Heresy

Diversified into the Losers — Closelook Heresy XIII

Why the crowd's cure for concentration is the disease Bessembinder diagnosed

“The best-performing 2.4% of firms account for all of the $US 75.7 trillion in net global stock market wealth creation from 1990 to December 2020.”

— Bessembinder, Chen, Choi & Wei, Long-Term Shareholder Returns

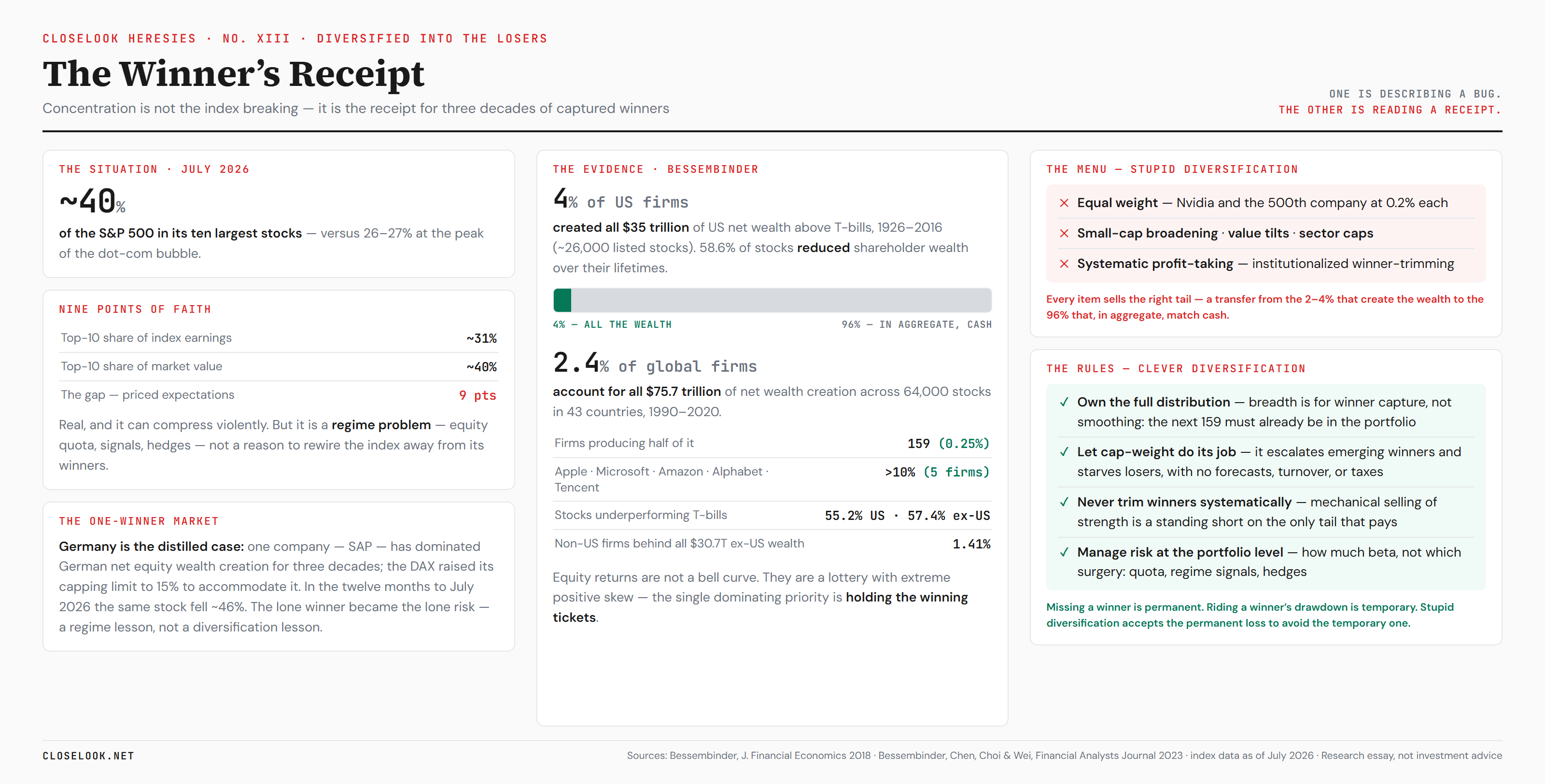

I. The situation

Let us begin with the fact, because the fact is not in dispute.

