Daily Pulse · · 08:30 NY · market

Temperature 59 — first crack in semis, defensives bid

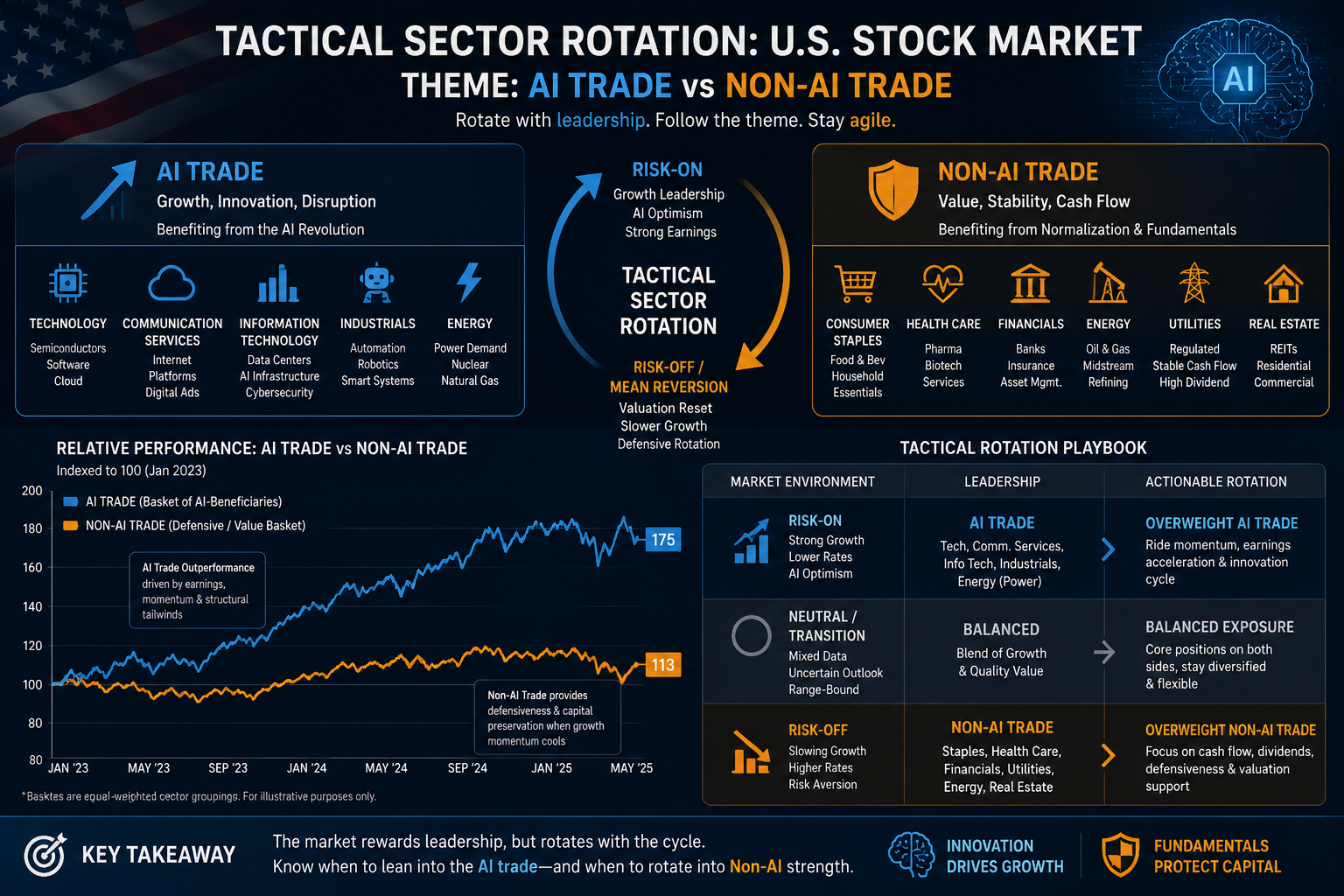

Risk-on but rotating

Index moves

| Index | 1D | 1W |

|---|---|---|

| Rubin 100 | -2.95% | +4.95% |

| HALO 100 | -0.89% | +1.08% |

| Euro-AI 50 | -2.39% | -2.31% |

| AW25 | — | +0.03% |

Pattern alerts

- NOC support-confluence WARNING

- MCD support-confluence WARNING

- PFE support-confluence WARNING

- NOW support-confluence NEUTRAL

- JNJ support-confluence WARNING

Cointegration

0 active pairs, 7 breaks.

The Closelook Temperature sits at 59 🟡, still risk-on but Tuesday's session put a fresh divergence on the tape. The Rubin Build-Out 100 shed 2.95% on the day after a 27.3% trailing-month surge — the kind of single-session reversal that typically marks a digestion phase rather than a trend break, but worth watching. The Euro-AI 50 followed Rubin lower with a 2.39% daily decline and is now negative on the week at −2.31%, suggesting European semi and AI names are meeting resistance after their own month-long recovery. HALO 100, with its larger defensive and healthcare weight, held up at −0.89% — exactly the basket composition that should outperform if rotation is underway.

The sector tape from Tuesday confirms the rotation read. Defensives bid hard: XLV +1.96%, XLP +1.28%, XLF +0.78%. Cyclicals and tech rolled: XLK −1.51%, XLY −0.90%, XLI −0.39%. SPY closed −0.15%, masking a wide cross-sectional spread of roughly 350bps between healthcare and tech in a single session.

Inside semis the damage was sharper than the cap-weighted ETFs suggest — SOXX −3.15%, SMH −2.61%, AVGO −2.13%, MRVL −3.71%, with SOXL (3× bull) down 9.4%. NVDA itself held green at +0.61%, the only major semi up on the day. Single-name confirmations of the rotation: Netflix +2.59% and Sprouts Farmers Market +6.51% — both non-AI, non-tech.

The Pattern Scanner registered 28 active signals, top five clustered in support-confluence setups: NOC at 41 confidence and MCD at 37, both in red regimes, alongside PFE and JNJ in yellow. NOW is the one growth name in the cluster at green-regime, 34 confidence. The scanner is finding technical floors in defensive names — pharma, defense, staples — not in names riding momentum. That pattern read lines up cleanly with what the sector ETFs printed yesterday.

Cointegration shows zero active pairs against seven recent breaks — a structurally elevated break count without new pair formation. When pair relationships dissolve in bunches like this, cross-asset correlations are shifting. That fits the rotation hypothesis: capital rebalancing across sectors rather than settling into a clean trending environment.

Forward focus: whether Rubin can hold the week's +4.95% gain through Friday, whether Euro-AI's week-to-date weakness deepens or finds a floor, and whether the defensive bid in pharma/staples/financials extends into a second session — a one-day move is rotation noise, a two-day follow-through is rotation signal.