Daily Pulse · · 08:30 NY · signal

Mixed / transitional

Index moves

| Index | 1D | 1W |

|---|---|---|

| Rubin 100 | +3.28% | -4.76% |

| HALO 100 | +2.06% | +0.62% |

| Euro-AI 50 | +3.33% | +4.13% |

| AW25 | — | +5.65% |

Pattern alerts

- PFE support-confluence WARNING

- MCD support-confluence WARNING

- NOC support-confluence WARNING

- UL support-confluence WARNING

- LMT support-confluence WARNING

Cointegration

0 active pairs, 6 breaks.

§1 — Lede

🟡 Cross-asset signals are mixed: gold and long bonds bid hard, dollar soft, but equity leadership is concentrated in Layer 1 semis while broad participation remains uneven.

§1.5 — Pre-market US (futures)

S&P (ES) +0.02% · Nasdaq (NQ) -0.04% · Dow (YM) +0.04% · Russell (RTY) -0.02% · snapshot 10min ago

S&P and Dow futures marginally positive; Nasdaq and Russell slightly negative, signalling tech-heavy and small-cap drag pre-bell.

§2 — Cross-asset regime

Gold $417.40 +1.43% · Bitcoin $77,875 +0.54% · TLT $83.91 +1.07%

Gold (GLD +1.43%) and long bonds (TLT +1.07%) are both bid simultaneously — a defensive co-movement that typically signals underlying duration demand or risk hedging. Bitcoin's +0.54% is constructive but not a leadership print.

§2.5 — Europe midday

DAX +0.12% · CAC +0.06% · Euro Stoxx 50 +0.15% · AEX +0.17% · IBEX -0.01% · snapshot 16min ago

European indices fractionally higher across the board; AEX leads (+0.17%), IBEX the sole decliner (−0.01%), breadth narrow but positive.

§3 — Risk & dollar

DXY (dollar, UUP proxy) $27.73 -0.22% · VIX (equity vol) 17.32 -0.69% · VVIX (vol of vol) 96.45 +1.94% · VXN (Nasdaq vol) 23.71 -1.58% · MOVE (bond vol) 81.53 -4.44%

DXY proxy (UUP −0.22%) continues to soften. VIX at 17.32 (−0.69%) and VXN at 23.71 (−1.58%) move in the same direction, no equity vol divergence. VVIX at 96.45 (+1.94%) sits notably above its ~80 baseline, indicating the options market is pricing elevated uncertainty about future vol itself. MOVE at 81.53 (−4.44%) is the sharpest single-day move in the complex — bond vol compressing hard while equity vol meta-measure rises is a split worth watching.

§4 — Asia overnight

Nikkei (EWJ) +1.02% · Hang Seng (EWH) +0.97% · Shanghai (MCHI) +0.07% · KOSPI (EWY) +3.50%

KOSPI proxy (EWY +3.50%) is the clear regional outperformer; Japan and Hong Kong both gained ~1%; Shanghai (MCHI +0.07%) was essentially flat, confirming intra-regional dispersion.

§5 — US yesterday

SPX (SPY) $741.25 · d +1.02% · w -0.14% · m +5.28%

NDX (QQQ) $713.15 · d +1.66% · w -0.22% · m +10.68%

DJI (DIA) $500.24 · d +1.27% · w +0.62% · m +1.81%

RUT (IWM) $279.87 · d +2.52% · w -0.99% · m +1.95%

Russell 2000 (IWM +2.52%) led the tape, followed by Nasdaq (QQQ +1.66%) and Dow (DIA +1.27%); on a monthly basis Nasdaq is up +10.7% vs. Russell's +1.95%, reflecting persistent large-cap tech dominance over the period.

§6 — S&P 500 sectors

Top-3 (5d): Energy +3.77% · Financials +1.31% · ConsStaples +0.94%

Bottom-3 (5d): Materials -4.49% · Industrials -1.66% · ConsDisc -0.66%

Consumer Discretionary (+2.53%) and Tech (+2.25%) led; Energy (−2.43%), Consumer Staples (−0.66%), and HealthCare (−0.13%) lagged — a pro-cyclical day with defensive sectors sold.

§7 — Europe today

DAX (EWG) +2.00% · FTSE (EWU) +1.66% · CAC (EWQ) +2.41%

CAC proxy leads Europe (+2.41%); DAX and FTSE both up ~2%.

