Heresy · 08:30 NY

Tech-Free — A Flag of Inconvenience

On the structural underperformance of value investing in a world that no longer rewards it.

There is a moment, on the chart of every great compounder, when the value investor has to walk away. The P/E is no longer "reasonable." The EV/EBITDA is no longer "interesting." The dividend yield, once respectable, has been outrun by the share price. The screen filters cease to fire. The investor closes the file.

This is presented as discipline. It is, mostly, miscalibration.

Above a certain price, good companies are not cheap anymore. Only bad ones are.

That is not a paradox; it is mechanical. The market is, on average, capable of recognising a great business. It bids up the price until the obvious value gap is closed. What stays in the value bucket — what remains cheap — is overwhelmingly the broken, the structurally challenged, the slowly disrupted. Some of these revert. Most do not. Bad companies rarely become good. They become smaller, then forgotten.

The value investor's central wager is that mean reversion will rescue what the market has currently mispriced. In some markets — financials post-2009, energy in 2020, certain industrials — that wager has paid. In others — retail being eaten by Amazon, autos before electrification, cable before streaming, traditional advertising before platforms — it has been a slow, dignified march into underperformance.

The deeper problem is structural

Value investing as a school was built for an economy where most businesses were predictably mean-reverting and where the durable edge came from buying assets below replacement cost. That economy still exists in pockets, but it is no longer where the great compounders live. Increasing-returns businesses, network-effect platforms, AI infrastructure plays — these do not appear on a value screen because they were never supposed to. The screen was designed to filter them out.

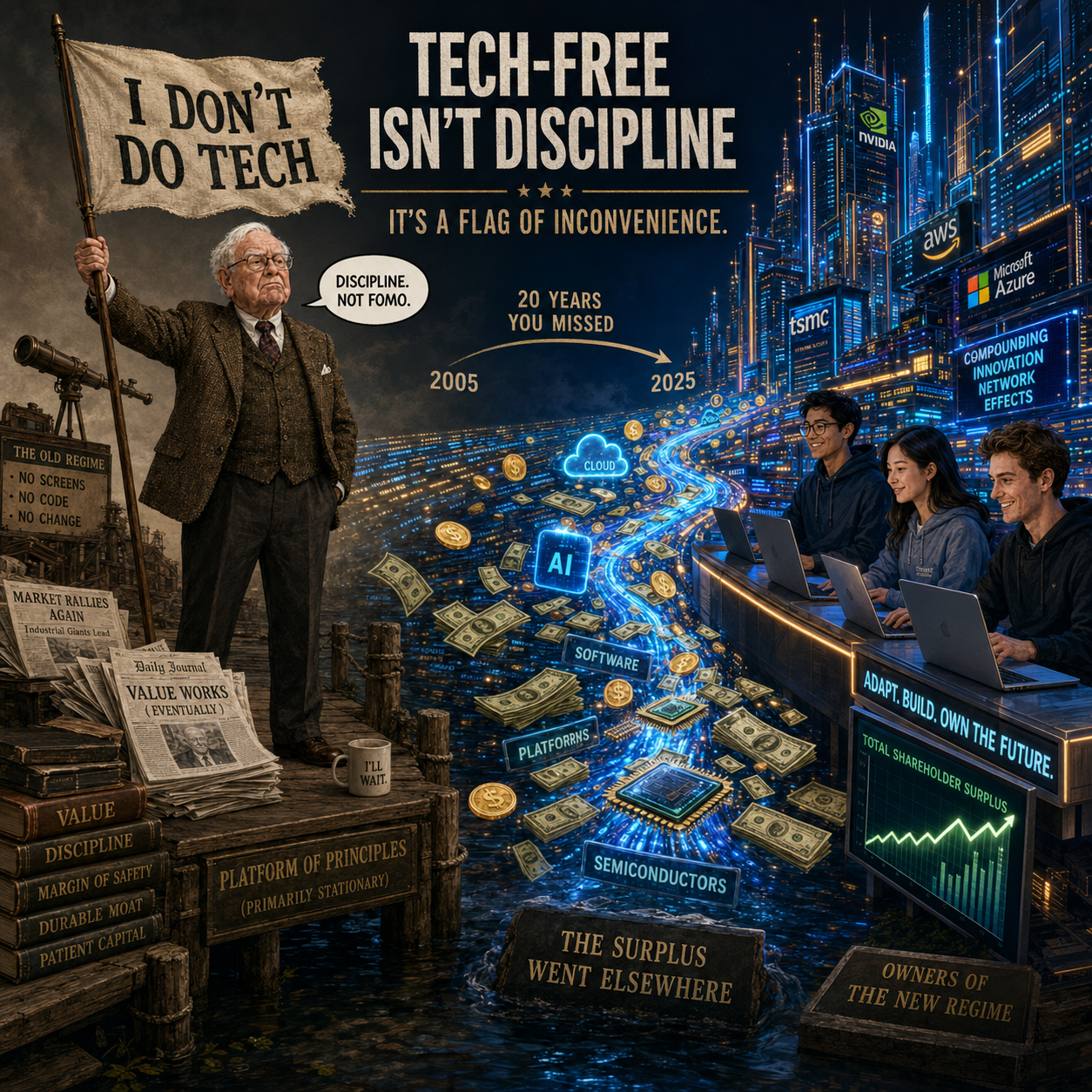

The data is unambiguous and now embarrassing. Over the ten years through early 2021, the Russell 1000 Growth Index returned roughly 400 percent total versus 171 percent for Russell 1000 Value — more than double. Over the five years through mid-2024, the rolling annualised return difference reached minus ten percentage points per year. Two decades of structural underperformance is no longer noise. It is a signal about the methodology.