The ten largest stocks in the S&P 500 now carry roughly 40 percent of the index — on some measures as much as 43 percent, the highest concentration on record. The Magnificent Seven alone account for about a third. For every dollar in a cap-weighted S&P tracker, forty cents sit in ten names; sixty cents are spread across the other 490. The MSCI World, marketed as exposure to 23 developed markets and some 1,400 companies, is roughly three-quarters American, and its top ten holdings are the same American names.

The historical comparison writes itself, which is precisely why everyone is writing it: at the peak of the dot-com bubble in 2000, the top ten reached about 26 to 27 percent. Today's reading does not approach that benchmark. It obliterates it.

One more number, because it is the honest one: the top ten produce roughly 31 percent of the index's earnings against their ~40 percent of its market value. The gap between those two numbers — call it nine points of faith — is real. Concentration at record levels, a cap-weight premium over earnings-weight, and an entire industry of commentary pointing at it.

So far, no heresy. The heresy begins with what happens next.

II. The chorus

Because next, on schedule, the chorus arrives.

You have seen the posts. Your LinkedIn feed is full of them, and so is mine. “You aren't buying the market — you're buying a tech fund with a side of general stocks.” “Passive investing has morphed into a concentrated bet.” “The last time it looked like this was 1999.” The argument always terminates in the same word — dot-com — and the same prescription: diversify properly. Equal weight. Broaden into small caps. Rotate to international. Trim the winners. Or, most conveniently, hand the problem to an active manager who will do all of this for you, for a fee.

Note who is singing. The concentration critique is overwhelmingly authored by active portfolio managers, boutique fund houses, and wealth managers — the professions that have spent fifteen years explaining away their underperformance against the very index they now diagnose as broken. This does not make them wrong. Incentives never make anyone wrong; they make them predictable. After a decade and a half in which “we'll beat the market” died as a pitch, “the market is no longer the market” is the last sales argument standing. Concentration is not their discovery. It is their product requirement.

And the dot-com analogy does the heavy lifting because it is the one crash every client remembers. It converts a statistical observation (weights are high) into a moral certainty (this ends like 2000). Whether the analogy holds — profitless optical-fiber startups at 100x sales versus firms generating a third of the index's actual earnings — is a question the posts rarely reach. The analogy is not analysis. It is a call to action.

III. The menu

And what is the action? When the concentration alarm rings, the industry reaches for a familiar menu. It deserves to be catalogued precisely, because every item on it will matter in a moment:

- Equal weight. Same index, every stock at 0.2 percent. Nvidia and the 500th company, identical allocations. Sold as “automated discipline — buy low, sell high.”

- Small- and mid-cap broadening. Add the Russell 2000, the MDAX, the laggards. More companies must mean more diversification.

- The value tilt. Rotate from expensive winners into cheap left-behinds. Mean reversion as a religion.

- International rebalancing. Trim the US, add Europe, Japan, emerging markets — regardless of where the world's earnings power actually resides.

- Sector caps. Limit technology to a “reasonable” share, redistribute to utilities and staples.

- Active breadth. Sixty to eighty “sensibly chosen” stocks, none above 2 percent. The classic diversified mandate.

- Dividend strategies. Harvest yield from mature payers; skip the compounders that retain capital.

- Systematic profit-taking. Rebalancing rules that mechanically sell whatever has grown. Institutionalized winner-trimming.

- Multi-asset dilution. When in doubt, less equity altogether: bonds, gold, alternatives.

Nine instruments, one melody. Every single item on this menu does the same thing to a portfolio's return distribution: it cuts weight from the right tail and redistributes it toward the middle and the left. Each one, without exception, reduces exposure to the largest winners and increases exposure to everything else.

The menu's implicit assumption is that “everything else” is where safety lives. The evidence says it is where returns go to die.

IV. The evidence

Hendrik Bessembinder, Arizona State University, asked a question so basic it went unasked for a century: over their full lifetimes, do individual stocks beat Treasury bills? The answers, across three studies, remain the least digested findings in modern markets. (Regular readers have met them once before — The Haystack and the Needle used this arithmetic to convict thematic ETFs. This essay is about something larger: the cure the industry prescribes for concentration itself.)

United States, 1926–2016 (updated through 2022): of roughly 26,000–28,000 listed stocks, the majority underperformed one-month T-bills over their lifetimes — in the updated data, 58.6 percent of all US stocks reduced shareholder wealth rather than adding to it. All of the net wealth creation above the T-bill rate — some $35 trillion — came from about 4 percent of firms. The top 90 companies, a third of one percent, produced half of it. The other 96 percent, in aggregate, matched cash.

