Weekly Signal · · 11 min read

Gold's Buyer Base Has Changed

Gold's Buyer Base Has Changed

Gold has turned negative on the year — and the sharper tell is who stopped buying. Central-bank demand slowed from its extreme pace, Chinese and Indian jewelry demand fell as prices ran too high, and at the margin gold was increasingly owned by the same speculative crowd that had been chasing Bitcoin. Three demand channels softening at once is the real risk. Yet price has pulled back to the lower edge of the multi-year channel — a rule-based buy for us — so we are starting to reinitiate.

Gold is turning negative on the year. And it is not simply weakening. The buyer base has changed.

For much of the move since summer 2025, gold was being bought not only as a traditional inflation hedge or crisis-protection asset. It was increasingly being bought by the same type of marginal buyer who had been buying Bitcoin: investors chasing scarcity, liquidity, protection against currency debasement, and upside momentum.

That changed the nature of the trade. Gold started to behave less like a classic defensive asset and more like a speculative risk-on liquidity asset. That helped it on the way up. But it also makes the current breakdown more dangerous.

The buyer changed

The old gold story was simple. Gold was the hedge against inflation. Gold was the hedge against crisis. Gold was the hedge against currency debasement. Gold was the asset you owned when confidence in paper money weakened.

Those narratives still matter. But they may no longer be the dominant force at the margin.

Since summer 2025, gold increasingly attracted the same kind of buyers who were already buying Bitcoin and other scarcity assets. These buyers were not necessarily buying gold as a conservative insurance policy. They were buying it as part of a broader liquidity-and-debasement trade.

That is a different buyer. And when the buyer changes, the asset changes.

A traditional defensive buyer tends to buy weakness. A speculative marginal buyer tends to chase strength. That means gold can rise faster during the momentum phase, but it can also lose support quickly once the trend breaks. That is what appears to be happening now.

Central banks did not stop — but they stopped being the marginal story

Central banks did not disappear as buyers of gold. That is important. The official sector still owns gold, still buys gold, and still uses gold as part of reserve diversification. Central-bank demand has not collapsed. But it has slowed from the extreme pace of the prior years, and that matters.

The central-bank bid helped create the structural floor for gold. It gave the move legitimacy. It reinforced the idea that gold was becoming more important in a multipolar reserve world. But once gold moved into the $400 GLD area, central banks were no longer the only important force.

They may have still been buying, but they were no longer the dominant marginal buyer driving the price higher.

That baton increasingly passed to financial buyers: ETFs, bars, coins, momentum funds, debasement trades, and the same scarcity crowd that had been buying Bitcoin.

That is the regime change. Gold was no longer only a reserve asset. It became a crowded financial trade.

Jewelry demand is the missing confirmation

The other major problem is jewelry. Jewelry is not a small side category in gold. It is the largest private pool of above-ground gold ownership. Roughly 45% of all above-ground gold sits in jewelry — mostly in India and China.

That means jewelry is not just “consumption.” It is stored wealth.

And that stored wealth is price-sensitive. When prices rise too far, especially in key physical markets like China and India, consumers do not simply keep buying the same amount of gold at any price. They buy less weight. They delay purchases. They exchange old jewelry. They recycle existing gold. In some cases, they sell into strength.

That is exactly the risk now. Jewelry demand has weakened sharply. In China, demand has been down around 30%. In India, demand has also fallen materially. Globally, jewelry volumes have been under pressure as high prices reduced affordability.

This is important because jewelry demand usually acts as a stabilizer for gold. When prices fall, physical buyers often return. But when prices are very high, the opposite happens: the physical buyer steps back. So gold loses one of its natural support systems.

Private gold can become supply

This is the hidden structural downside risk. Because jewelry represents such a large share of above-ground gold, even a small change in household behavior can matter.

The risk is not that everyone sells their jewelry at once. That will not happen.

The risk is that the marginal flow changes. Instead of buying new gold, households exchange old gold. Instead of absorbing supply, they create supply. Instead of confirming the rally, physical buyers become sellers into strength. That changes the supply-demand balance.