§8 — Reference portfolios

| Index | Day | Week | Month |

|---|---|---|---|

| Rubin 100 | +3.28% | -4.76% | +14.52% |

| HALO 100 | +2.06% | +0.62% | -2.48% |

| Euro-AI 50 | +3.33% | +4.13% | +9.80% |

| AW25 | — | +5.65% | +12.01% |

Euro-AI 50 (+3.33% day, +4.13% week) and Rubin 100 (+3.28% day, +14.52% month) outperform sharply; HALO 100 lags on the month (−2.48%), and Agentic Winners 25">AW25's daily return is not available today. Month-to-date dispersion between Rubin and HALO exceeds 17 percentage points.

§9 — Generation phase

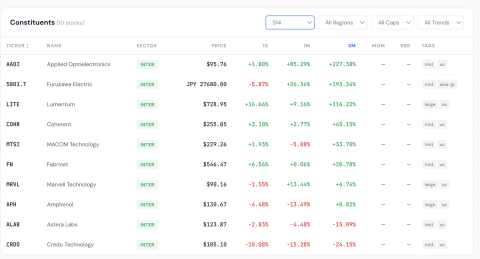

Layer 1 — Architects & IP w +1.22% · m +26.38%

Layer 2 — Manufacturing w -2.85% · m +9.51%

Layer 3 — Memory & Packaging w -6.62% · m +13.24%

Layer 4 — Substrates & Power w -3.98% · m +18.98%

Top sub-sectors (week): EDA & Chip IP +5.14% · Deposition, Etch & Process -0.82% · Architects (Chip Design) -1.25%

Lagging sub-sectors (week): Wafer Processing & Precision -15.46% · Photomasks & Mask Infrastructure -12.54% · Advanced Packaging & Bonding -10.64%

Layer 1 — Architects & IP dominates intraday (+5.41%) and on the month (+26.38%); EDA & Chip IP is the top sub-sector weekly gainer (+5.14%). Wafer Processing (−15.46% week) and Photomasks (−12.54% week) are severe weekly laggards, flagging a split within the semis supply chain.

§10 — Money Temperature

Composite 56 🟡 · Label Mixed / transitional · Instruments 8 contributing

Composite at 56 ('Mixed / transitional') on 8 instruments; the reading is above neutral but not elevated, consistent with selective rather than broad risk-on deployment.

§11 — Pattern Scanner

Active 28 signals · PFE 36 🟡 support-confluence · MCD 36 🟡 support-confluence · NOC 28 🟡 support-confluence · UL 26 🟡 support-confluence · LMT 25 🟡 support-confluence

28 active signals, all top hits flagged as support-confluence patterns; four of five top tickers carry a red regime label (MCD, NOC, UL, LMT), suggesting the scanner is finding potential floors in defensive and industrial names under pressure.

§12 — Cointegration Lab

Active pairs 0 · Breaks 6

Zero active pairs; 6 recent breaks logged. An elevated break count with no reconstituted pairs signals continued structural dislocation in pair relationships — no mean-reversion trades currently open.

§13 — Cross-read

The session presents a structurally ambiguous picture. Gold and TLT rallying together while the dollar softens points to a flight-to-quality undercurrent that coexists, uncomfortably, with the day's pro-cyclical equity surface (Discretionary and Tech leading, defensives sold). VVIX at 96 — well above its 80 baseline — while MOVE compresses 4.4% in a single session is the key divergence: bond vol is normalising fast but equity option traders are paying up for vol-of-vol protection, which is not the signature of a clean risk-on regime. Within equities, Rubin Layer 1 (+5.4%) versus the 17-point monthly gap between Rubin and HALO confirms the tape is narrow: the rally is concentrated in semiconductor architects and AI infrastructure while broad-market baskets, small caps on the week, and defensive sectors diverge. Six cointegration breaks with zero reconstituted pairs reinforces the message that cross-asset relationships are still in flux.

§14 — Watch next session

- VVIX: if it holds above 95 into Friday's close, equity vol-of-vol is signalling a regime shift rather than noise — monitor for a move back below 85 as the normalisation trigger.

- Rubin Layer 1 vs. Layer 3 spread: Wafer Processing is down 15.5% on the week; a bounce or continued divergence from Architects will determine whether the semis move broadens or stays concentrated.

- TLT: if it closes above 84.50, the simultaneous gold-and-bonds bid confirms a genuine duration/safety rotation that contradicts the pro-cyclical equity narrative.