Closelook@US Stock Markets

Customers Waiting, Investors Waiting

The sold-beat regime did not break this week — it got a grading rule. Microsoft and Amazon were paid fifteen percent each for capex with demand already booked; Meta was charged eight for capex in search of an answer; and the chip complex crashed and reclaimed on a settlement calendar, not a thesis.

Current edition · 2026-08-02

This week's edition of Closelook@US Stock Markets, dated August 2, 2026.

Last week's letter ended on a dare: Microsoft's twenty-for-twenty record was about to meet a tape that had sold every collector's beat of the season — either the sold-beat rule broke there, or it was the regime. The market chose a third answer. It did not break the rule; it refined it. Microsoft raised capex and was paid 15.5% — its best print reaction in years. Meta raised capex the same night and was sold 8%. Amazon raised capex Thursday and was paid 15.3% — the largest day-one reaction in its print record. Apple beat on the headline and was sold 7.4%. Same season, same direction of spend, opposite verdicts — because the market has stopped grading the size of the check and started grading its anchor: whether the spending answers demand that is already booked, or goes looking for it. In between, the semiconductor index broke its June floor on a Wednesday close and reclaimed the whole break in one +8.5% Thursday — a crash with a settlement date rather than a thesis. And the Nasdaq closed the week above the shelf that has rejected it five times — on a month-end print this book refuses to score until it survives a week without the calendar's help. The rule, the flush, and the asterisk: that is the whole letter.

1 · This Week's Action Free

The tape, day by day. Monday and Tuesday were the middle of Asia's forced-selling sequence — the US complex heavy but orderly, the real violence six time zones west (the geography of it is Saturday's Global letter; the levels are ours). Wednesday stacked the week's three verdicts into one night: the FOMC held at 3.50–3.75 on a divided 9–3 vote read hawkish — the long end sold to 4.66 on the ten-year and 5.19 on the thirty — while SOXX closed at 465 — fifteen points through the 480.50 June floor: by last week's own written rules, crack #2, the escalation line, and then some. Then Microsoft and Meta printed after the bell and split the sky: Microsoft's beat carried Azure +43%, a contracted backlog up 84% to $678 billion and 30 million paid Copilot seats; Meta's carried a 28% revenue beat wrapped around an earnings miss, an operating margin down from 43 to 31, and a capex floor raised again. Thursday the market graded them in opposite directions — Microsoft +15.5% to 451.10, Meta −8% — while the chip complex ripped +8.5% back to 504.53 the day the forced seller's deadline expired, the single best semiconductor session of the cycle. Thursday night Amazon and Apple repeated the split at higher stakes: AWS accelerating from 28% to 37% growth against Apple's cost-repricing guide. Friday sorted it: Amazon +15.3%, Apple −7.4%, Eaton +7.4% on its eleventh straight beat, the S&P green into the month-end stamp, and QQQ closing at 687.9 — above the 682–684 shelf, round six resolved up, asterisk attached.