A market that looked tight on the way up can suddenly feel heavy on the way down. If financial buyers are still chasing, that extra supply can be absorbed. But if financial buyers are also fading, the market becomes fragile.

That is the key point. Gold is vulnerable when traditional physical demand weakens at the same time that speculative financial demand starts to unwind.

The Bitcoin connection

This is where Bitcoin matters. Gold and Bitcoin are not the same asset. But since summer 2025, they increasingly shared the same marginal buyer.

Both were bought as scarcity assets. Both were bought as debasement hedges. Both were bought as alternatives to fiat money. Both benefited from liquidity and momentum. Both attracted investors looking for upside outside the traditional stock-and-bond framework. But Bitcoin is the cleaner speculative expression of that trade.

If investors want maximum upside, they may prefer Bitcoin. If they want a true defensive asset, they may question whether gold is still a defensive asset if it is now owned by speculative buyers. That leaves gold in an awkward middle ground.

It is less explosive than Bitcoin in a risk-on phase. But it may also be less defensive than expected in a risk-off phase if the wrong buyer owns it. That is why the current move matters. Gold is not only losing price momentum. It may be losing narrative leadership.

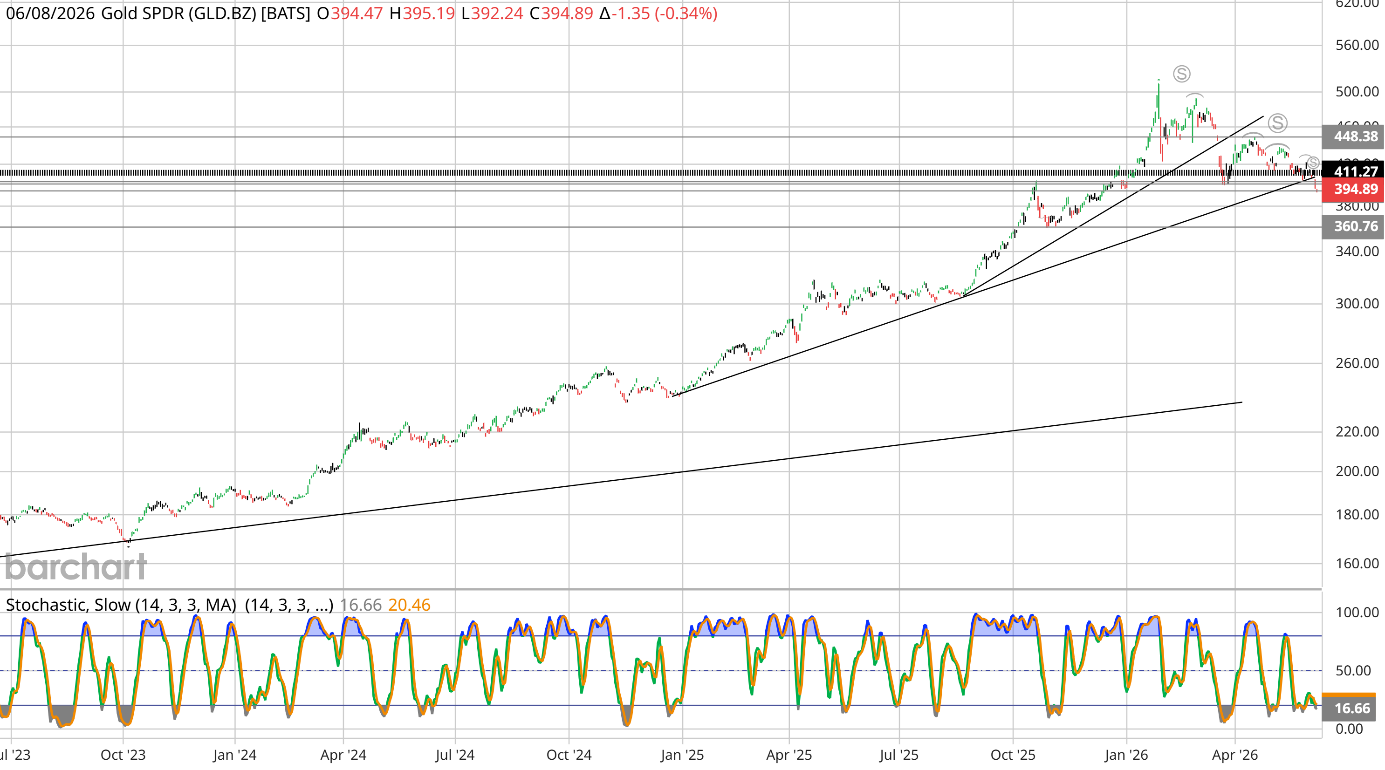

The chart is now confirming the shift

The GLD chart is warning that the trade is weakening. The key near-term level is around $395. That is the immediate support and battleground area. If GLD cannot reclaim and hold that zone, the breakdown becomes more serious. The next major support area is around $360 — the level that matters if the current weakness turns into a deeper unwind.

The technical message is clear: GLD has lost momentum, broken below the prior support zone, and turned negative on the year. That changes psychology. Investors who bought late in the move are no longer sitting on comfortable gains. Some are flat. Some are losing money.

That matters because speculative buyers behave differently when momentum disappears. They do not usually stay because the long-term hedge thesis is intact. They leave because the chart is broken.

Why this matters now

The gold market now has three problems at the same time.

First, central banks are still buyers, but no longer the accelerating marginal force they were earlier in the cycle.

Second, jewelry demand in China and India has weakened because prices became too high. That means traditional physical demand is no longer fully confirming the rally.

Third, the speculative financial buyer that entered gold through the same logic as Bitcoin may now be stepping away.

That combination is dangerous. Gold can handle one weak demand channel. It is much harder to handle three at the same time. If central banks slow, jewelry buyers step back, and speculative buyers unwind, gold can fall much faster than the traditional safe-haven narrative suggests.