Global, 1990–2020: 64,000 stocks across 43 countries, $75.7 trillion in net wealth creation. The skew is worse. The majority of stocks — 55.2 percent in the US, 57.4 percent elsewhere — underperformed T-bills. The best-performing 2.4 percent of firms account for all of it. A mere 159 firms — a quarter of one percent — produced half. Five companies (Apple, Microsoft, Amazon, Alphabet, Tencent: 0.008 percent of the sample) produced over 10 percent. Outside the US, the concentration tightens further: 1.41 percent of non-US firms account for the entire $30.7 trillion of non-US net wealth creation.

And the trend runs toward more concentration, not less: in the 2016–2019 window, five firms alone accounted for over a fifth of US wealth creation.

Germany is the distilled version of the ex-US finding. One company — SAP — has dominated German net equity wealth creation for three decades, to the point where the index architecture itself had to bend around it: SAP breached the DAX's 15 percent capping limit (a limit raised from 10 percent in 2023 precisely to accommodate it), forced index funds into mechanical selling of the country's one great winner, and prompted Deutsche Börse to sketch a second, uncapped DAX. A national market with 40 blue chips and, by Bessembinder's arithmetic, approximately one wealth engine. The rest of the exchange list — in aggregate, over decades — is a machine for converting equity risk into T-bill returns, at best.

Read those numbers again and then reread the menu in Section III. Equity returns are not a bell curve where breadth buys you the comfortable middle. They are a lottery with extreme positive skew, in which a rational participant's single dominating priority is holding the winning tickets. Now the reframe, and it is the entire essay:

Classical diversification is the systematic sale of lottery tickets. Every item on the menu — equal weight, small-cap breadth, value rotation, sector caps, winner-trimming — is a transfer of capital from the 2–4 percent that create all the wealth to the 96–98 percent that, in aggregate, create none. It is not diversification across the sources of return. It is diversification into the losers.

There are, in other words, two different activities hiding under one word — call them stupid diversification, which sells the right tail to buy the middle, and clever diversification, which exists to capture the tail. The rest of this essay is the bill for the first and the rulebook for the second.

V. The bill

What does stupid diversification cost? Bessembinder's own arithmetic supplies the invoice: remove the top few percent of performers and the remaining thousands of stocks, in aggregate, match Treasury bills — full equity risk, cash returns. The entire equity risk premium lives in the right tail that the menu systematically trims.

The deeper cost is an asymmetry the chorus never prices:

- Missing a winner is permanent. If your equal-weight fund held Nvidia at 0.2 percent through its ascent while the cap-weighted index rode it from 1 to 7-plus percent, that forgone compounding never comes back. There is no mean reversion in a missed ten-bagger.

- Riding a winner's drawdown is temporary — conditional on the regime surviving. Cap-weight investors ate brutal drawdowns in their winners (Amazon −90 percent after 2000, Apple repeatedly halved) and were made whole many times over, because they still held the ticket when compounding resumed.

Stupid diversification accepts the permanent loss to avoid the temporary one. It sells asymmetric upside to purchase symmetric mediocrity, and it pays fees and turnover for the privilege. Yes, equal weight wins some backtests — chiefly windows dominated by small-cap regimes and rebalancing premia. Averages flatter it; distributions convict it: strategies that structurally underweight the wealth-creating minority must, in expectation, converge toward the return of the wealth-neutral majority. Which is to say: toward cash, plus noise, minus costs.

VI. The steelman

Now the part the chorus deserves to hear said properly, because a heresy that cannot state its opponent's best case is merely a mood.

The critics conflate two different things, and one of them is real. Concentration-as-fact — wealth creation residing in few names — is Bessembinder, and it is an argument for cap-weight. Concentration-as-risk — a handful of names at demanding valuations, correlated to a single narrative, in one country and one currency — is a genuine portfolio condition, and pretending otherwise is its own stupidity. Cap-weight has no valuation brake: it rode Japan to 44 percent of world market cap in 1989 and rode the Nasdaq into 2000, and the cap-weighted investor who bought the S&P peak in March 2000 waited some thirteen years to be durably whole. The nine points of faith between today's top-ten earnings share and market-cap share can compress violently.

Germany just staged the demonstration. The same SAP that outgrew its index has, in the twelve months to July 2026, fallen roughly 46 percent — halved by AI-disruption fears in enterprise software, cloud-margin pressure, and an Oracle-led capex war — dragging the country's flagship index with it. The lone Bessembinder winner became the lone Bessembinder risk. And, irony fully noted: the DAX capping rule that mechanically trimmed SAP near its highs helped German index investors this particular year. Sometimes the stopped clock is right.