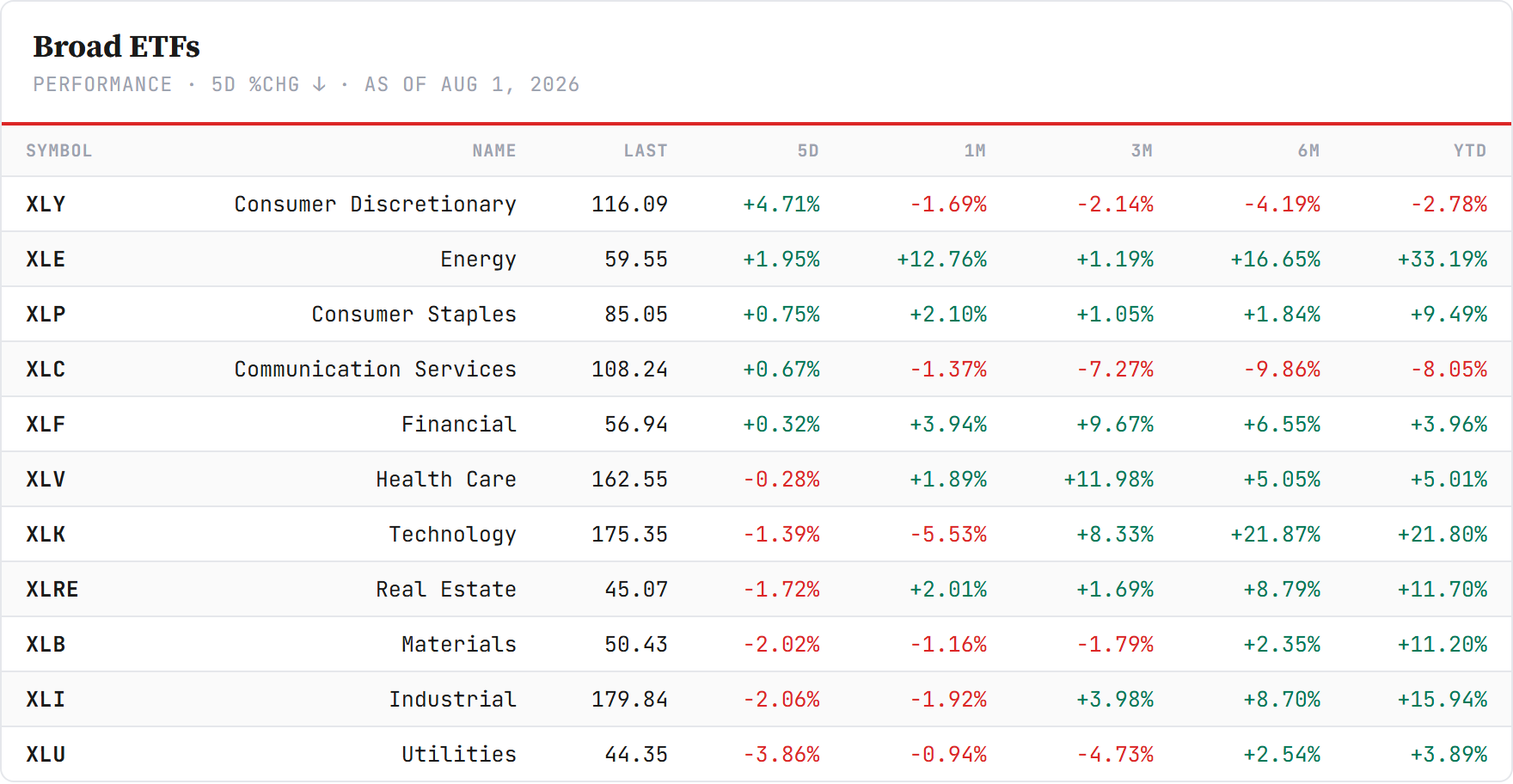

The sector read. Consumer discretionary +4.7% is Amazon's Friday wearing a sector costume — the exact mirror of two weeks ago, when the same sector wore Tesla's miss at the bottom. Energy +2.0% (+33% YTD, the year's sector leader still). The bottom deserves a long look: utilities −3.9%, the week's worst sector — in the same five sessions in which Eaton raised its year on data-center electrical demand and was paid for it. The market paid the company that ships the power backbone and sold the sector that owns the wires: that is a rate trade overpowering a demand trade at the sector degree, and the two lines cannot diverge indefinitely. Industrials −2.1% and materials −2.0% carry the same rate fingerprint.

