Daily Pulse · · 08:30 NY · market

Temperature 62 — semis re-lead, Interconnects +18% week

Risk-on rally, narrow leadership

Index moves

| Index | 1D | 1W |

|---|---|---|

| Rubin 100 | +0.80% | +5.80% |

| HALO 100 | +0.44% | -0.22% |

| Euro-AI 50 | +1.31% | -1.29% |

| AW25 | — | -2.25% |

Cointegration

0 active pairs, 3 breaks.

Closelook Temperature ticks up to 62 🟡, still in the transition zone but the cascade is breaking. Three pair-relationships are recorded as BREAKING on the regime monitor — BTC–QQQ, QQQ–SPY, SPY–GLD — with the SPY–GLD spread at z = 2.01. The S&P printed a fresh high on the day, the Nasdaq-100 extended on it, and the dispersion underneath both was the widest of the week.

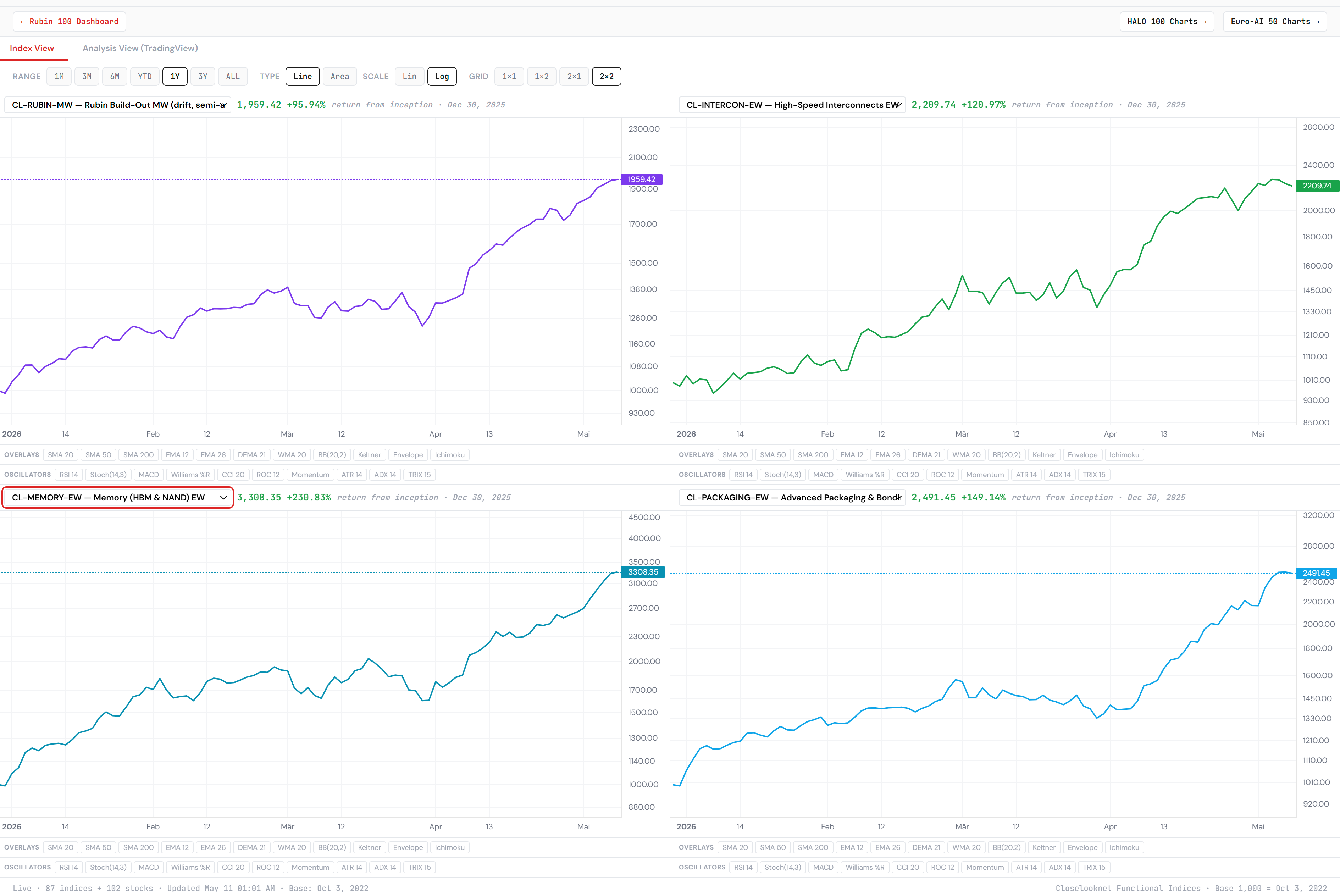

Rubin Build-Out 100 closed +0.80% on the day (CW), +5.80% on the week, +25.41% on the month and +69.66% YTD. The equal-weight cut ran hotter on the month at +27.83%, the momentum-weight variant at +29.44% — both still tracking the same buildout-trade slope. Inside the index, the leadership is concentrated in three sub-sectors:

- High-Speed Interconnects: +17.97% week, +29.66% month, +156.91% YTD. The single hottest line on the entire Rubin matrix. Names: AAOI, Furukawa (5801.T), Lumentum, Coherent, MACOM, Fabrinet, Marvell, Amphenol, Astera Labs, Credo.

