software platforms and IT-services firms — converged on the same deployment model:

- OpenAI runs dedicated forward-deployed engineering roles across many markets (including Munich), explicitly described as leading frontier-model deployments in production with strategic customers.

- Anthropic + DXC (11 Jun 2026) announced a multi-year global alliance to bring Claude into mission-critical enterprise systems; DXC — a Global Premier partner — will train tens of thousands of Claude-certified forward-deployed engineers, recruited from its own teams and certified in about 90 days through the Anthropic Partner Academy.

- ServiceNow + Accenture (Knowledge 2026, May) launched a joint forward-deployed engineering program that builds agentic workflows natively on the ServiceNow platform — 300-plus pre-built agent skills, governed through an AI Control Tower — taking customers from pilot to production before enterprise-wide rollout.

- AWS (30 Jun 2026) committed $1 billion to a forward-deployed engineering organization that embeds engineers directly with customers — thousands of engineers, roughly 45-day deployment cycles, pods of five to six, early customers spanning the Allen Institute, Cox Automotive, the NBA, the NFL, Ricoh and Southwest — explicitly “agentic-first,” compressing timelines from months to days, following OpenAI and Anthropic.

When frontier labs, hyperscalers, software platforms and large IT-services firms all move toward the same model, the market is saying something: agentic AI is being adopted not as a software upgrade but as an operating transformation. That requires people, not only models.

The bullish read

FDE growth means enterprise AI demand is real enough to justify high-cost technical labor — companies do not embed engineers with customers unless the commercial prize is large. It is bullish for agentic AI because agents need real workflows, and bullish for the infrastructure around agents: once customers move from pilots to production, they need observability, permissions, orchestration, memory, retrieval, data governance, identity, security and cost control. FDE growth can foreshadow rising demand for the full agentic-infrastructure stack.

The bearish read

There is a real risk. A rising FDE count can mean the product is not yet scalable. If every customer needs a large embedded team, the business starts to look more like consulting than software: it may win large accounts while gross margins come under pressure, and it may reveal that agentic AI is still too bespoke, too fragile and too workflow-specific to scale cleanly.

So the signal must be read in context. FDE growth is constructive when it comes with rising production deployments, contract expansion, usage growth, RPO, net revenue retention and repeatable product patterns. It is more questionable when it comes with margin compression, endless customization, weak product reuse and slow rollout. The best companies use FDEs as learning sensors — deploy into customer environments, discover recurring patterns, convert those into product features, then scale with less human effort over time. The weaker ones simply rent engineers under an AI label. Probability, not prophecy: the indicator tells you the direction of travel, not the destination.

How we measure it

The signal should not be a single job-posting count; it should be a composite. The framework we track:

- FDE Hiring Intensity — forward-deployed, deployment, applied-AI and customer-engineering roles posted by AI companies.

- FDE Share of Engineering — what fraction of total engineering hiring is moving toward customer deployment (size-normalized).

- FDE Geographic Breadth — how many regions and cities show FDE hiring; enterprise deployment is local, regulated and relationship-heavy.

- FDE Organization Maturity — individual contributors only, or also FDE managers, deployment leads and platform roles?

- FDE-to-Sales Ratio — engineers to make deployments work, or salespeople to generate pipeline?

- FDE-to-Research Ratio — for the labs, is the center of gravity shifting from model research toward customer deployment?

- Partner-Certified FDE Capacity — deployment engineers trained through alliances (Anthropic–DXC, ServiceNow–Accenture).

- Earnings-Call Deployment Language — are managements increasingly talking about production deployment, workflow automation and measurable outcomes?

- Production Deployment Count — real, named production rollouts versus pilots and proofs of concept.

From signal to a Closelook index

Closelooknet will track this transition through a dedicated Forward Deployment Intensity index — a measure of how quickly the market is moving from model capability to agentic production adoption. It combines public data: job postings and company career pages, partner announcements, earnings-call transcripts and customer-deployment announcements. The goal is not to count one job title mechanically; it is to measure a structural change — AI moving from demo software to operating infrastructure. The index is built around three lines:

- FDE Hiring Index — monthly forward-deployed / deployment-engineering intensity across the labs, hyperscalers, cloud platforms, software vendors, data companies and agentic-infrastructure providers.

- FDE Partner Capacity Index — certified or announced deployment capacity through IT-services firms, consultancies and platform alliances.

- AI Production Deployment Index — a hard filter for real-world evidence: named customers, production rollouts, regulated-industry integrations, measurable savings, usage expansion, enterprise-wide scaling.

Together those lines show whether agentic AI is merely being discussed or actually being absorbed into enterprise workflows. It is the bridge from the AI Capex trade to the AI Opex trade: the Capex phase was measured in GPUs, HBM, CoWoS capacity, power and data-center spend; the Opex phase will be measured in deployment engineers, production agents, workflow penetration, orchestration, observability, identity, governance and usage economics. The forward-deployed engineer sits at the center of that transition.

This is research and positioning logic — a reference-diary view, not investment advice.; nothing here is a recommendation.

Track the moment when AI stops being a model story and becomes an operating-system story. Stay close. Look closer.

Sources

Verified 30 Jun 2026. Palantir and OpenAI forward-deployed engineer role descriptions (careers pages). FDE job-posting growth: Indeed / Live Data Technologies — about 643 postings (Apr 2025) to about 5,330 (Apr 2026), roughly +729% year over year by one measure; other cuts report higher. MIT Project NANDA (2025), enterprise-AI deployment study. Anthropic and DXC, multi-year global alliance, 11 Jun 2026 (anthropic.com; dxc.com). ServiceNow and Accenture forward-deployed engineering program, Knowledge 2026 (servicenow.com; accenture.com). AWS $1 billion forward-deployed engineering organization, 30 Jun 2026 (aboutamazon.com; TechCrunch; SiliconANGLE).

Closelook publishes a market diary, not investment advice. The strategies described here are educational. Tax, suitability, and risk depend on personal circumstances — consult a licensed advisor before acting.