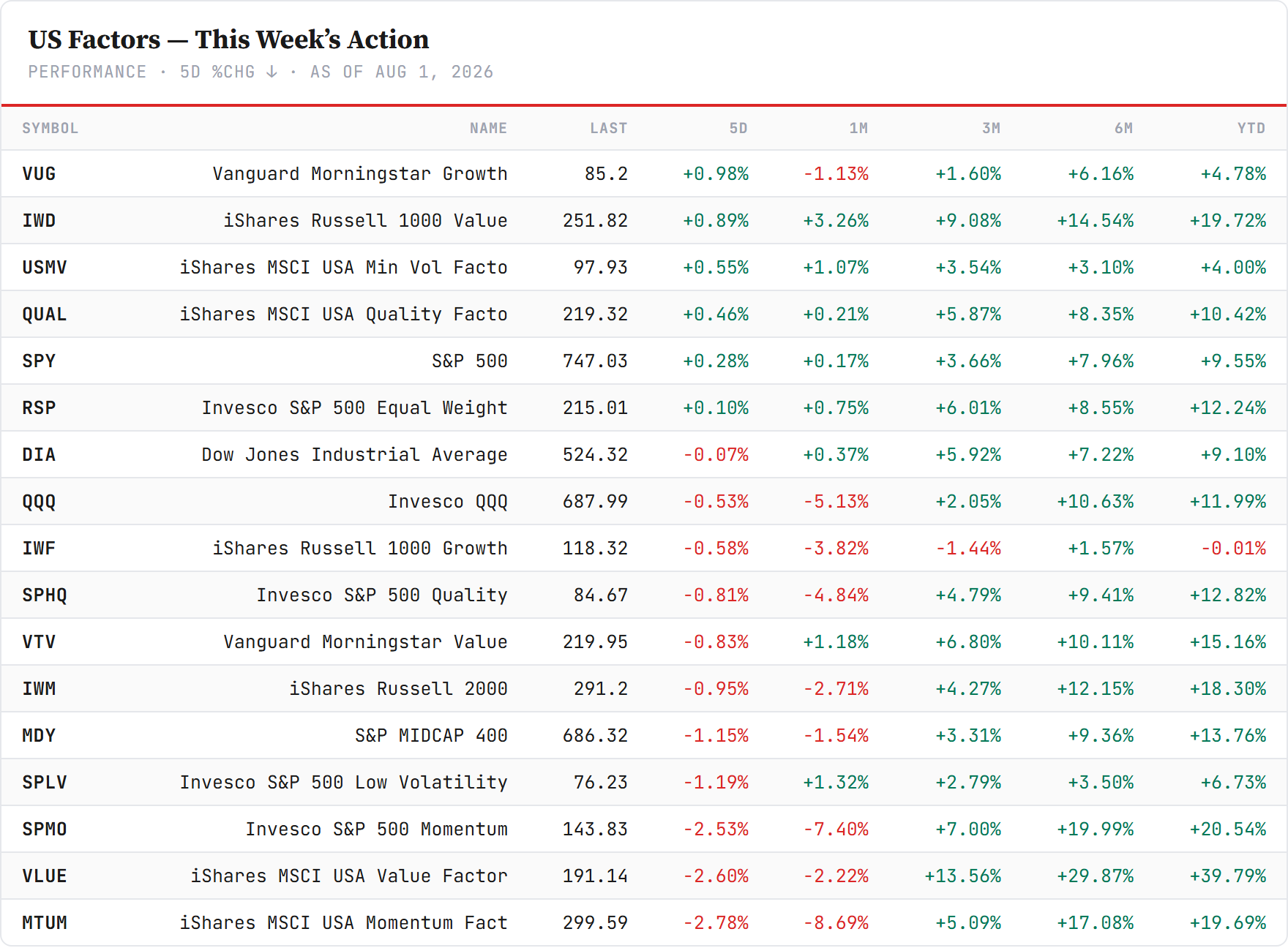

The factor read — the flush's signature. Momentum was the week's casualty — MTUM −2.8%, the S&P momentum cut −2.5% — which is mechanically what a forced liquidation of crowded winners looks like, while min-vol (+0.6%), quality (+0.5%) and the equal-weight (+0.1%) sat out the violence entirely. The S&P green, the equal-weight flat, momentum crushed: a positioning event, not an earnings event — on the week the season's biggest earnings landed. The prints moved single names fifteen percent; the factor complex barely noticed. That divergence is the cleanest evidence yet that July's stress lived in positioning, not in the P&Ls.