What would change the view?

The bearish setup would weaken if GLD quickly reclaims the $400 area and holds it. That would suggest the breakdown is failing and buyers are returning. It would also reduce the risk of a move toward $360.

The second thing that could change the view is a return of traditional gold demand. If lower prices bring back jewelry buyers in China and India, that would help stabilize the market.

The third thing would be a renewed macro shock: falling real yields, a new inflation scare, or a geopolitical crisis. Any of those could revive gold's traditional hedge narrative.

But until that happens, the market has to be judged by the marginal buyer. And right now, that buyer looks less reliable.

The line in the sand

- Reclaims and holds the ~$400 area: the breakdown is failing and buyers are returning — and the risk of a move toward $360 fades.

- Cannot hold ~$395: the breakdown becomes more serious, and the next major support sits around $360.

- What would also turn it: a return of physical demand — lower prices bringing jewelry buyers in China and India back — or a fresh macro shock (falling real yields, an inflation scare, a geopolitical crisis) reviving gold's traditional hedge narrative.

- House view: a secular bull market meeting the lower trend line is a rule-based buy for us, so we are starting to reinitiate — scaled, with the channel floor as the line. Investment diary, not advice.

Bottom line

Gold's weakness is not just a technical story. It is a buyer-base story.

Central banks did not stop buying, but they stopped being the whole story. Jewelry demand, especially in China and India, has weakened sharply as prices became too high. And the financial buyers who pushed gold higher since summer 2025 increasingly looked like the same buyers who were chasing Bitcoin: scarcity, liquidity, debasement protection, and upside momentum.

That helped gold on the way up. But it also makes the breakdown more fragile.

Jewelry accounts for roughly 45% of above-ground gold. If households stop buying, exchange old gold, or sell into strength, private gold can become supply. At the same time, if the speculative financial buyer fades, gold loses the marginal demand that carried it higher.

That is why the current level matters. GLD needs to hold or quickly reclaim the $400 area. If it fails, the next important support sits around $360.

GLD is sitting exactly at the lower edge of the multi-year trend channel. A secular bull market meeting the lower trend line is a rule-based buy for us — so we are starting to reinitiate a position, scaled, with the channel floor as the line in the sand.

The Weekly Signal reads the regime a move is occurring in, not a price target. Closelooknet Weekly Signal — analytical framework, skin in the game, reference portfolios. Not investment advice.