- Memory (HBM & NAND): +9.66% week, +55.74% month, +268.40% YTD. The Memory sub-sector alone has now compounded 268% since Rubin's October-2022 base. SK hynix is the structural-authority pick here per the diary; the broader sub-sector confirms.

- Lithography: +8.44% week, +21.18% month. ASML extension after the Korea-semi re-rate.

The laggard inside Rubin is Wafer Processing & Precision at −5.56% week. The composite holds because the winners are doing 18% / 10% / 8% weekly moves while the laggards drop 5%. That is the late-run-concentration signature the tactical-rotation framework on yesterday's cover named explicitly: narrow market breadth, AI-semi exhaustion territory, leadership crowded and extended.

The sector ETFs confirm the same read at the broader-market level. XLK +5.78% week, SMH +7.08%, XLE +3.79%. Defensives and cyclicals soft on the week: XLU −0.49%, XLF −0.50%, XLY −1.01%, XLRE −1.10%. XLV held up at +1.32% on the week but is still −0.77% on the month — the brief healthcare bid from Tuesday's session has not turned into a sustained rotation. The breadth tell: SPY +2.27% week vs RSP (equal-weight S&P) +0.06% — a 221bp spread that says the cap-weighted index ran on a narrow set of mega-caps while the average S&P name was flat.

Country dispersion is the second axis, and it's where the Memory / Interconnects narrative finds its reflection in the global tape. Korea EWY +7.79% week and now +95.97% YTD as the Asian semi supply chain — Samsung, SK hynix — re-rates with the HBM cycle. Taiwan EWT +1.24% week / +50.29% YTD. Netherlands EWN +1.96% week (ASML reads through). At the other end: Indonesia EIDO −5.29% week / −23.48% YTD, India INDA −2.93% week. The EM-heterogeneity pattern flagged in the Lab Read is on full display this week — there is no "EM" anymore as a single asset class, only a 13-percentage-point weekly spread between Korea and Indonesia.

Inside HALO the divergence is sharper than the −0.22% week composite headline suggests. The five hottest sub-sectors: Space & Satellite +14.98% week / +19.21% month, Energy Transition & Clean Power +15.06% week / +26.54% month, Energy MW +12.94% week, Longevity & Healthspan +1.91% week / +5.94% month, Nuclear & Uranium −2.03% week. The five coldest: Defense & Drones −5.84% week / −12.10% month, Better Food / Clean Label −5.09% week / −11.36% month, Med Devices & Animal Health −5.32% week / −11.37% month, Destination Economy −4.63% week, Payments & Financial Infra −4.87% week. Defense is being repriced hard across both HALO and Euro-AI — the late-2025 rerate is now unwinding.

Euro-AI Sovereign 50 is split the same way at the sub-sector level. CL-EUROAI-CHIP (Chip Architecture & Cloud) +14.67% week / +38.43% month — ASML and ARM extending. Semi Equipment & Materials +6.67% week / +27.22% month. Power, Grid & Cooling +0.98% week. Industrial AI & Robotics −3.19% week. Defense & Aerospace −8.91% week / −17.29% month — Rheinmetall and the European defense cohort losing the geopolitical-rerate premium.

The cointegration monitor is the structural read on all of this. Three pair-dominoes are BREAKING simultaneously: BTC–QQQ (the risk-asset coupling), QQQ–SPY (tech vs broad), SPY–GLD (risk vs haven, spread z = 2.01). When three relationships dissolve in one cascade like this — and the cascade is ordered from outermost asset class inward — the regime is re-pricing through pair relationships rather than through any single move. Pair Spreads on the monitor: Risk vs Haven +27 (risk-on), Tech Premium +3 (slightly positive), De-dollarization −18 (dollar bid), Duration −45 (rates moving up, not flight-to-quality).

Forward focus: whether the SPY–GLD cointegration break resolves through dollar weakness (gold catches a bid) or rate-fade (TLT recovers); whether Memory and Interconnects can hold their parabolic monthly slope through the AAPL / NVDA earnings window; and whether the defensive bid that briefly emerged on Tuesday returns now that the late-March winners have re-asserted leadership. The diary continues to size down the names that have done the most work since the March/April lift-off — the cover framework from yesterday still applies.