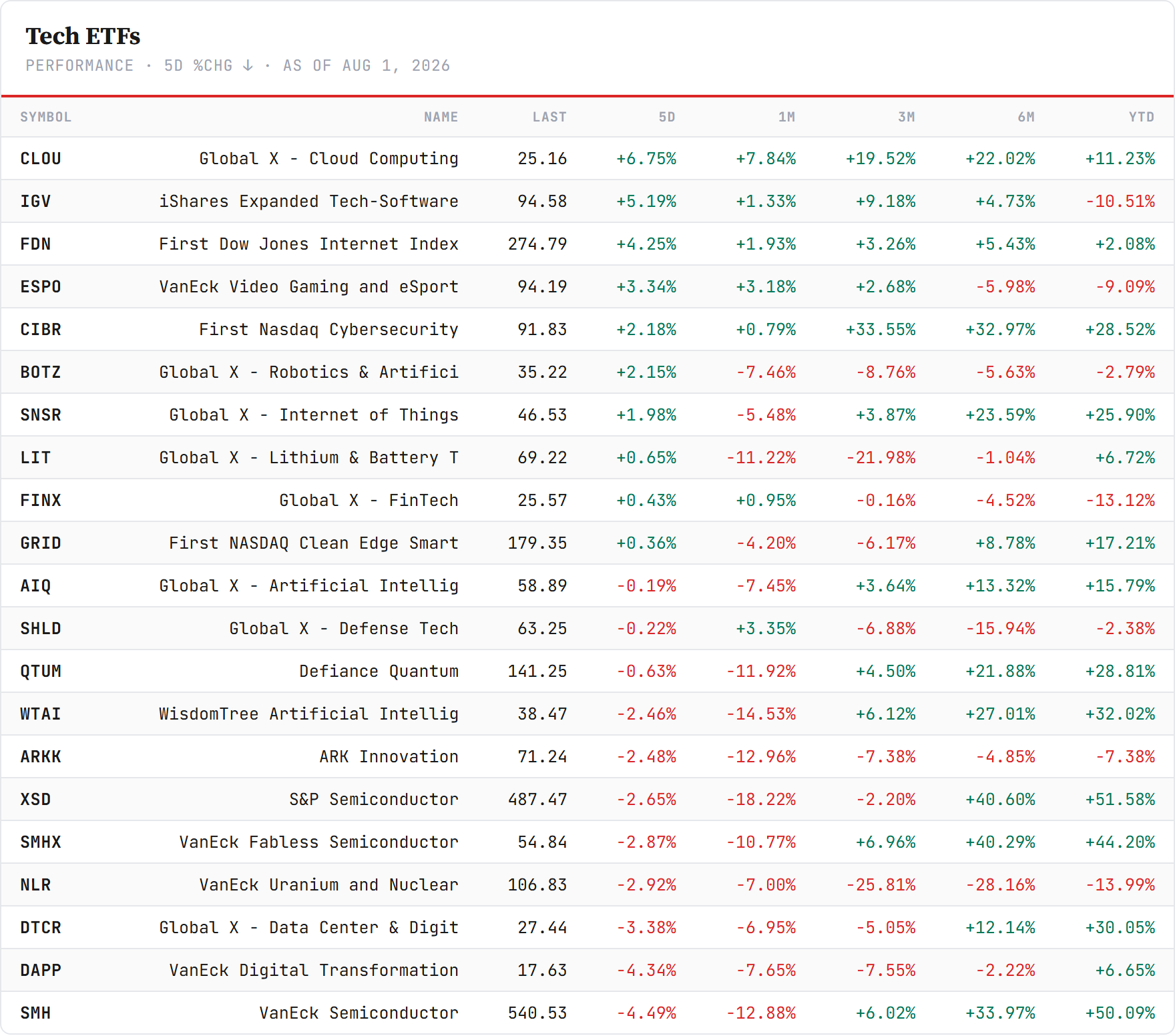

Inside tech — the handoff, printed in the sleeves. The week's spread inside "tech" was ten points: cloud software +6.8%, the broad software basket +5.2%, internet +4.3% against the semiconductor complex −4.5% — and the chip number includes Thursday's +8.5% moonshot. The month-scale ledger now reads: chip designers −18%, broad semis −13%, fabless −11% against cloud +7.8% — a twenty-five-point spread in thirty days. Last week we wrote that the market had started trading the layers instead of the trade. This week the layers reported earnings, and the market paid the operating layer's sleeves on the actual numbers. Two markers fix where that leaves the software side: the cloud basket (CLOU) closed at 25.16, attacking its early-June high of 26.38 — testing its old ceiling while the chip sleeves still trade a fifth below theirs — and the broad software basket (IGV) sits at 94.58, ten points above its June correction low (84.76) but stuck inside the resistance shelf that runs up to 96. One sleeve at the door, one in the waiting room: the operating layer's re-rating is real, and not yet finished proving itself.