But look at what the episode actually proves. Did anyone reliably identify, ex ante, that SAP would halve while other AI-adjacent giants rose? Did the diversifiers rotate out at €270, or were they underweight the entire three-decade ride that made SAP worth trimming? The honest lesson of SAP 2026 is not “own less of your winners forever.” It is: concentration risk is a regime problem, and regime problems require regime tools — exposure management at the portfolio level, valuation awareness, signals that measure whether the tape is confirming or divorcing from the narrative. That is a different discipline (regular readers know where we do that work: the Weekly Signal exists precisely because “how much equity beta right now” is a real question). Performing surgery on the index — permanently rewiring weights away from winners — is the wrong tool answering the right worry. You do not fix a regime problem by institutionalizing a return problem.

What would the critics need to show to win the argument outright? That someone can identify the 2.4 percent in advance, repeatedly, after costs. Fifty years of active-management data are the answer to that.

VII. The alternative

So what does clever, Bessembinder-consistent diversification look like? Not a product. A set of rules:

- Own the full distribution. Breadth has exactly one legitimate purpose, and it is not smoothing — it is winner capture. You hold thousands of stocks not to reduce variance but to guarantee that the next 159 are in the portfolio before anyone knows their names. Maximum breadth at purchase, precisely because selection is impossible. (The return-skew arithmetic is the same one that governs which ETF wrappers earn their place.)

- Let cap-weight do its job. Market-cap weighting is the only scheme that automatically escalates your position in emerging winners and starves your losers — without forecasts, without turnover, without taxes. The concentration in today's index is not a design flaw. It is the receipt for three decades of captured winners. An index that never concentrates is an index that never held a great company to maturity.

- Never trim winners systematically. Any rule that mechanically sells strength — equal-weight rebalancing, profit-taking bands, sector caps — is a standing short position against the right tail, the only tail that pays.

- Beware patriotic diversification. The German investor “diversifying” out of the concentrated MSCI World into a basket of familiar Mittelstand names is executing the purest form of the error: leaving the set that contains the global 2.4 percent for a set that, ex-SAP, has spent decades matching T-bills with equity risk. Home bias is diversification into the losers with a flag on it.

- Manage risk at the portfolio level, not inside the index. If concentration-as-risk worries you — and after SAP's year, it should at least interest you — the levers are equity quota, regime signals, and hedges. How much beta, not which surgery. Keep the return engine intact; throttle the fuel.

- Accept the deal. The price of guaranteed winner capture is riding winner drawdowns. There is no version of the equity risk premium that excludes this. Anyone selling you one is selling item 6 from the menu.

VIII. Falsification

A heresy that cannot fail is a slogan. This one fails if:

- Equal weight or active breadth outperforms cap-weight over a full decade without the assist of a small-cap regime or a winner-collapse at the start of the window;

- Someone demonstrates persistent, cost-adjusted, ex-ante identification of Bessembinder's 2.4 percent — at which point concentration into that skill beats indexing, and this essay becomes a museum piece;

- Future Bessembinder updates show wealth creation de-concentrating — the 2.4 percent broadening toward 10, 20, 30 percent of firms — which would restore the bell-curve world in which classical diversification is rational.

Until one of those happens, the arithmetic stands.

IX. Coda

The chorus looks at the index and sees ten companies wearing forty percent of the weight, and calls it a failure of diversification. Bessembinder looks at a century of data and finds that ten, ninety, a hundred and fifty-nine companies are the stock market's return, and everything else is expensive cash.

Both are looking at the same object. One of them is describing a bug. The other is reading a receipt.

Concentration is the receipt. The risk was always somewhere else — in regimes, in valuations, in the quota you choose to run. Manage that. And the next time a post tells you the MSCI World is “not properly diversified,” ask the only question this essay requires:

Diversified into what?

Related on Closelook: The Haystack and the Needle — Heresy XII · ETF Return Skew · Market Regime · The Weekly Signal · The First 50% Trap

Sources: Bessembinder, “Do Stocks Outperform Treasury Bills?” (Journal of Financial Economics, 2018); Bessembinder, Chen, Choi & Wei, “Long-Term Shareholder Returns: Evidence from 64,000 Global Stocks” (Financial Analysts Journal, 2023); Bessembinder wealth-creation updates through 2022–2025 (ASU W. P. Carey); index concentration data as of July 2026 (S&P top-10 ~40–43 percent, Mag7 ~32–34 percent; dot-com peak top-10 ~26–27 percent); SAP/DAX capping and 2026 drawdown per Deutsche Börse/ISS Stoxx reporting and market data. Closelook Heresies are research essays, not investment advice.