What you are left with

If you faithfully follow the discipline, you end up holding Pepsi, Coca-Cola, gold, banks, perhaps tobacco. There is nothing wrong with any of these. They are excellent businesses. They are also growing roughly with population and inflation, while the world's productive surplus is being captured elsewhere. A portfolio of high-quality slow-growers, dutifully rebalanced, is a portfolio with built-in underperformance DNA. Not because any individual holding is bad, but because the mix is structurally tilted away from where compounding actually happens.

The most candid version of this critique

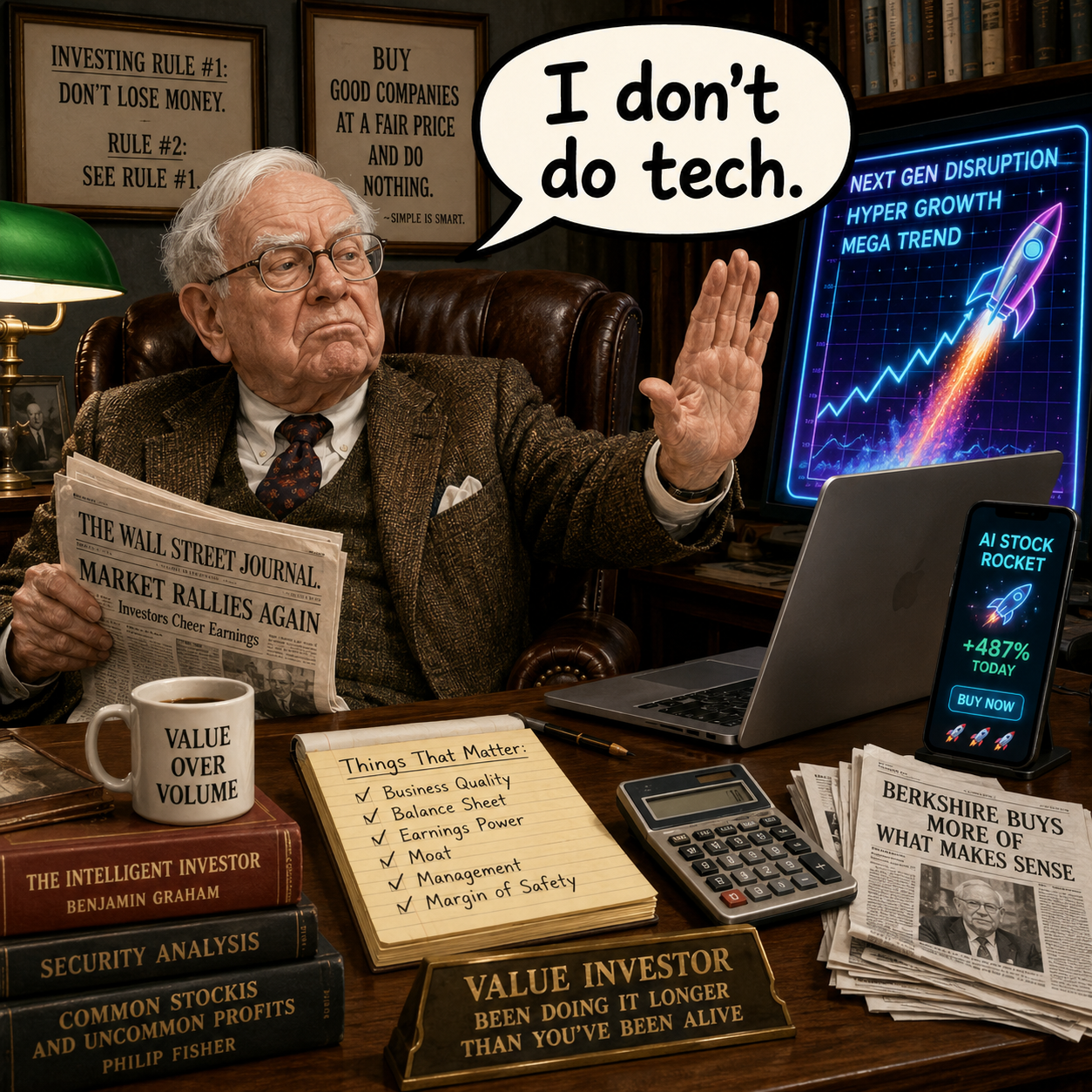

The most candid version of this critique comes from value investors themselves, when pressed. Many of them simply do not understand the technology stack well enough to underwrite it. The vocabulary is foreign. The unit economics look insane on the way up. The capex is uncomfortable. The market caps are vertigo-inducing. So a rule emerges, half explicit, half subconscious: I don't do tech. It sounds humble. In a world where tech is approaching half the economy and a clear majority of the productive surplus, it is not humility. It is a self-imposed handicap dressed up as discipline.

Even Warren Buffett, the patron saint of the school, has acknowledged for years that not understanding technology was his single most expensive blind spot. He bought Apple late and reluctantly, after decades of avoiding the sector, and the position became one of his largest ever — a confession dressed as a victory lap.

Where genuine value work still belongs

There is room for it. A real value process applied to genuinely mean-reverting situations — distressed debt, post-bankruptcy equities, deeply mispriced cyclicals at the bottom — still works and probably always will. But the school as it is widely practised — applied indiscriminately to a world that no longer mean-reverts — has produced two decades of structural underperformance for clients who were told they were being prudent.

Tech-free is not a discipline. It is a flag of inconvenience. The investors who waved it have spent twenty years watching the surplus they meant to harvest go to people who saw the regime they refused to see.

The market does not reward attachment to a methodology. It rewards seeing what is actually happening.